Uma carta aberta aos criadores. Atualmente, existem centenas, se não milhares, de boletins informativos viáveis baseados em associação. E isso é ótimo - uma vantagem inequívoca tanto para criadores quanto para consumidores. Desses milhares, vários deles servem como fontes de ideias originais, notícias e análises que são incrivelmente valiosas para os ecossistemas profissionais. É a síntese dessas ideias que tem o maior impacto potencial. Se a educação não tem preço, estamos entrando em uma nova era de criação de valor. Imagine uma cafeteria da era do Iluminismo.

Há boletins informativos dirigidos por operadores que publicam ideias originais. Há cartas significativas que fazem a curadoria das ideias de outros. Algumas delas informam sobre as notícias e outras categorizam e comentam os desenvolvimentos do setor. Muitas vezes, os relatórios que foram escritos por uma pessoa são aprimorados por outras. E, com bastante frequência, os principais veículos de comunicação, como o The Wall Street Journal ou a CNBC, pegam os conceitos originais e os transformam em seus próprios conceitos. Como em uma cafeteria, essa é uma forma valiosa de síntese de informações.

John Dowell é professor da Michigan State University. Em seus quase 40 anos de carreira, ele lecionou inglês, sociologia e antropologia. Seu curso sobre a introdução da síntese explica:

Uma síntese é uma discussão escrita que se baseia em uma ou mais fontes. Portanto, sua capacidade de escrever uma síntese depende de sua capacidade de inferir relações entre as fontes - ensaios, artigos, ficção e também fontes não escritas, como palestras, entrevistas, observações. Esse processo não é novidade para você, pois você infere relações o tempo todo - por exemplo, entre algo que leu no jornal e algo que viu pessoalmente, ou entre os estilos de ensino de seus instrutores favoritos e menos favoritos.

Na Era do Iluminismo (1715-1789), um europeu podia entrar em uma cafeteria pagando uma bebida. Mas a bebida era apenas o preço da entrada, a conversa era a atração. Não eram apenas as conversas sobre assuntos de sociologia, economia e direito que impulsionavam a época. Às vezes, os clientes ouviam conceitos que preenchiam lacunas em seu próprio pensamento. Outras conversas solidificavam ideias fundamentais, direta ou indiretamente.

Inspiração para a cafeteria

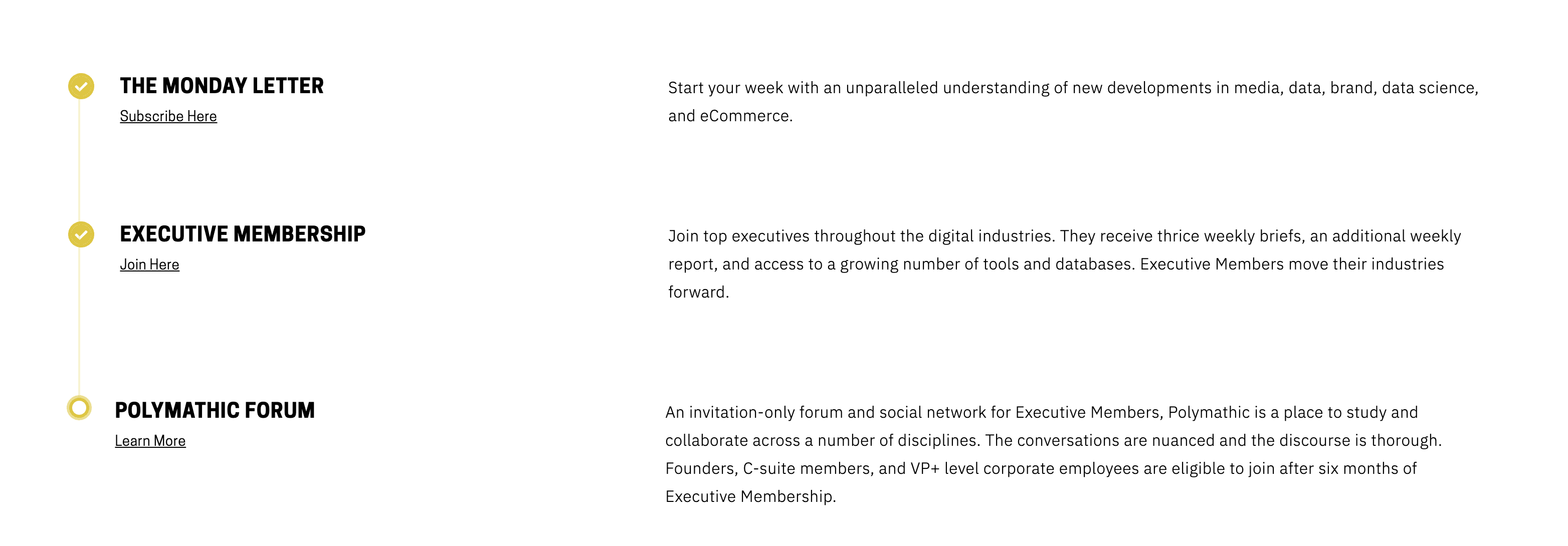

Em novembro de 2015, tive uma conversa em uma cafeteria que me marcou como uma das discussões profissionais mais importantes que já tive. A discussão era sobre a mecânica da comunidade e a necessidade de ferramentas que pudessem maximizar a serendipidade. Em um dia ocioso no final de 2015, comecei a planejar o lançamento do que eu então chamava de 2PM Links. Paguei por um serviço chamado Goodbits e lancei a página de destino do site. Depois de mais ou menos uma semana promovendo a ideia do 2PM no Twitter, confirmei que a primeira carta seria publicada para doze leitores inteiros. Eu passaria a publicar cinco dias por semana durante 180 dias úteis seguidos.

No papel: O 2PM Links seria uma parte de conceitos originais e uma parte de síntese de dados e narrativas, uma curadoria de desenvolvimentos que contariam uma história. Os próprios e-mails permitiriam o diálogo 1:1. Os leitores mais engajados escreveriam explicando como reconheceram microtendências e movimentos maiores. Outros explicavam métodos para sintetizar cada carta para obter o máximo efeito. Ocasionalmente, eu lia um e-mail de um dos primeiros assinantes explicando como um conjunto de artigos ao longo de várias semanas o ajudou a planejar as próximas etapas de sua empresa. Por quase dois anos, essas cartas ajudaram a sustentar a motivação para manter a consistência operacional.

Alcance vs. Profundidade

Para criar algo que foi projetado para crescer lentamente, mantive funções remuneradas em empresas estabelecidas. Entretanto, na época em que comecei a publicação, eu estava entre empregos na mídia. Tendo gerenciado ou liderado o comércio eletrônico em duas editoras de mídia digital, aprendi muito com dois estilos muito diferentes de publicação baseada em conversão (leia-se: afiliada).

A Empresa A criou um funil hiperdirecionado, concentrando-se em um consumidor específico (afluente). Nesse caso, o tráfego direto era alto e o SEO era um funil secundário. A marca era o mais importante. Essa empresa dependeria dela. A empresa B criou um sistema que dependia de SEO e do interesse no tópico, e não da influência da plataforma em si. Para a B,a fidelidade do leitor era secundária em relação à descoberta de SEO. Os visitantes clicavam para ler sobre um tópico com o qual haviam se deparado. Se A fosse um funil, ele seria curto e largo. A confiança era construída com o tempo. Para A, o número de leitores seria impulsionado pela fidelidade à plataforma. Enquanto isso, o funil B captava novas pessoas otimizando os artigos para palavras-chave de tópicos. Seu funil seria mais longo, com vários pontos de entrada ao longo dele. Esses pontos de entrada também serviriam como oportunidades de saída. A rotatividade era maior.

O resultado:

- Empresa A: público menor, maior fidelidade, maior taxa de conversão. 1,8 milhão a 2,2 milhões de MAU. Segmento de produto: luxo moderno.

- Empresa B: menor fidelidade, menor taxa de conversão, público maior. 6-7 milhões de MAU. Segmento de produto: luxo acessível até ofertas diárias.

A e B continuam a operar marcas de mídia bem-sucedidas com objetivos diferentes. Como se diz, há mais de uma maneira de esfolar o gato.

Para comprovar a viabilidade a longo prazo do boletim informativo, dei 180 cartas para que as coisas fossem resolvidas. À medida que as coisas avançavam, o 2PM assumia cada vez mais características da Empresa A. Depois de chegar ao número 180, essa identidade influenciava as próximas etapas. Quando eu chegasse à Carta nº 180, haveria três opções:

- seguir em frente e publicar o nº 181

- fechar a carta

- replanejar e criar uma empresa

A escolha foi a opção número três. Em minhas sete páginas de planos rabiscados, concordei que enfatizaria a profundidade em vez do alcance. Manteria a ênfase na versão "A" da mídia. Para isso, enfatizei um modelo de assinante pago. E, em seguida, um modelo de dados/consultoria. E, mais tarde, uma comunidade executiva. Essas iniciativas me permitiriam reinvestir as receitas em serviços aprimorados, design, desenvolvimento de conteúdo e maior acesso geral.

Do público à comunidade

Em uma questão de duas semanas, entre dezembro de 2017 e janeiro de 2018, mudei a plataforma do Goodbits para o Mailchimp, projetando uma integração com o Memberful. Investi em branding e design. Programei grande parte da v1 do site em meu tempo livre. E, mais tarde, importei cerca de 240 edições do 2PM para o site do WordPress, uma a uma. Em março de 2018, após dois meses de testes, a primeira assinatura do 2PM foi lançada para os assinantes da Monday Letter.

Dessa forma, o sistema do 2PM tornou-se uma espécie de funil. Cerca de 10% de todos os assinantes tornam-se membros executivos. E, mediante convite, uma porcentagem dos membros executivos opta pela comunicação direta com executivos que pensam da mesma forma em vários setores digitais.

A comunidade de Membros Executivos do 2PM, Polymathic, foi inspirada por dois pensamentos distintos.

- O fórum foi criado para ajudar executivos talentosos a desenvolver novas competências essenciais por meio de: (a) identificando pontos cegos e (b) aprendendo com líderes que dominaram essas atividades.

- Quando cheguei ao último Code Commerce, lembro-me de quatro ótimas conversas em minha primeira hora no local. Essas conversas foram com Jason Del Rey, Alex Taussig, Marc Lore e Jen Rubio.

Para participar do evento de dois dias da Recode, os ingressos variam de US$ 2.000 a US$ 4.000. Nesse aspecto, o preço tem uma função valiosa. Lá, é provável que todos com quem você conversar deixem uma impressão valiosa. Os eventos tendem a atrair operadores de alto nível. Entre os discursos principais desses eventos importantes, poucas conversas são desperdiçadas e quase todas as interações extracurriculares agregam valor profissional. Dessa forma, o evento não é o único produto. A comunidade de participantes proporciona um valor adicional. O Polymathic Forum foi projetado para se assemelhar aos corredores digitais das principais conferências, como Sundance, PopTech, Google's Solve for X ou FOO Camp. À medida que o número de participantes aumenta, aumenta também a força do local.

Desde a recepção de 15 a 25 membros executivos em nossas mesas-redondas mensais até a criação do Polymathic da 2PM, a mudança do público para a comunidade proporcionou serendipidade de maneiras que antes eram inimagináveis. A receita da assinatura torna-se a principal variável aqui. As assinaturas pagas oferecem um nível de oportunidade que as plataformas orientadas por publicidade não podem oferecer. Como exemplo prático, considere a diferença entre restaurantes fast food e estabelecimentos quatro estrelas.

Em geral, há dois tipos de restaurantes. Uma cadeia anuncia "bilhões de pessoas servidas". Isso enfatiza os KPIs da empresa: alcance, volume e satisfação das massas. Mas e se você não estiver tentando alcançar as massas? O segundo tipo de restaurante se baseia na qualidade da comida e do serviço, além da atmosfera convidativa para conversas. Nesse último ambiente, é mais provável que se encontre a serendipidade. É emblemático de uma mudança de priorizar o público (alcance) para priorizar a comunidade (profundidade).

Andy McIllwain, gerente sênior de marketing da GoDaddy, teve uma ideia interessante sobre o crescimento do setor de boletins informativos e a mudança do público para a comunidade. Em uma breve série de tweets, ele explica:

A década de 2010 foi marcada por plataformas de mídia social radicalmente abertas - uma bagunça gigantesca e incontrolável. Nos próximos dez anos? O pêndulo volta para as comunidades de nicho de interesse e propósito.

McIllwain continua:

Modelos de receita da comunidade: Patrocínio direto, taxas de associação escalonadas, comissões de afiliados e experiências pagas (eventos, retiros). As marcas precisam participar disso. É a mudança do público para a comunidade.

Embora existissem boletins informativos orientados por membros antes do Substack, o conceito de comunidade com acesso pago foi popularizado com o crescimento da popularidade da plataforma apoiada pelo A16Z. Assim como uma mesa em seu restaurante favorito, a comida é apenas uma parte da atração nesses ambientes, quando executada adequadamente. A outra é a ambientação e o ambiente. No 2PM, a ideia de comunidade é levada um passo adiante. A associação executiva abre oportunidades legítimas de serendipidade. Dez vezes por ano, convidamos nossos membros pagantes para um jantar de cortesia em um dos principais mercados (Nova York, Los Angeles, Chicago, Austin e Boston).

Dessa forma: as comunidades fechadas e orientadas pela mídia se tornaram o antídoto para o ruído dos lugares comuns digitais. Você verá isso em publicações como: Trapital, Petition, Off The Chain, Stratechery e Thing Testing. Em cada caso, cada fundador de mídia trabalha incansavelmente para fornecer valor aos seus membros pagantes. Uma associação é um voto para o futuro, além do presente. Há mais espaço para empresas como essas. E esses projetos geralmente começam com estratégias simples em torno de ideias originais. A esperança é que mais boletins informativos sejam lançados e que mais comunidades se formem ao redor deles. Devemos incentivar o envolvimento e a concorrência. É assim que as ideias tomam forma. O ecossistema, como um todo, é a cafeteria de hoje. Esse não é apenas o futuro da mídia, ele é emblemático de uma mudança maior à medida que a humanidade adota a cultura digital como sua.

Leia a carta de nº 343 aqui.

Reportagem de Web Smith | Editado por Carolyn Penner | Aproximadamente 2PM