NATSEC Roundtable No. 14: Civilian Drone Defense

You could say that we are incredibly privileged. We are consumers consumed by all of what makes America, America. Sports, short-form media, reality television, politics, sensational news, social division, gambling, and all of the rest. We are generally safe from the atrocities that are now common in other countries, both first world and global south.

Every industrialized nation in a position to be exposed to modern unmanned warfare has been exposed but most Americans have not. The gap between what the rest of the world’s operator class understands about drones and what the American consumer understands about drones is the largest single asymmetry in the protective equipment market today, and it is the entire opportunity.

The American consumer cannot do any of this. The American consumer has not been asked to.

At roughly 5:30 in the morning on the 28th of January in 2024, a one-way attack drone of Iranian provenance, built around Chinese commercial components and routed through the supply networks of an Iraqi Shia militia umbrella called the Islamic Resistance in Iraq, approached a logistics outpost in northeastern Jordan called Tower 22. The drone arrived at the base at almost the same minute that an American MQ-9 (drone) was returning from a routine patrol. The operators on duty could not tell the two aircraft apart; Tower 22 had air defenses but hey did not engage. The Iranian drone slipped through the layer, descended toward the container housing units where the night shift was sleeping, and detonated against the side of a connex box.

The names of the three soldiers who died that morning were Sergeant William Jerome Rivers, Specialist Kennedy Ladon Sanders, and Specialist Breonna Alexsondria Moffett. Rivers was 46 and lived in Carrollton, Georgia. Sanders was 24 and lived in Waycross. Moffett was 23 and lived in Savannah. All three were reservists assigned to the 718th Engineer Company at Fort Moore. Forty-seven other Americans were wounded; eight were casevaced. The collective public memory of the attack peaked on a Monday and was substantially gone by Friday.

The system could not distinguish between a friendly aircraft and a hostile aircraft because both of them looked roughly the same to the sensors they presented to. That is the entire problem set of modern unmanned warfare condensed to a single morning. It is also the operating condition the American consumer is about to inherit, and the American consumer is the least prepared population in the industrialized world to inherit it.

The asymmetry, stated plainly

A Ukrainian artillery officer in 2026 has more practical drone-defense literacy than the average American Fortune 500 chief executive. A Sudanese journalist on the road between El Fasher and Khartoum has more functional multispectral signature awareness than a Silicon Valley founder who pays for a private security detail. A rancher in the cartel corridors of Sonora or Sinaloa can identify the engine note of an inbound quadcopter at three hundred meters and tell you, from the pitch, whether the drone is carrying ordnance. The American consumer cannot do any of this. The American consumer has not been asked to.

This isn’t as much of a moral observation as it is a market observation. Every other large population in the world that has been exposed to drone presence at scale has produced a downstream consumer awareness, a vernacular, and a thin protective equipment market underneath it.

The Ukrainians have consumer-grade RF jammers sold openly in Kyiv electronics stores. The Israelis have IDF-surplus signature management material in regular civilian rotation. The Russians moved a third of their conscripted population through drone-defense familiarization in 2024 and 2025. The Mexicans and Colombians who live in cartel-contested territory have built informal countermeasure economies that include thermal-defeating tarps, RF detection, and trained dogs that signal on engine pitches above a certain frequency. None of this exists at scale in the United States because the United States has not, until very recently, been touched in any way – here or abroad.

The events that should have changed that have been treated as foreign news, novelty news, or UAP news.

The events we have not internalized

On the evening of the 6th of December in 2023, a fleet of drones approximately twenty feet in length and operating at speeds north of one hundred miles per hour began transiting Langley Air Force Base in Hampton, Virginia. The drones continued for seventeen straight nights. They flew south across Chesapeake Bay, across the airspace of Naval Station Norfolk (which is the largest naval base in the world), across the home base of Naval Special Warfare Development Group (Little Creek, Virginia), and back. The F-22 squadron at Langley could not engage them under existing rules of force. The incursions stopped on the 23rd of December, 2023, as cleanly as they had begun. The Pentagon has never publicly attributed them.

Roughly one year later, beginning on the 13th of November in 2024, a similar but larger pattern emerged over New Jersey. It began at Picatinny Arsenal in Morris County. It spread to New York, Pennsylvania, Ohio (including airspace closures at Wright-Patterson), Utah (Hill Air Force Base), California (Plant 42 and Camp Pendleton), and Texas (Naval Air Station Joint Reserve Base Fort Worth). By mid-December the FAA had imposed temporary flight restrictions over parts of nine New Jersey towns and the Nuclear Regulatory Commission was reporting a surge in sightings over US nuclear facilities. The Department of Homeland Security, the FBI, the Department of Defense, and the FAA collectively told the public that what they were seeing was a combination of authorized commercial drones, hobbyists, and misidentified manned aircraft. NORAD simultaneously confirmed that there had been more than six hundred unidentified drone incursions over US military installations since 2022.

The most likely explanation for the New Jersey wave, given what is now public, is that some portion of it was rehearsal by adversary services and some portion of it was tolerated commercial overflight that the existing regulatory framework had no language to describe. The actual answer matters less than the public response.

The public response was a national news cycle, followed by a Twitter cycle, followed by silence.

There was no consumer behavior change. There was no protective equipment purchase wave. There was no demand on Congress to update the statutes that prevent counter-UAS engagement over civilian airspace. The signal moved through the discourse without leaving a residue.

This is the population that is going to be exposed at scale in the next thirty-six to eighty-four months. We are extraordinarily soft.

How the sensor stack got here

The history of armed drone warfare in the post-Cold War period is, fundamentally, a history of capability migration from state monopoly to commercial availability, compressed across roughly twenty-five years.

The Central Intelligence Agency armed its first MQ-1 Predator with Hellfire missiles in late 2001. The first targeted killing using that system occurred in Marib Governorate, Yemen, on the 3rd of November in 2002. The capability was, at that time, a sovereign capability of one nation. It cost in the high tens of millions of dollars per system, required a satellite link and a CONUS-based pilot to operate, and was sustained by an industrial base that the United States and a small number of close partners exclusively held.

Twenty-two years later, on the 1st of June in 2025, the Ukrainian Security Service ran Operation Spiderweb, in which a swarm of small commercial-component drones launched from concealment positions inside Russia destroyed a substantial fraction of Russia’s strategic bomber fleet, including Tu-95 and Tu-22M3 airframes that the Russian state cannot replace at scale. The drones were assembled in a garage. The total cost of the operation was a rounding error against the value of what it destroyed. The capability that twenty years earlier had required a sovereign intelligence service had migrated to a determined non-state actor or sub-state intelligence cell with a parts list and a parking lot.

In between those two endpoints, the milestones are dense and consistent. The Houthis crippled five percent of global oil production with a Saudi Aramco drone strike in September 2019. The Venezuelan opposition attempted to assassinate Nicolas Maduro with two DJI Matrice 600s carrying C-4 at a military parade in Caracas in August 2018. Azerbaijani Bayraktar TB2s decimated Armenian armor in the forty-four day war over Nagorno-Karabakh in late 2020, which was the moment that any serious military observer understood the doctrinal shift had arrived. The Israeli operation against Iran in June 2025 included drone components prepositioned in Iranian territory for months before activation. The cartel use of armed quadcopters in Michoacán and Tamaulipas is now constant enough that the Mexican military has its own drone-defeat schools. The Sudanese RSF runs a drone-buy program through Wagner-adjacent supply lines that puts dozens of strike-capable platforms a month into a non-state actor’s hands.

None of this is exotic.Actually, most of this technology stack is consumer-grade. The CV models doing the targeting are YOLO derivatives, the same person-detector that runs on a Raspberry Pi for backyard security cameras. The thermal cores are FLIR Lepton modules, sold openly. The flight controllers are Pixhawk. The mesh networks are off-the-shelf 2.4 and 5.8 GHz. The military-grade version of any of this leads the commercial version by roughly two to three years. That is the timeline a consumer defense category needs to be ready for, and it is the timeline that the existing tactical apparel and surveillance avoidance markets are not built for.

What the sensor stack actually does, and what it does not do

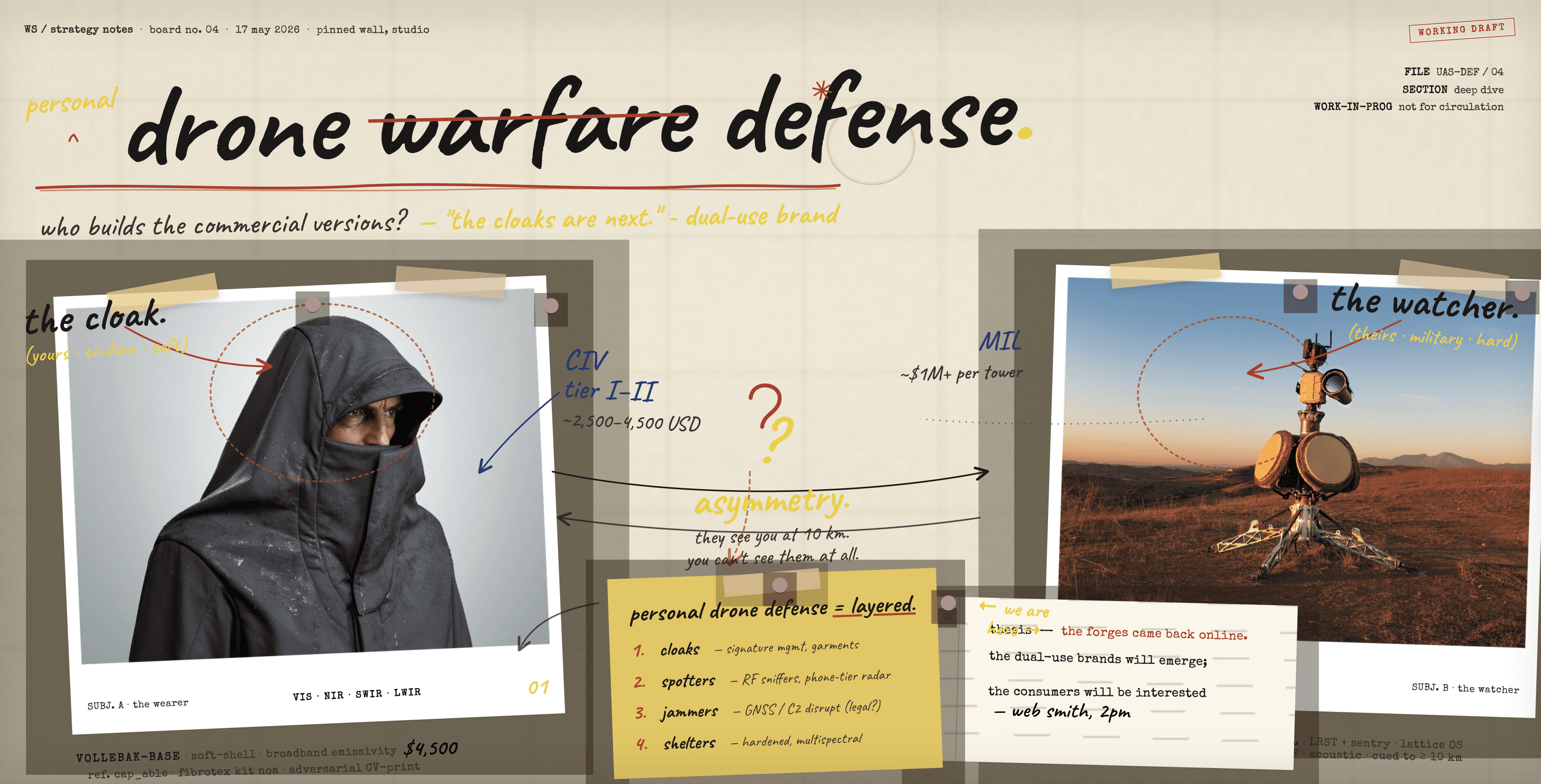

The threat surface that a personal protective system has to be built against is not “drones.” It is the sensor stack that drones present.

Commercial and prosumer platforms, which is the realistic personal threat through 2028 or 2029, target via electro-optical first, longwave thermal second, and navigate by GPS with visual-inertial backup. The CV layer is doing person-detection at the model level. The control link is on 2.4 or 5.8 GHz. The platform leaks RF in characteristic ways that are documented and detectable. Military-grade systems extend this with SAR, RF emission targeting, and multispectral fusion across the near-infrared, short-wave infrared, mid-wave infrared, and long-wave infrared bands, but the dominant near-term threat is the commercial layer.

The defensive doctrine that emerges from working backward from this stack is, in order: detection, concealment, deception, disruption, and hard kill.

Most personal anti-drone thinking jumps directly to disruption, which is the layer that is least available to a civilian buyer and least useful even when it is available. The eighty percent of survivability sits in the first three layers, which is the part of the doctrine that no consumer brand currently sells coherently.

Detection is RF awareness. A passive spectrum scanner tuned for the ISM bands picks up DJI, Autel, and most prosumer control links at ranges of several hundred meters. The hardware is software-defined radio at this point. The consumer-grade unit costs less than a decent pair of running shoes. The institutional-grade unit (the DroneShield RfPatrol Mk2, currently sold into military and executive protection channels) does this at higher fidelity with a maintained signature database. Knowing that a drone is in your area before it has imagery of you is the single highest-leverage capability in the entire stack.

Concealment is multispectral signature management. The standard wool blanket and Mylar bivy approach that defines the consumer survival market is binary and self-defeating. A reflective bivy blocks thermal entirely, which creates a cold anomaly against ambient that is, in some conditions, more identifiable than the human body it was supposed to be hiding. What modern signature management does is broadband emissivity matching to background. The defense industry product is the Fibrotex ULCANS netting that is now the US Army’s standard concealment kit, and its personal-scale analogs (Kit Noa, Saab’s Special Operations Tactical Suit).

The consumer version of this category does not exist yet at any kind of brand scale. Building it is the opportunity. I want to.

Deception is adversarial computer vision. The Italian fashion-engineering firm Cap_able has been shipping knitwear since 2023 with adversarial patches woven directly into the textile that misidentify the wearer to YOLO at approximately sixty percent rates under published testing. A frontier paper from November 2025 demonstrated thermally-activated dual-modal adversarial clothing that maintains above-eighty-percent attack success across both the visible and infrared bands simultaneously. The research is twelve to twenty-four months from a productized form factor.

Whoever ships the first dual-modal adversarial garment that does not look like a research artifact will define the consumer category aesthetic for a decade.

Disruption is where the public imagination collides with the legal and physical limits of the civilian channel. DIY EMP devices at man-portable scale are ineffective, dangerous to the operator, or illegal under FCC Part 15 and 18 U.S.C. § 1362, often all three simultaneously. The commercial counter-UAS systems that defeat drones at meaningful range (Epirus Leonidas, the Anduril Anvil, BAE Bofors) are crew-served, vehicle-mounted, and tightly export-controlled for entirely sensible reasons. Active RF jamming hardware is restricted to government and critical infrastructure customers in the United States and most of NATO. The civilian disruption layer is, honestly, passive RF detection plus operational discipline. Any brand that pretends otherwise is a liability rather than a category leader.

Hard kill at personal engagement range is a shotgun, the specialty loads exist. Effective range is thirty to forty meters against prosumer quadcopters with the right shot column. Net guns and SkyWall-class systems extend the range with no kinetic risk to bystanders but are slow, single-shot, and priced for facility security rather than personal use. Against a swarm of any meaningful size, hard kill is a last-resort interrupt for the one or two units that defeated the upstream layers. It is not a primary defense and should not be marketed as one.

The current consumer market is theater

What exists today for civilian buyers in the United States who are awake to this threat surface is a fragmented catalog of products positioned for the wrong customer. The tactical apparel brands selling “stealth hoodies” against thermal are selling cotton with a marketing budget. The Faraday-pouch market is mostly legitimate but positioned for crypto-paranoia and Faraday-as-EMP-protection rather than as one layer of a coherent personal signature management system. The YouTube ecosystem selling DIY capacitor-bank EMP devices is selling personal injury claims. The military surplus channel has the actual physics-validated material (Fibrotex panels, Saab MCS components, IDF-surplus thermal-disruptive material) but no consumer brand, no fitting guidance, no integration, and no marketing that speaks to anyone who is not already inside the operator subculture.

What the market does not have is the brand that does for personal signature management what Patagonia did for technical outerwear in the 1980s, what Yeti did for coolers in the 2010s, or what Athletic Greens did for daily supplementation in the late teens.

The category requires a premium consumer brand that takes the physics seriously, builds an integrated product line, prices it at the upper end of the technical apparel market, and uses long-form content as the primary acquisition channel. The content is half of the moat. The buyer for this category is a reader. They read SOFREP, they listen to Cleared Hot, they subscribe to War on the Rocks, they may even read 2PM on ocassion. The brand that wins this category will be the brand that publishes the field manual that defines the category before anyone else has the language for it.

The civilian stack you can actually build, today

The tables below are what an informed civilian buyer in the United States can actually acquire in 2026, assembled from existing brands, with gaps marked where the consumer category does not yet exist and the operator has to substitute or improvise.

Tier I. Foundation ($600 to $900)

The minimum coherent stack. Closer to insurance than to operational kit.

| Component | Product | Approximate Cost |

|---|---|---|

| RF detection (handheld passive scanner) | RF Explorer 6G Combo or 3G Combo | $269 to $399 |

| Faraday phone pouch | Mission Darkness Faraday Bag | $25 |

| Faraday laptop or tablet sleeve | Mission Darkness Non-Window Faraday Bag XL | $60 |

| Adversarial CV garment | Cap_able knit hoodie (Manifesto Collection) | $250 to $400 |

| Mylar contrast-break panel (static use only) | Heatsheets Survival Bivy | $15 |

Tier II. Operator ($2,800 to $4,500 additional)

The functional stack. This is what a civilian buyer who treats personal signature management as a real protective category should be running.

| Component | Product | Approximate Cost |

|---|---|---|

| Personal multispectral concealment | Snipers Hide ThermaShield poncho or surplus ULCANS panel | $200 to $600 |

| Multispectral hide-site netting | Tropic Concealment Solutions or surplus ULCANS Kit Sophia | $400 to $1,200 |

| Thermal-disruptive base layer | Wild Things Tactical Heavy Weight Polartec or equivalent | $200 to $400 |

| Outer ghillie augmentation | Red Rock Outdoor Gear base + local-flora additive | $80 to $150 |

| Spectrum analyzer (upgrade from RF Explorer) | Aaronia Spectran V5 or V6 | $1,200 to $2,500 |

| Directional antenna | Aaronia HyperLOG or OmniLOG | $200 to $500 |

| Tactical Awareness Kit hardware | Samsung Galaxy S-series running ATAK | $400 to $900 |

| Comprehensive Faraday integration | Mission Darkness CYBER Faraday Bag set | $150 |

Tier III. Maximum civilian capability ($5,000 to $12,000 additional)

The ceiling of what a civilian buyer in the United States can legally acquire and operate. Above this tier the products are restricted to government, critical infrastructure, or executive protection contracts.

| Component | Product | Approximate Cost |

|---|---|---|

| Passive wearable C-UAS detector | DroneShield RfPatrol Mk2 (executive protection channel) | $4,000 to $8,000 |

| Vehicle multispectral camouflage | Surplus or commercial MCS panels | $1,500 to $3,500 |

| Hard-kill platform | Beretta 1301 Tactical or Mossberg 590A1 | $700 to $1,500 |

| Anti-drone specialty loads | Drone Munition or Skynet Mi-5 | $100 to $200 per case |

| Net launcher (non-lethal interrupt) | SkyWall Patrol or civilian net gun equivalent | $500 to $5,000 |

| Thermal imager (situational awareness only) | Pulsar Helion 2 XP50 Pro or Bering Optics Hogster | $2,500 to $4,500 |

The three gaps the market has not closed

Three product categories do not exist for the American consumer in any form that an experienced operator would respect. Each is a build opportunity for whoever wants to define the category before the catalyst event arrives.

The first is a multispectral concealment garment system built for the civilian body type, sized like outdoor apparel, branded for the buyer who is not in uniform, and priced at the upper end of the technical outerwear category. Fibrotex Kit Noa is the physics reference; Patagonia is the merchandising reference. The synthesis has not been done.

The second is a passive wearable RF detector at a consumer price point, branded for civilian executive protection and outdoor recreation use, paired with a companion mobile app. DroneShield owns the institutional channel. There is no civilian-channel equivalent priced below $1,500, and the buyer who would pay $499 for a respectable handheld unit numbers in the hundreds of thousands today.

The third is a dual-modal adversarial garment that defeats both visible-band and infrared computer vision simultaneously, in a form factor that reads as outdoor or urban apparel rather than science experiment. The research exists as of November 2025 but the product does not. Whoever ships it first will define the visual identity of the category.

Marketing the category

The brand that wins this market will sound like nothing currently in the tactical category and very little in the technical outdoor category. The voice has to read as competent, calm, and operator-adjacent without leaning into the cosplay aesthetic that defines most of the existing tactical apparel market.

Think of how Vollebak markets apparel for what they call “the next hundred years.” Think of how Triple Aught Design wrote about urban operating environments fifteen years before the rest of the market caught up. Think of how Outlier sells four-figure technical apparel with no military framing at all. The aesthetic is technical, restrained, photographically dark, and the copy treats the buyer as someone who has already done the homework.

Three positioning vectors will work. The first is continuity, which is the language of buyers who want to keep doing what they have been doing (running, ranching, traveling, working in austere environments) in conditions that have changed underneath them. The second is autonomy, which is the language of buyers who recognize that institutional security infrastructure has degraded and the burden has moved to the individual. The third is stewardship, which is the language of buyers who are protecting other people (family, team, principal) and need the equipment to perform without them being the most technical person in the room.

The acquisition channel is content first, retail second, direct-to-consumer eCommerce as the operating infrastructure. The brand will be built on a publication, a podcast, or a newsletter before it sells a single unit. The Athletic Greens model applies directly. The brand that wins this category will spend the first eighteen months publishing the field manual that the buyer trusts before the buyer is ready to spend $3,000 on integrated kit.

That is the moat.

The cost ladder

The retail price ladder, when this category is built correctly, lands at four tiers.

Entry ($249 to $499). The single garment or single device that earns the buyer’s trust and establishes the brand. This is the adversarial hoodie, the high-end Faraday kit, the consumer RF detector. It is also the gift purchase, the gateway purchase, the trial purchase.

Core ($999 to $2,499). The integrated personal kit. Multispectral cloak, thermal-disruptive base layer, RF detector, Faraday kit, integration accessories. The buyer at this tier has made the decision to treat the category as real.

Expedition ($4,999 to $9,999). The full operator-grade civilian stack. Adds the upgraded spectrum analyzer, hide-site netting, ATAK-integrated hardware, the optional thermal imager.

Bespoke (custom). The family or executive protection package, custom-fit, custom-configured, sold through a consultative channel. This tier carries the margin. The first three build the brand that earns the right to sell the fourth.

Gross margin on the core tier should land at sixty to sixty-five percent. On the bespoke tier, eighty percent is achievable. The unit economics work in the same way that Yeti’s worked when they moved from a single cooler SKU to a product system, and the way Patagonia’s worked when they moved from technical jackets to integrated outerwear. The category does not get built one product at a time. It gets built one customer cohort at a time, and the right cohort is willing to spend at retention rates that look like Patagonia rather than Amazon.

The build I am testing

The personal stack I am testing sits at the upper end of Tier II, with selective additions from Tier III where the gear is legally available to a civilian buyer in Ohio. The RF Explorer goes in the running pack. The Cap_able piece sits in regular outerwear rotation. The ThermaShield and the Tropic Concealment net sit in my garage. The Mission Darkness Faraday kit is already integrated into the daily-carry rotation for the phone and the Yubikey. The DroneShield RfPatrol acquisition is a longer process given the institutional channel, but the path exists through executive protection resellers and through the defense ecosystem relationships that the 2PM editorial work has produced.

The reason to build it now is mostly editorial. The category is coming whether the American consumer is ready for it or not, and the publication that has a credible operator perspective on it from inside the build will define the conversation for the next thirty-six months.

The Forges Went Dark established that the manufacturing side of the dual-use shift was real and that the reshoring underneath it would not be reversed. This is the protective equipment side of the same shift, pointed at the buyer rather than the contractor. The brands that arrive first will be the brands that are still here when the rest of the market figures out it is a category.

If and / or when

The catalyst event that ends that conviction is not a question of whether. It is a question of which. A drone incident at a Super Bowl. A coordinated swarm at a presidential inauguration. A paparazzi drone that kills someone famous. A cartel drone strike that crosses the Rio Grande and kills a sheriff. An attributable Chinese or Iranian incursion that the public cannot un-know. Any one of these flips the category from niche-premium to mass-aware in a single news cycle. The work to do is to be the brand that defined the language before that next morning.

韦伯-史密斯的研究与写作

Afterword: Acronyms and terminology

The vocabulary of unmanned warfare and signature management has been built largely inside defense and intelligence institutions, and it is not yet in common civilian use. The terms below appear in the essay above and across the broader literature.

| Term | Expansion | What it means in practice |

|---|---|---|

| ATAK | Android Team Awareness Kit | Government-developed situational awareness app, originally for special operations, now available in a civilian variant (CivTAK). |

| AEO | Answer Engine Optimization | The discipline of making content discoverable by AI answer engines rather than traditional search. |

| CONUS | Continental United States | Used to distinguish operations or personnel located inside the lower 48 from those forward-deployed. |

| C-UAS | Counter-Unmanned Aerial Systems | The product and doctrine category for detecting, tracking, and defeating drones. |

| CV | Computer Vision | The machine-learning subfield that handles image recognition and object detection, including person-detection on drones. |

| DTC | Direct to Consumer | A commerce model in which the brand sells directly to the end customer without retail intermediaries. |

| EMP | Electromagnetic Pulse | A burst of electromagnetic energy capable of disabling electronics. Effective at scale only via nuclear detonation or large directed-energy systems. |

| EO/IR | Electro-Optical / Infrared | The dominant sensor pair on commercial and military drones, covering visible light and thermal bands. |

| FPV | First-Person View | A drone control mode in which the pilot sees through a camera on the drone in real time. The dominant attack drone format in Ukraine. |

| GNSS | Global Navigation Satellite System | The umbrella term for GPS and its international counterparts (GLONASS, Galileo, BeiDou). |

| HaaS | Hardware as a Service | A commercial model in which the customer subscribes to a hardware capability rather than purchasing the unit outright. |

| HEL | High Energy Laser | Directed-energy weapon class used in some emerging counter-UAS systems. |

| HPM | High Power Microwave | Directed-energy weapon class that disables electronics across a wide area. Epirus Leonidas is the visible US example. |

| INS | Inertial Navigation System | A self-contained navigation method that does not require external signals like GPS. |

| ISM band | Industrial, Scientific, Medical band | The unlicensed radio frequency bands (notably 2.4 GHz and 5.8 GHz) used by most commercial drone control links and Wi-Fi. |

| ISR | Intelligence, Surveillance, Reconnaissance | The military function of collecting information on adversaries or environments. Most modern drones are ISR platforms first. |

| LWIR | Long-Wave Infrared | The thermal band (roughly 8 to 14 micrometers) in which human bodies are most distinctive against ambient. |

| MCS | Mobile Camouflage System | Multispectral concealment material designed to be applied to vehicles or platforms in motion. |

| MGRS | Military Grid Reference System | The grid coordinate system used in military and ATAK environments. |

| MWIR | Mid-Wave Infrared | Thermal band (roughly 3 to 5 micrometers) used by higher-grade military sensors. |

| NATSEC | National Security | The institutional and commercial sphere oriented around defense, intelligence, and homeland security work. |

| NIR | Near Infrared | The first non-visible band beyond red light. Used by night-vision systems and some agricultural sensors. |

| NORAD | North American Aerospace Defense Command | The joint US-Canadian command responsible for aerospace warning and control over North America. |

| NORTHCOM | United States Northern Command | The US combatant command responsible for homeland defense. |

| POS | Point of Sale | Retail terminology for the system that processes transactions at the moment of purchase. |

| SAR | Synthetic Aperture Radar | A radar imaging technique that produces high-resolution imagery in all weather, day or night. |

| SDR | Software-Defined Radio | A radio system whose signal processing happens in software rather than fixed hardware. Underpins most modern RF detection. |

| SWIR | Short-Wave Infrared | Thermal band (roughly 1 to 3 micrometers) that penetrates haze and some forms of visual camouflage. |

| UAS / UAV | Unmanned Aerial System / Vehicle | The formal terms for what most people call a drone. UAS refers to the full system including ground station; UAV is the aircraft itself. |

| UV | Ultraviolet | The band of the electromagnetic spectrum above visible light. Used by some sensor stacks and certain camouflage detection systems. |

| YOLO | You Only Look Once | The dominant real-time object detection model family. The de facto person-detector on commercial drone targeting systems. |

Further reading from 2PM: The Forges Went Dark. For corrections, additions, or off-record discussion of the category, the contact channel is the usual one.

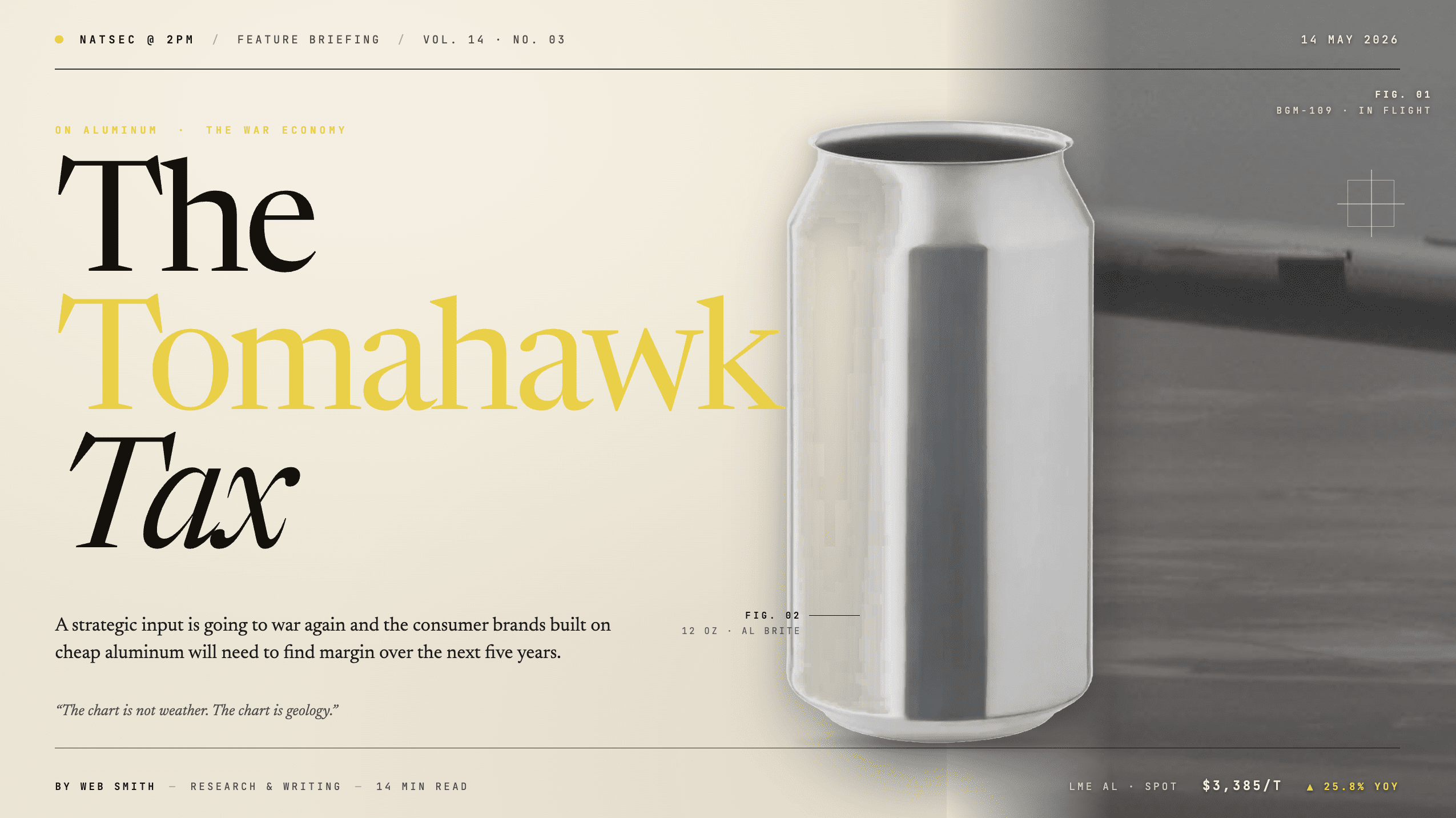

Memo: The Tomahawk Tax and Sparkling Water Can

On aluminum, the war economy, and the consumer brands that will not survive the next five years. This essay is a feature post for the NATSEC @ 2PM briefing series.

I was in the Carolinas, earlier, when the conversation in a small meeting turned to aluminum, and not in the way it turns at a beverage conference. This was not packaging weight, sustainability narrative, or the standard pieties of the can. The room was a small one, a glass table and the kind of muted hospitality that signals money is in the process of being moved, and someone at the end of the table, defense-adjacent in the way that certain operators are now, laid out what they were modeling on a five to seven year horizon. The following was attributed and cleared accordingly.

The model was designed against a thinned smelter base, munitions replenishment, allied stockpiles, the per-unit aluminum content of a Tomahawk against a Patriot interceptor against a loitering munition flown out of a shipping container by a defense-technology startup that did not exist in 2019.

The horizon, a word repeated more than once, was five to seven years.

I have heard a lot of forecasts in commerce, and most of them are a performance of optimism for an audience that has already paid to hear them. This one was not. It was the math of a strategic input being absorbed by a buyer that does not negotiate, on a timeline long enough to matter and short enough to act on, and I have not stopped thinking about a twelve ounce can since.

The story has a shape, and the shape is older than the industry it threatens.

The Read From the Chart

The number, as of the most recent close on the London Metal Exchange, is roughly $3,385 per tonne. The chart on Trading Economics is a four-year line of memory: an all-time high of $4,103 in March of 2022 when Russia entered Ukraine and a different commodity scare ran through the global supply, a long drift through the back half of 2023, and a steep ascent through 2025 and into the first quarter of 2026 that has carried the price up 25.84 percent against the same week last year and up 9.14 percent against the prior month. The same model puts the twelve month forward at approximately $3,616 per tonne, which is to say within reach of the 2022 high.

Three forces are pulling on the chart, and they are not the kind of forces that resolve themselves through a single quarter of resupply.

The first is acute and geopolitical. In March, Iran struck targets across all six Gulf Cooperation Council states in what the United States and Israel have referred to as Operation Epic Fury, and the operational consequence for global aluminum has moved faster than the consumer press has reported. Qatar halted its joint refinery operation with Norsk Hydro, Bahrain’s Alba declared force majeure on all deliveries, and roughly ten percent of global primary supply now sits in a region operating under siege conditions, with LME and COMEX inventories already near record lows before the strike package was authorized. The market response was not panic. The market response was reprice, and the reprice has held.

The second force is structural. China, which produces approximately sixty percent of the world’s primary aluminum, has imposed an annual production cap of 45 million tonnes, a self-imposed ceiling designed to manage overcapacity and the carbon profile of its heavy industrial sector. Indonesia, which has been the consensus answer to the question of marginal capacity, is constrained by energy costs and by a regulatory regime that has made greenfield smelting more difficult rather than less. There is, in other words, no swing producer of consequence, and the absence of one is the condition the market is now pricing.

The third force is political and domestic. The fifty percent tariff on imported aluminum, including imports from Canada, which has been the largest source of beverage-grade can stock in North America for decades, passes through to packaging in the kind of penny increments that look modest on a slide and feel structural on a profit and loss statement. Zevia, which is publicly traded and therefore obligated to disclose what private competitors can keep quiet, has booked an incremental $5 million in 2026 aluminum costs attributable to tariffs alone. That is one mid-cap brand making one disclosure on one quarter, and the disclosure scales across a category that has been built on the assumption of cheap, abundant, recyclable, infinitely available aluminum.

The chart is telling operators something the salesforce cannot, and the operators in the Carolinas were listening to it.

A Reminder From 1941

The first time aluminum became geopolitics, it nearly cost the United States the war, and the history is worth a careful read because the architecture of the problem is more familiar than the trade press tends to remember.

In 1939, Germany was the world’s leading producer of primary aluminum, and the Reich had built that capacity through a combination of domestic investment and cartel agreements to which Alcoa, the American monopolist of the period, had been at least a tolerant participant. R. S. Reynolds, the foil entrepreneur, traveled to Europe in the same year, saw what he saw, and came home alarmed enough that he mortgaged his existing foil plants to fund new smelters in Listerhill, Alabama and Longview, Washington, because he could not move Washington fast enough to do it for him.

By the time of Pearl Harbor, the United States had a problem the records describe in plain language. Glenn L. Martin required roughly 16,000 pounds of aluminum to build a single medium bomber. President Roosevelt’s plan called for 50,000 aircraft per year. That math required 400,000 tonnes of capacity, and Alcoa had committed to 187,500. The Secretary of the Interior at the time, Harold Ickes, told the press, plainly, that if America lost the war it could thank the Aluminum Corporation of America.

What followed is the part of the story that the contemporary business histories tend to skip, and it is the part that matters most for the present analysis. The federal government did not negotiate with the monopoly; it built around it. The Defense Plant Corporation broke ground on three new smelters in the Pacific Northwest, the Bonneville Power Administration appropriated $2 billion to multiply the generating capacity of the Columbia River hydroelectric system by a factor of six, and one well-cited estimate credits Grand Coulee power alone with producing the aluminum in one-third of the American aircraft built over the course of the war. Reynolds, using a Norwegian process that Alcoa had refused to license under cartel discipline, added 450,000 tonnes of capacity inside U.S. borders during the war years, and Aluminium Limited added another 300,000 in Canada. By 1941, U.S. primary production had crossed one million tonnes for the first time in history, and by 1945 the Supreme Court had ruled that Alcoa had monopolized the American market and ordered its remedy.

The lesson, preserved in the institutional memory of the Office of the Secretary of Defense industrial base shop and in a small handful of business school case studies, is that aluminum is not a commodity in the way that wheat is a commodity. It is a strategic input, and when the country requires it, the country acquires it. The price you pay for a can is the residual of what the country did not need in a given quarter, and that residual is the variable that the operators in the Carolinas were attempting to model.

We are about to relearn the lesson, and the relearning is already underway.

The Replenishment

The Pentagon’s Munitions Acceleration Council, which is a body that did not exist three years ago, issued a memo at the end of April naming fourteen “critical” munitions for fast-tracked, multiyear procurement, and the list reads like the inventory of a campaign that has been spent down to the studs. Twelve of the fourteen are legacy systems: Patriot PAC-3, Standard Missile-3 Block IB at $896 million for fifty-two missiles and components, Standard Missile-6, Tomahawk in two variants, AMRAAM, JASSM, LRASM at $473 million split across the Air Force and the Navy, and THAAD. The remaining two are emerging systems: a low-cost containerized cruise missile program in which Anduril, CoAspire, Leidos, and Zone 5 will collectively produce more than 10,000 units beginning in 2027, and Castelion’s hypersonic Blackbeard, contracted under terms that require a minimum of 500 missiles per year once testing validates.

The 2026 spending bill funds the list at $6.3 billion, which is $1.9 billion above the administration’s original request, with multiyear procurement authority running through fiscal year 2032. Another $500 million is appropriated for solid rocket motor industrial base expansion, workforce development, and supplier qualification. An additional $2 billion was added to the $25 billion reconciliation tranche allocated last summer. The total U.S. defense budget for 2026 is approaching $1 trillion, which is approximately 39 percent higher than 2021, and NATO defense expenditure is now estimated at $1.4 trillion. None of these numbers, on their own, are surprising to anyone who has been watching the geopolitical situation since 2022. The interaction of these numbers with a strategic input that the market has just repriced by roughly twenty-five percent year over year is a different conversation, and it is the conversation that the consumer category is not yet having.

A Tomahawk uses aluminum. A Patriot interceptor uses aluminum. A loitering munition is, in structural terms, a lightweight aluminum airframe wrapped around a warhead, an electronics package, and a battery. Every drone in the autonomous fleet that the defense-technology investor class has been funding requires aluminum, and the new low-cost containerized cruise missile program has been deliberately designed for affordable mass, which is the contracting term of art for thousands of units per year of an airframe whose cost basis is structurally a function of aluminum, electronics, and propellant.

Mark Cancian at CSIS has placed the production timeline at three to four years before output meets demand, and until then, allied procurement runs behind U.S. requirements rather than alongside them. The Gulf states want their air defenses replenished, Ukraine still wants Patriots, Japan wants Tomahawks, and Europe is mobilizing its own production base under the European Defence Fund. The aluminum coming out of a Bahrain smelter under siege conditions is not coming to a beverage can factory first, and it is not coming second either.

Where the New Money Has Gone

The second leg of the squeeze is capital, and the magnitude of the reallocation has not been adequately metabolized by the consumer commerce press.

Venture capital deployed approximately $49.1 billion into defense technology in 2025, which is nearly double the $27.2 billion deployed in 2024 and the largest annual figure that PitchBook has recorded. U.S. equity funding in the sector tripled to $14.2 billion, with American startups capturing the lion’s share of the global pool. Manufacturing-focused defense investment, which is the unsexy capex layer where smelting capacity and forging lines and CNC throughput live, rose to $4.7 billion across 39 deals, up from $2.6 billion across 24 deals the prior year. Defense-technology exits hit a record $54.4 billion, more than triple the $18.2 billion of 2024, and most of the exit volume cleared through acquisitions rather than public offerings.

The headline rounds are familiar to anyone who has been reading the NATSEC @ 2PM briefings over the past eighteen months. Anduril raised $2.5 billion in June at a $30.5 billion valuation. Saronic raised $600 million for uncrewed maritime systems. Helsing raised $694 million in Germany. Hadrian, the defense-manufacturing startup, took $260 million from Founders Fund and Lux Capital. Castelion, which most consumers have never heard of, has just signed a Pentagon agreement that obligates a minimum 500-missile annual production rate. The pattern is consistent, the capital is patient, and the policy environment is catching up to the capital rather than the other way around.

The argument that 2PM has been making across the Drop Economy essay and the dual-use thread that preceded it is the argument that matters here. The same Silicon Valley funds that wrote consumer brand checks in 2021 are writing defense manufacturing checks in 2025, and the operator talent that built growth-stage consumer brands is being recruited into defense operations and ground-truth manufacturing roles. Capital is finite, attention is finite, and operator bandwidth is finite. The reallocation is already complete in the rooms that matter, even if the trade press has not finished reporting it.

The downstream consequence for the consumer category is straightforward. When a tier-one venture fund leads a $260 million Series C in a defense manufacturer at a clearing multiple, the same fund’s limited partners reset their expectations across the rest of the portfolio. Premium consumer brands with thin margins, soft moats, narrative-led positioning, and no defensible distribution are no longer the asset class. They are the cautionary tale told at the limited partner meeting, and the well-funded brands have already absorbed this and adjusted their internal messaging accordingly. The brands that have not absorbed it are still printing pitch decks that assume a 2021 capital environment.

The Math of the Can

It is worth running the numbers cleanly, with every operator anonymized, because the math is unambiguous and the math is where the conversation should be moving.

A twelve-ounce aluminum can, sold in volume to a beverage brand under a long-form supply agreement, has historically priced somewhere between 10 and 13 cents for the empty can itself, with sleek and slim formats running slightly higher and standard formats slightly lower. Add fill, label, contents, freight, and slotting, and the fully loaded cost of goods on a single unit lands somewhere between 25 and 35 cents, depending on the brand’s scale and the terms of its co-packing relationships. Packaging, taken together across aluminum, glass, and plastic, accounts for roughly one-third of total raw material cost in beverage manufacturing, and aluminum is the largest single line within packaging for a sparkling water brand built on the slim can format.

A premium sparkling water brand sells to a major grocery account at somewhere between 55 and 75 cents per unit at wholesale, with co-packer and distributor margin layered in. Direct-to-consumer pricing on a 24-pack runs between $30 and $48, which is $1.25 to $2.00 per unit on the retail face, with freight and last-mile fulfillment absorbing most of the apparent premium. Gross margins at wholesale run between 35 and 50 percent on a good quarter, and at DTC between 50 and 65 percent on the contribution line before customer acquisition cost.

A 25 percent rise in aluminum, holding all other inputs equal, adds roughly 3 cents to the cost of a single can. On a 65-cent wholesale unit, that is four to five percentage points of gross margin compression. If aluminum tracks the Trading Economics twelve-month forward and adds another seven percent on top of where the chart already sits, the compression deepens to five to seven points by the middle of 2027, which on a brand operating at a 38 percent wholesale margin amounts to approximately fifteen percent of gross profit erased before a single dollar of customer acquisition spend has been deployed.

For omnichannel sparkling water, which is to say the brands selling 24-packs into apartment doorsteps in coastal metropolitan markets, the compression is structurally worse rather than better. Freight is itself aluminum-adjacent in the sense that trucking, fuel, and corrugated packaging all carry their own inflation profiles, and the DTC consumer base is the segment most willing to trade down at the moment that price moves on the digital shelf. Premium DTC sparkling water as a category has never had pricing power in the way that Poppi or a small handful of cult-coded competitors have had pricing power. It has had narrative power, and narrative power compresses faster than COGS does when the underlying input is no longer underwriting the deck.

Three Anonymized Archetypes

Brand A is well-capitalized, holds national distribution, has dominant shelf presence at scale, and has hedged aluminum forward through structured supply agreements with its can converter. The brand has the volume to negotiate sleeve pricing on cans, the operator depth to manage co-packer leverage actively, and the marketing efficiency to absorb a one to two point gross margin hit through promotional rationalization rather than retail price. Brand A will look fine on the next earnings call and the call after that, and Brand A will quietly acquire one or two distressed competitors in 2027 at multiples that look like opportunism in retrospect.

Brand B is mid-tier, venture-funded, operating somewhere between $40 million and $80 million in revenue, with premium DTC and natural channel presence. Brand B has four to six months of can inventory on the books and a co-packer contract that resets in the third quarter. The brand’s pitch deck has, for the last two raises, shown a path to 65 percent contribution margin at scale, and the deck does not survive contact with aluminum at $3,600 per tonne. The next raise will be a flat or down round if it happens at all, or a strategic sale to a category platform, or, in the most common case, a tightening exercise that ends in a retrenchment from DTC and a return to wholesale at lower velocity and tighter terms. Some of these brands will not raise at all, and some will burn down to a sale that the press release will describe in flattering terms even when the deal terms are not.

Brand C is indie, founder-led, operating between $3 million and $11 million in revenue, premium-positioned without institutional capital. The math at Brand C is the cleanest and the most brutal. Without scale leverage on can pricing, without hedging, and without a Series B war chest, Brand C either pivots to a higher-margin product extension, which is to say powders, concentrates, functional ingredients, or formats other than the slim aluminum can, or it does not exist in any commercially meaningful form by 2028. The brands at this tier that exercise fiscal discipline will pivot, and the brands that have been operating on aesthetic alone will not. The acquisitions at this tier will be few, and they will not be flattering. Strategic buyers do not pay premium multiples for compressed-margin businesses in categories they already understand, and the exits, where they happen, will be classified as talent-and-IP acquisitions rather than as category roll-ups.

Who Survives the Next Five Years

The survival profile of the category, looking out across the procurement window the Pentagon has now made explicit through 2032, is legible enough to plan against, and the planning is the point of this essay.

The brands that survive will share four characteristics, and the characteristics compound on each other in the way that brand defensibility compounds across the moats that 2PM has been mapping for the better part of a decade.

The first characteristic is structural cost advantage, which means scale, vertical integration, or proprietary formulation that allows the brand to move at least part of its volume out of pure aluminum dependency. The energy drink houses that already own their can supply contracts qualify, the functional beverage brands building in formats other than the standard twelve-ounce slim sleeve qualify, and the hybrid-format players who can shift between can, glass, bottle, and powder without rebuilding the line qualify.

The second characteristic is real pricing power, which is less common than the founder decks claim and which has very little to do with the price the brand currently charges. Real pricing power means that the consumer will not trade down if the brand raises retail by ten percent, and the test for pricing power is the cultural meaning, ritual context, or flavor specificity that a competitor cannot replicate. Most premium sparkling water does not pass the test. The category has taste, which is a substitute for pricing power until the substitute becomes too expensive to maintain.

The third characteristic is distribution moat, which is rare and getting rarer as retailers consolidate their own private-label sparkling water programs to capture exactly the contribution margin that a national brand can no longer hold. The brands that own the cold case, the route, the cooler placement, or a category captaincy at a grocery banner are the brands that will be permitted to absorb input inflation without losing shelf, and the brands that depend on shelf rental are not.

The fourth characteristic, which 2PM has been arguing across the Universal Commerce Protocol work in January and across the Drop Economy work in April, is the editorial and retrieval layer that the AI age now requires. The brand that controls the vocabulary that the answer engines use to describe a category will own that category through the procurement window, and the control is built through editorial discipline, narrative density, and community signal rather than through performance marketing spend. Palantir is a defense and data company that has built a Shopify storefront operating as an investor relations channel that happens to accept Apple Pay, and the brand has earned more cultural coverage in eighteen months than most CPG operators earn in a decade.

The infrastructure that made it possible is the same infrastructure that powers any merchant on the platform. The lesson is not that a sparkling water brand should sell defense merch, and the lesson is not that a sparkling water brand should pivot to drone parts. The lesson is that editorial control of the answer engine layer compounds across exactly the kind of category compression cycle the next five years will deliver, and the brands that build the layer now will be the brands that the AI describes to a future customer who has not yet typed the question.

The Verdict

Is the squeeze coming. Yes, on the procurement schedule the Pentagon has already published, with the capital flows the venture data has already confirmed, and against the chart that is sitting on Trading Economics for anyone who cares to look. About the timing, yes. About the magnitude, yes. About the structural nature of the move rather than a cyclical one, yes on every count that the data supports.

About the consumer category response, partially. The well-funded brands will be fine, in the way that well-funded brands tend to be fine in a compression cycle, and the brands operating with some semblance of fiscal responsibility will pivot to higher-margin formats and survive in a smaller, more profitable, less narratively exciting form than the decks of 2021 promised. There will be a number of survivors. There will be very few acquisitions, and the acquisitions that occur will not be flattering on the terms the press releases will describe. The remainder of the category, which is to say the brands that have been operating on aesthetic alone in the absence of pricing power, distribution moat, cost advantage, or editorial discipline, will return capital gracefully or they will not.

The conversation in the Carolinas did not end with a resolution, in the way that the most useful conversations tend not to. Someone refilled a glass, someone made a joke about the price of a Patriot interceptor, and the room broke up into the smaller conversations that follow the formal agenda. I drove back to the hotel thinking about aluminum, about the country, about the five to seven year window the room had been modeling, and about how few of the brands at the table when I started this work will be at the table when the procurement cycle clears.

A strategic input is going to war again, in the way that strategic inputs have done before, and the brands that prepare for it now will exist in 2030 in a recognizable form. The brands that wait for the chart to confirm the trend will discover, as every operator who has ever sold a hard good through a hot input eventually discovers, that the chart is not weather, the chart is geology, and the time to plan against geology is before the geology reaches the shelf.

韦伯-史密斯的研究与写作

Reporting reflects aluminum spot pricing and forecasts as of the most recent close on the London Metal Exchange via Trading Economics; Pentagon Munitions Acceleration Council disclosures and FY2026 appropriations; PitchBook, CB Insights, and Crunchbase defense-technology venture data for 2025; SIPRI global defense expenditure data; CSIS analysis on munitions surge production; and historical accounts from the U.S. wartime aluminum buildup of 1939 through 1945, including the Defense Plant Corporation program and the antitrust resolution of the Alcoa monopoly.