如果你是在冰箱经常空空如也的环境中长大的,那么亚马逊 Prime 就是你的天赐之物。成年后:一觉醒来,看着冰箱,你的记忆会让你做出不理智的反应,然后你就会毫无必要地打开一个应用程序来填补储藏室或冷藏室的空位。不到两个小时,问题就解决了,你的货架也不再引发食物不安全的想法。亚马逊得到了生意、配送费和数据。好市多就该死了。我不可能是唯一一个经常这么做的人。

这种消费行为的市场会越来越大。通常年费为 139 美元的亚马逊 Prime 为有需要的人提供了一个更便宜的选择,你会听到更多关于它的消息。Prime Access 虽然从 2017 年就开始提供,但最近由亚马逊力推(亚马逊于 2022 年 10 月对这一计划进行了扩展)。可能是作为一个双管齐下的解决方案:

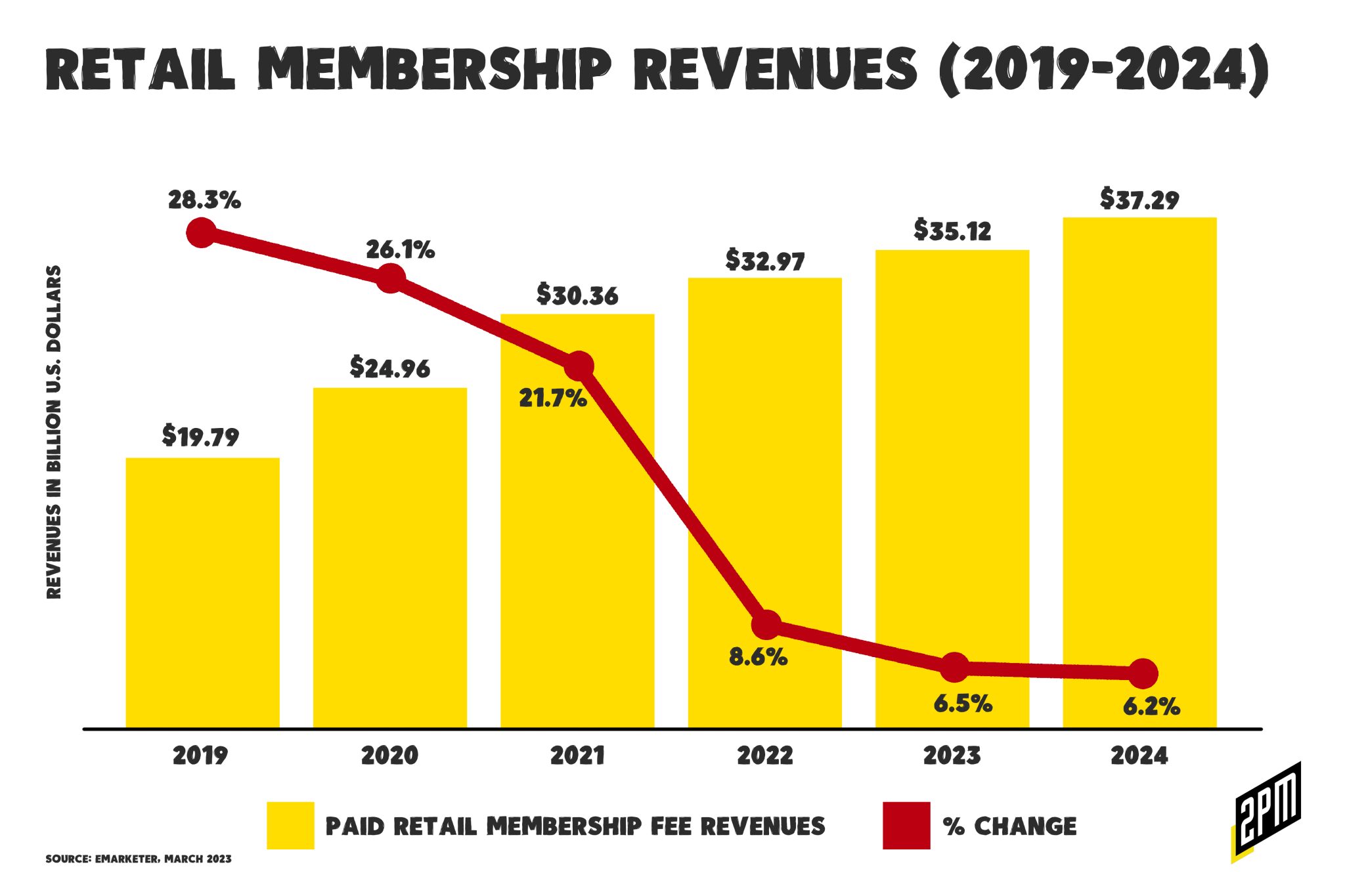

- 其余通货膨胀影响(4.9)

- 零售会员收入下降

不久之后,该应用程序可能会反映出更经济的食品杂货选择。稍后再详述。

从最初的数字书店到现在的多产业巨头,亚马逊一直走在电子商务发展的最前沿。2023 年 4 月,亚马逊宣布推出 Prime Access(一项已有六年历史的计划),旨在让低收入用户享受到亚马逊 Prime 的民主化服务,这再次证明该公司需要适应零售业的发展。

Prime Access 是亚马逊为符合条件的政府项目提供的折扣会员计划。在美国,符合条件的用户注册后可享受亚马逊 Prime 的所有特权,而价格仅为普通会员的 50%。

在整个行业会员收入增长下降的背景下,Prime Access 可能会极大地影响亚马逊的潜在增长。会员制初创公司Inveterate为以下公司的会员忠诚度计划提供支持:Liquid IV、Fresh Clean Tees、Lashify、Fly by Jing、Flamingo Estate 等:

德勤(Deloitte)的一项研究发现,如果付费忠诚度计划能提供显著的益处,67% 的消费者会加入该计划(相比之下,只有 33% 的消费者对免费积分计划持相同看法)。

亚马逊希望通过吸引更多可能对付费忠诚度计划感兴趣的受众,抓住甚至提高剩余的增长。根据Activate公司2022年10月的一项调查,亚马逊Prime仍然是评价最高的忠诚度计划。这其中包括CostCo、山姆会员店(Sam's Club)、沃尔玛(Walmart+)和Instacart+。但可以预见的是,增长速度已经放缓。

传统上,亚马逊 Prime 被视为奢侈品,主要面向高收入家庭。然而,这项新举措代表着亚马逊目标市场的显著扩大。通过利用一系列政府项目,亚马逊正在让更广泛的人群享受到其优质服务,从而扩大其潜在用户基础和收入来源。此举显示了以会员制为驱动、基于应用程序的电子商务的威力:通过降低准入门槛,亚马逊可以开发服务较少(但不断增长)的市场,从而提高其增长潜力。这可能是一剂解药。

在商务活动中,尤其是在亚马逊 Prime 等基于应用程序的市场中进行一键式重复购买时,简单的力量无论怎样强调都不为过(以下是最近对这一主题的深入探讨)。亚马逊模式通过提供无缝、无摩擦的购物体验而出类拔萃。消费者完成购买的步骤越少,转化的可能性就越大。通过尽可能简化购买流程,亚马逊鼓励用户重复购买,从而培养了客户忠诚度并推动了销售。在商业民主化的背景下,我认为有必要引起关注。

本着简化的原则,Prime Access 还致力于实现电子商务的民主化。根据亚马逊的规定,您可以提供以下计划的资格证明或参与证明:

- SNAP EBT

- 医疗补助

- 妇女、婴儿和儿童计划(WIC)

- 补充保障收入(SSI)

- Direct Express 借记卡(DE)

- 贫困家庭临时援助(TANF)

- 全国学校午餐计划(NSLP)

- 低收入家庭能源援助计划(LIHEAP)

- 部落援助资格信(TTANF)

- 营养援助计划(NAP)

传统上,网上购物主要面向那些可支配收入较高并能使用信用卡的人群。通过参加各种政府援助计划,亚马逊可以享受 Prime 优惠,从而扩大了在线零售市场的范围。这一举措为最近才成为企业零售商关注焦点的人群提供了同样的便利和优势,从而实现了商业市场的民主化:

可以说,这是新的直接面向消费者的零售方式。从原产地工厂直接发货可以保持低廉的价格。中国超快时尚巨头 Shein 已风靡全球,并在不断壮大,其 SKU 数量和销售量令 Zara、H&M 和 Boohoo 等竞争对手相形见绌。这些服装价格低廉,一次性使用,令人上瘾。Temu 可以满足人们对 "物美价廉 "产品的类似需求,尤其是在美国通胀率持续攀升,消费价格不断上涨的情况下。

像Shein和Temu这样的中资跨境电子商务公司都非常关注这部分人群,但很少有公司能像亚马逊一样接触到他们。亚马逊的优势在于购买方便、产品齐全、价格透明,而且离消费者很近。与此话题相关的是,有传言称亚马逊可能会收购 Albertsons 和 Kroger 计划剥离的 500 家门店。这些门店将使亚马逊能够发展其亚马逊生鲜(Amazon Fresh)业务,这是比全食超市更经济的商品来源。简而言之,全食超市的规模有限。

在 4 月初致股东的一封信中,亚马逊首席执行官安迪-贾西(Andy Jassy)表示,一直难以起步的杂货业务需要成为公司战略的重点。早在 2017 年,亚马逊就斥资 137 亿美元收购了全食连锁店,但这也伴随着磕磕碰碰。亚马逊还被迫关闭了 Amazon Go 和 Amazon Fresh 分店,并裁员数千人。今年 2 月,亚马逊宣布暂停推出 Amazon Fresh 门店,同时重新评估这一概念的经济效益。

对这一计划的认识以及随之而来的进一步民主化并非没有潜在的弊端。其中一个令人担忧的问题是,在经济极度不稳定的时期,亚马逊允许消费者使用信用卡冲动购买日用品和家庭必需品等必需品。由于一键购买的便利性和琳琅满目的商品的诱惑,消费者可能会发现自己的消费超出了自己的能力范围,这可能会导致债务水平上升。

虽然这是一个潜在的风险,但重要的是要注意,网上购物的便利性,尤其是在购买必需品方面,也可以作为一种财务规划工具。例如,比较价格和产品的能力可以帮助购物者做出更明智的决定,从长远来看有可能省钱。此外,送货上门的便利性可以节省交通费用,尤其是对于那些生活在食品荒漠或交通不便的地区的人来说。

亚马逊对 "Prime Access "的宣传强调了以会员制为驱动、基于应用程序的杂货和家居用品电子商务的变革力量。通过宣传其 Prime 服务的民主化,亚马逊不仅扩大了其增长潜力,还为更具包容性的商业铺平了道路。同时,这一发展也凸显了消费者教育的必要性,以减少债务增加的可能性。随着电子商务市场的不断发展,在提高便利性和可及性的同时,还必须采取措施促进负责任的消费,这一点至关重要。

作者:Web Smith | 编辑:Hilary Milnes,美术:Alex Remy 和 Christina Williams