Some industries are more fragile than others – even if that’s not felt by the average consumer. Of the most fragile is eCommerce, something that people use everyday without thinking, but which depends on a weakened state of trade made all the more complex by a number of concurrent global conflicts. Of them, there are now two that have captured the American imagination, concern, and even involvement: the Russo-Ukrainian War and Israel’s growing conflict with Palestinian terrorist groups, a geo-political complexity that requires an understanding of the region’s history, religious factions, and divisive politics to begin to understand.

We are more aware of persisting war than ever before. We are also more aware of the interdependency between the nations that fight them. The idea that the two are dependent on one another is not new, however. The following is extracted from Commercial Traveller, written in December 1842 under the banner “War and Commerce”:

We are not writing as politicians, for, although we are not without a political creed, in our commercial capacity we are of no political party. We look upon war as the deadliest enemy of commerce, and of human industry in all its forms, and we believe that commerce and the arts are so far necessary to national prosperity, that no people can be great, prosperous, and happy without them.

Around 80 years later, Alvin Saunders Johnson wrote the following in the Political Science Quarterly (1914): “International trade, we are often told, is one of the most powerful of the influences making for universal peace.” The section was entitled, “Commerce and War.”

In an era of unparalleled global connectivity, the boundaries between geopolitics and commerce have become increasingly porous. This intertwining of worlds is most evident when a singular event, like the eruption of a geopolitical conflict, sends ripples through commercial hubs thousands of miles away. Here’s but one of many examples:

The Chinese e-commerce website Shein has stirred new controversy by calling off its campaigns with Israeli Instagram influencers after it was criticized for selling Palestinian flags — and not Israeli ones — following Hamas’ terror onslaught against Israel earlier this month.

As the recent Russo-Ukrainian War has shown, the resilience of the global eCommerce ecosystem is both a testament to its adaptability and a reflection of its vulnerabilities. For one, it’s highly dependent on a healthy middle class. This March 2022 quote by Christopher Smart of the Barings Investment Institute still stands:

There was an emerging middle class [in Russia] that is now going to be knocked back. It’s going to be isolated. It’s going to have a currency that doesn’t really hold any value outside the country.

In this delicate balance between progress and conflict, warring nations emerge as crucibles, illustrating the intricate dance of commerce in the shadow of geopolitics. Below is five ways that the conflict between Russia and Ukraine directly impacted global commerce.

Supply Chain Challenges:The ongoing war coupled with associated economic sanctions strained the global supply chain, which is still recovering from the pandemic’s effects. Many American brands might believe they are insulated from European disruptions, but many US manufacturers rely on components from Europe. Notably, over 300,000 US companies are intertwined with supply chains in Russia or Ukraine, according to Practical eCommerce. Considering Russia’s significant exports, ranging from fuel and wheat to precious metals, businesses in countries like China, Germany, and Italy may face prolonged procurement times.

Rising Shipping Costs: As the conflict intensified supply chain pressures, global gasoline prices soared. Gasoline prices in The Netherlands and the US have surged since 2022, leading to higher transportation costs. Major carriers, from UPS and FedEx to international shipping giants like Maersk, alerted businesses about potential fuel and “war risk” surcharges.

Dampened Consumer Spending: The war’s ripple effects on global economies curtailed consumer spending and confidence. A typical American consumer, grappling with increased gas prices, dwindling investments, and escalating food costs, is likely to limit discretionary purchases.

Increased Borrowing Costs: The Russo-Ukrainian War accelerated global inflation. With the US Federal Reserve hiking interest rates in response to rising prices, borrowing became costlier for both businesses and individuals.

Potential for Product Hoarding: Memories of pandemic-triggered shortages linger. The Ukrainian crisis spurred some consumers into panic buying. Online retailers were advised to assess whether their products were prone to such buying frenzies (which could potentially lead to stock issues).

Israel, Ukraine, and Russia are each critical to global trade. But when worlds of commerce, cultural derision, and military conflict collide, the ripple effects are unpredictable. The response to conflict is mostly predictable, though: when will it end?

Infrastructure and “Soft Power Diplomacy”

Online retail, which grew considerably during the pandemic, wasn’t spared when Russia invaded in Ukraine in 2022. From supply chain disruptions to increasing borrowing costs, businesses, no matter where located, were facing the realities of a war occurring continents away.

The Israel-Palestine conflict could have a more direct impact on the US. As of writing this, the U.S. has deployed several vessels from the U.S Navy’s fleet and ordered 2,000 military personnel to be ready for deployment.

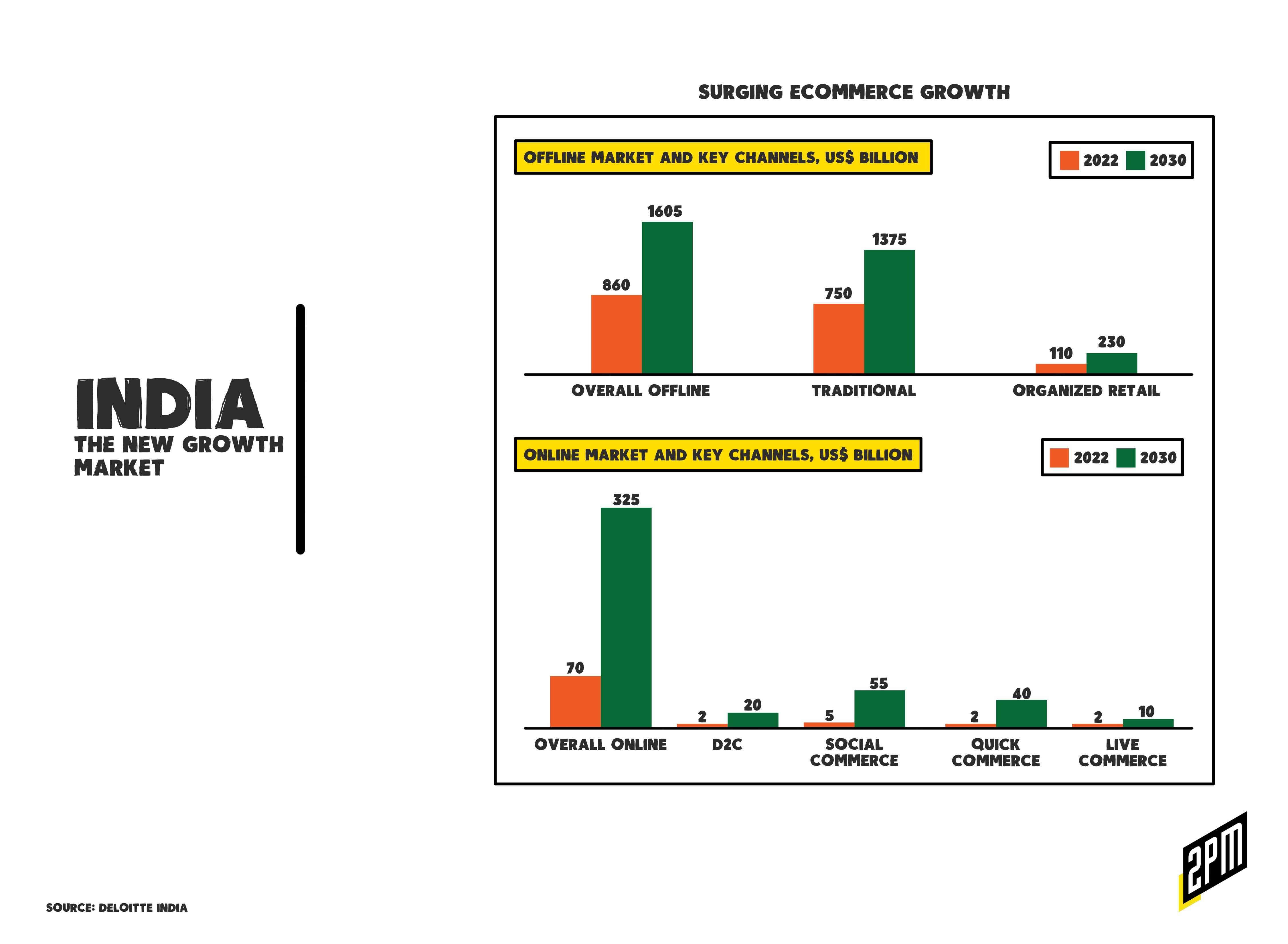

With around the size and population as the state of New Jersey, Israel, is a small-yet-powerful nation with an outsized impact. To put this in context, India is projected to reach $165 billion in eCommerce revenue by 2025 with 1.41 billion residents. Israel, with its 9 million residents, is expected to reach $12 billion in eCommerce retail value by 2025. Israel will generate 7% of India’s projected 2025 eCommerce totals with .64% of India’s population. And to be fair, online retail is not its leading industry.

The country boasts the United States and China as its top two import partners according to data collected by the CIA. As the global pandemic’s restrictions eased, Israel exhibited a surge in private consumption, revealing a robust retail framework. According to the International Trade Organization, Israel has an 87% internet penetration and a 47% eCommerce penetration, representing 4 million of the 9 million in Israel. This number is expected to grow to 5 million users by 2025.

With giants like Shufersal leading the local scene, and international heavyweights such as IKEA and Apple marking their presence in country, the market seemed poised for accelerated growth. Israel also boasts industry stalwarts like Yotpo, Mixtiles, Freightos, and Jifiti. Still, Israel’s eCommerce sector lags behind global averages, suggesting vast untapped potential. Yet, as Israel contemplated leveraging this potential and as local retailers like Rami Levy and Shufersal pivoted towards online sales, the global landscape darkens with clouds of new wars.

For the Russo-Ukrainian War, the tangible impact of the war on commerce was evident in supply chain disruptions. Despite being an ocean away, businesses worldwide, including those in the United States, felt the shockwaves. Many, unbeknownst to them, relied on materials sourced from either Russia or Ukraine. Russia’s significant exports like fuel, oil, and metals form a crucial part of global manufacturing, and disruptions here inevitably rippled outwards. The resultant long lead times were an immediate concern for eCommerce platforms, many of whom thrived on efficiency.

This, combined with the spike in transportation costs, isn’t just a transient concern; it changes the fundamental economics of eCommerce, pushing businesses to reassess their strategies. Here’s an example from an August 2023 feature in WWD on Ukrainian eCommerce:

In what organizers described as “soft power diplomacy,” Ukrainian makers of all disciplines are carrying on with their businesses to the best of their abilities, despite the ongoing invasion by Russia.

The cost of Ukraine‘s recovery and rebuilding was estimated to be $411 billion in March, based on a Word Bank report. Millions have left Ukraine since the fighting began in February 2022, including many craftspeople and workers who had provided services for the Ukrainian designers and makers. Impressively, 80 percent of the team behind the project is based in Ukraine, and all of the vendors and brands are also there. Given that, whenever there is a heavy attack, plans change, deadlines move and whatever work is underway is reconsidered.

From a macroeconomic perspective, the Ukrainian-Russian War catalyzed global inflation. Central banks worldwide, like the US Federal Reserve, responded with interest rate hikes, inevitably affecting borrowing costs for both companies and consumers. For burgeoning eCommerce platforms, especially in evolving markets like Israel, this could mean reduced credit availability, directly influencing expansion plans and operations.

Despite the challenges, history has shown that commerce is resilient. During the pandemic, businesses globally adapted, innovating to cater to a homebound consumer base. Similarly, in the face of geopolitical tensions, eCommerce platforms can leverage strategies like stockpiling specific high-demand products or diversifying supply chains to minimize dependencies on conflict zones. But as these two wars continue to intensify, exposure will only grow.

The intricate dance between war and commerce is a testament to the interconnectedness of our global economy. As Israel and other nations navigate their conflicts, those conflicts become all of ours (though their costs are infinitely higher). The ability to adapt and evolve will define the future of global eCommerce. The balance between technological progress, market dynamics, and geopolitical tensions will continue to shape our world, underscoring the importance of preparedness, agility, and innovation in the face of adversity. International trade is one of the most powerful of the influences making for universal peace.

It appears as though international trade is not enough of an incentive. We’ve proven this again and again, spiting ourselves in the process.

By Web Smith | Editor: Hilary Milnes with art by Christina Williams and Alex Remy