The all-day athleisure era is giving way to something more disciplined. Over the last 18 months or so, the everyday uniform has shifted from leggings and hoodies to polished work-leisure: stretchier chinos, knit blazers, temperature-regulating shirts, and trousers with a drape. That shift didn’t kill comfort; it put guardrails around it. Comfort now has to “pass” in more rooms—client coffees, school events, airport lounges, all without reading like a gym kit. At the same time, the culture has rediscovered real sport, especially tennis and running, as a stage for style and credibility.

As those two currents converge, athleisure has narrowed. It’s no longer the default “worn by all.” It’s increasingly worn most by people whose lives actually orbit sport: those who play, coach, race, or at least anchor their social life around studios, courts, clubs, or run crews.

Even a pawn can beat a king.

That’s visible in product (court/pickleball capsules, performance trousers replacing leggings as daywear), in distribution (destination retail near clubs and studios), and in marketing spend (athlete deals and federation partnerships instead of purely influencer grids). Adidas’ partnership with Texas Tech Women’s Soccer player Sam Courtwright appeared this week on the homepage, in what I gather is a leading indicator for what’s to come. The redshirt sophomore is a high value athlete, providing credibility to Adidas in the collegiate scene. With under 700 Twitter followers and ~4.200 Instagram followers (at the time of publishing), she’s not a bonafide “influencer” in the sense that her posts will drive instant business. Adidas is not playing checkers like the minions, they’re thinking further ahead. Even a pawn can beat a king.

Sportswear is returning home. And it needs athletes to provide the credibility and authority that once rested on the pliable shoulders of fitness influencers and barely-clothed yogis.

Lululemon, Vuori, and Alo: once shorthand for anytime/anywhere athleisure are also investing where the cultural heat is: real sport plus a club-coded lifestyle that reads appropriate off-court. Lululemon’s Team Canada outfitting and the brand’s women’s ultramarathon project (FURTHER) are emblematic of that pivot from “studio vibes” to “performance receipts.” Vuori’s jump onto the pro-tennis stage is another. Alo’s tennis/pickleball push and athlete seeding is the same play in LA tones. Just this week, it was announced that Adidas’ part

The net effect: the mass, anything-goes uniform is giving way to a split market. On one side, polished business-casual made with performance materials (the Mizzen+Main, Ministry of Supply, State & Liberty, Fair Harbor universe) satisfies daily wear. On the other, “sport-first lifestyle” led by tennis/run/golf claims permission to travel beyond the venue. The middle—undifferentiated leggings-and-hoodie looks for non-athletic pursuits, is what’s shrinking.

Who the top brands are signing (recent headline deals):

Below are notable, verifiable athlete partnerships and ambassador signings from 2023–2025 that illustrate the shift toward authentic sport. This is a curated snapshot of marquee names (not an exhaustive list of every ambassador).

Lululemon

- Sir Lewis Hamilton: (need I say more?)

- Frances Tiafoe (ATP): joined as a global tennis ambassador in January 2025

- Leylah Fernandez (WTA): active campaign face for tennis collections in 2025

- Team Canada (Olympic/Paralympic): official outfitter through the Los Angeles 2028 Games

- Programmatic sport push: women’s six-day ultramarathon “FURTHER,” tied to a women-specific running capsule

Vuori

- Jack Draper (ATP No. 5): multi-year apparel deal announced ahead of the 2025 US Open.

- Jared Goff (NFL): named ambassador in September 2025 as Vuori expands athlete partnerships

- Arch Manning (NCAA/NIL) and Colston Loveland (NFL): part of Vuori’s growing athlete slate

- Rob Machado (surf): long-running ambassador/collaborator anchoring the brand’s coastal performance DNA

- Olivia “Livvy” Dunne (NCAA gymnastics): collaborator and NIL face

Alo

- Parris Todd (pro pickleball): official sponsorship; featured in Alo’s tennis coverage and athlete content

- Julian “Juju” Lewis. He signed an NIL deal with Alo Yoga in February 2024 and later enrolled at Colorado; recent coverage of his new equity deal notes the prior Alo partnership

- Caleb Williams (USC, then NFL) — NIL partnership with Alo Yoga

- J.J. McCarthy (Michigan, now NFL) — cited as an Alo partner

Athleta

- Simone Biles (gymnastics): long-term partnership; continued 2025 visibility (ESPYs red-carpet collaboration)

- Lexie Hull (WNBA) and Kate Martin (WNBA): signed as brand ambassadors in 2025; Athleta also maintains a broad women’s roster across sports

Sweaty Betty

-

Denise Lewis (Olympic heptathlon): 2025 ambassador announcement.

Why this list matters: it maps the center of gravity for the category. The biggest storytelling budgets are flowing to real athletes and federation-level platforms, not just studio instructors or generic influencer seeding. For brands born in the athleisure boom, these deals buy credibility on court/track—then justify the off-duty product that customers want to wear to dinner.

The Analysis:

From “Gym-Anywhere” to “Polished Off-Duty.” Or why athleisure is ceding ground to casualwear and how Lululemon and others are leaning into sport and Sporty & Rich-adjacent aesthetics to win what’s next

After a decade of “wear-it-everywhere,” the cultural permission for overtly gym-coded outfits outside the studio, court, or track is narrowing. Consumers still want comfort, but the uniform is evolving toward polished casual (denim, trousers, cardigans) and club-coded sport (tennis/golf silhouettes that “pass” in more social settings).

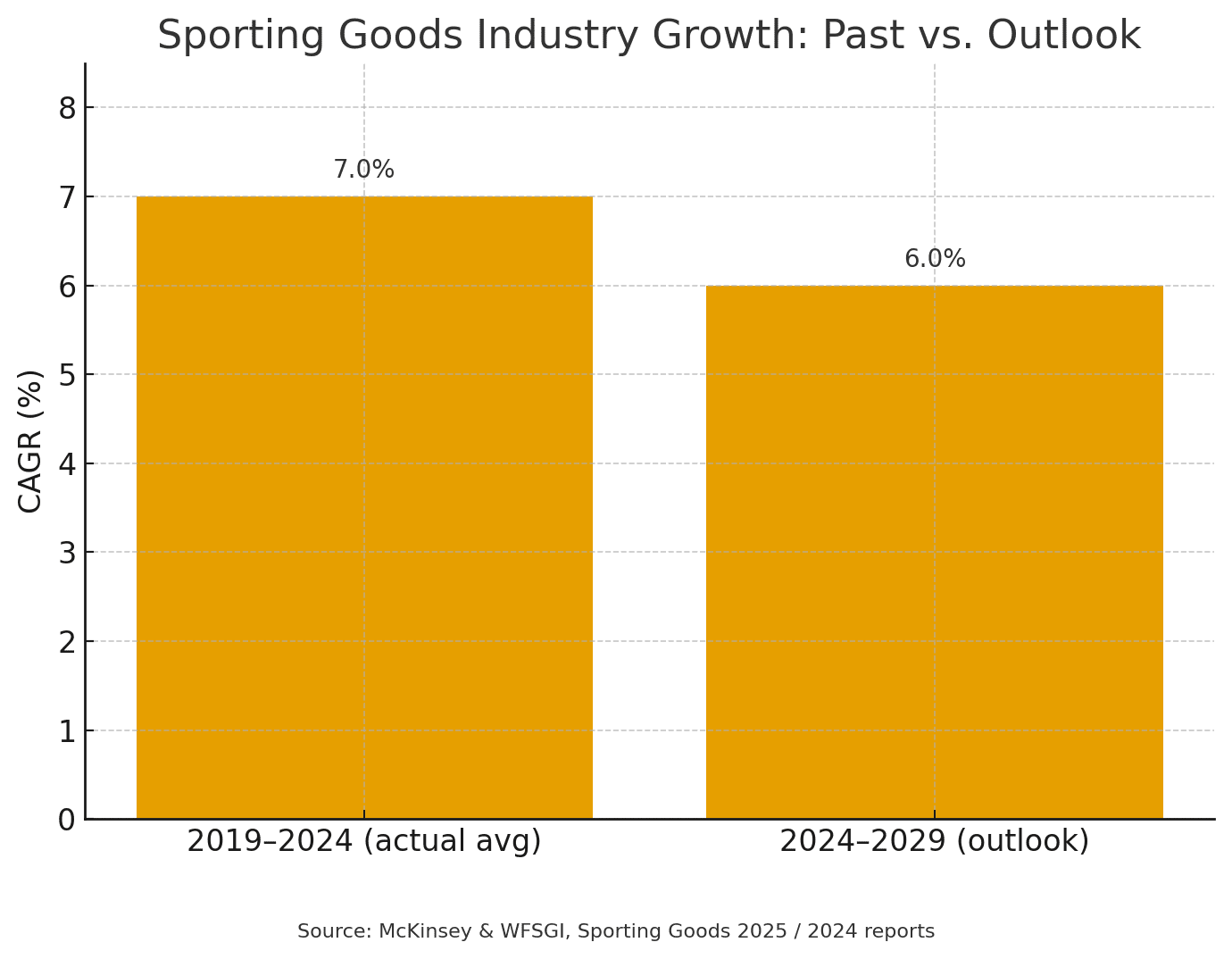

At the same time, performance sport is culturally hot again (tennis, running), nudging leaders to prove they’re serious about sport while selling a cleaned-up lifestyle aesthetic. Lululemon, Alo, and Vuori are each threading this needl: sport for credibility, Sporty-&-Rich-adjacent for lifestyle. as growth in the broader sporting-goods market softens from ~7% (2021–24) to ~6% (2024–29).

The demand shift: from “anywhere athleisure” to “polished comfort”

- Macro growth is normalizing. McKinsey/WFSGI’s 2025 outlook pegs industry CAGR at ~6% from 2024–29, down from ~7% during 2021–24. The market isn’t collapsing, but it is moving from break-neck growth to a productivity game.

- Comfort remains non-negotiable—just styled differently. As early as 2023, Circana tracked a steady pivot toward “polished comfort,” with dress pants, woven shirts, jackets/blazers and other “passable” items outperforming as shoppers seek versatility that reads appropriate across more venues.

- Active bottoms are soft. Between April 2024 and April 2025, US active bottoms sales fell ~12%, per Circana cited by Business of Fashion, even as overall sportswear remains resilient. That helps explain the lens shift away from leggings-as-daywear toward trousers, wide-leg track pants, and tailored knits.

- Category leadership is still attractive, but more contested. BoF and McKinsey State of Fashion 2025 notes sportswear continues to grow faster than the broader fashion market, but by slimmer margins and amid greater variance by region and company. Translation: out-execution matters more than tailwinds.

Why it matters: The “anywhere” athleisure look that felt novel in 2016 America can read underdressed at dinner, derivative on vacation, and flat at the office. The culture hasn’t abandoned comfort. However, it’s editing the costume toward refined, venue-appropriate pieces or sport-coded uniforms that carry social credibility.

Culture & sport: tennis goes mainstream, running gets mythic:

Tennis has become a fashion stage again (US Open capsules, pleated skirts, club sweats), and brands are investing accordingly. Meanwhile, running reclaimed mindshare as a proving ground for material innovation and women-specific design—spotlighted by Lululemon’s FURTHER ultra initiative and women-specific run capsule.

Lifestyle proof points:

- Lululemon’s Varsity/tennis assortment (e.g., the Varsity High-Rise Pleated Tennis Skirt) squarely channels that Sporty-&-Rich-ish country-club aesthetic.

- Alo pushes “Tennis Club” knits and dresses as street-passable athleisure.

- Vuori’s Court to Resort blends tennis/golf silhouettes built to move, explicitly framed to travel beyond the court.

Category economics at a glance:

- 2019–2024 actual/avg: ~7%

- 2024–2029 outlook: ~6%

Implication: With softer topline, the winners must harvest efficiency while re-segmenting product: more polished casual for lifestyle, more real sport for credibility.

Brand narratives: how the leaders are repositioning:

Lululemon: leaning Varsity while doubling down on sport

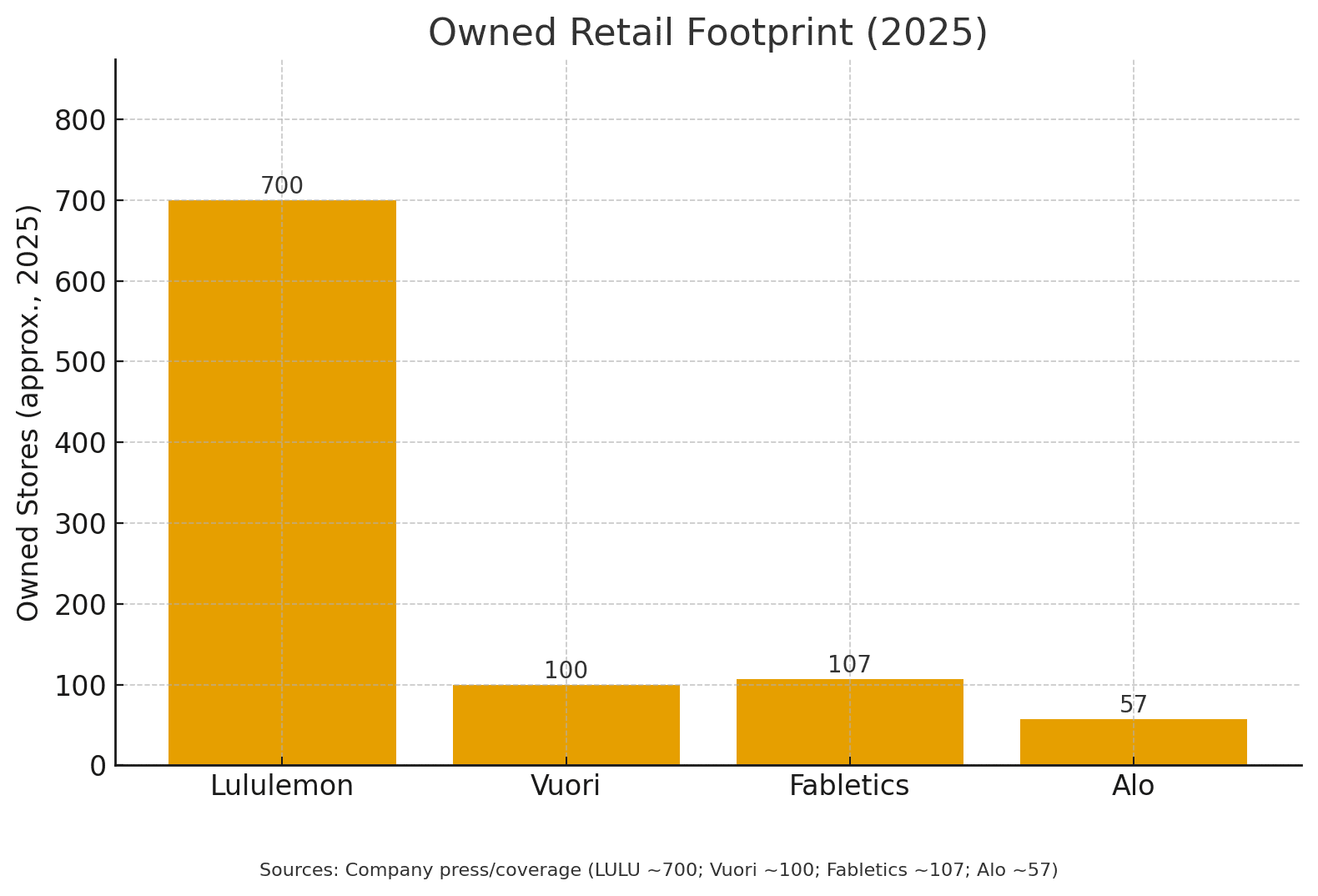

- Where it wins: Scale (~700 stores in 2025), brand equity with both genders, and a powerful accessories/basics engine.

- Where it’s vulnerable: North America momentum cooled into late 2024 as upstarts clawed share and style leadership; Reuters flagged the slowest quarterly growth in 4+ years amid stronger competition from Alo and Vuori.

The pivot in plain sight:

- Aesthetic: A more polished, preppy varsity palette—pleated skirts, polos, cable knits—clearly sits in the Sporty & Rich slipstream. Lululemon’s “Varsity” and tennis pages show the merchandising logic.

- Sport credibility: Lululemon attached itself to Team Canada (outfitter through the 2028 Games), and staged FURTHER, a six-day women’s ultra that anchored a women-specific running capsule (“Go Further”): a smart, ownable sport narrative that travels beyond the event. Not to mention, Lewis Hamilton, everyone.

Read: Lululemon is re-earning permission for lifestyle by proving it on-course/track—then selling the cleaned-up off-duty uniform.

Alo: luxury-wellness halo meets tennis-adjacent lifestyle

- Distribution & scale: ~57 stores as of April 2025 with plans to add 50+ through 2025; European rollout (London, Paris) is live; DTC is the engine (Vogue Business cites ~98% DTC mix).

- Aesthetic: “Tennis Club” knits/dresses and polished separates are built to pass at brunch or travel, not just the studio.

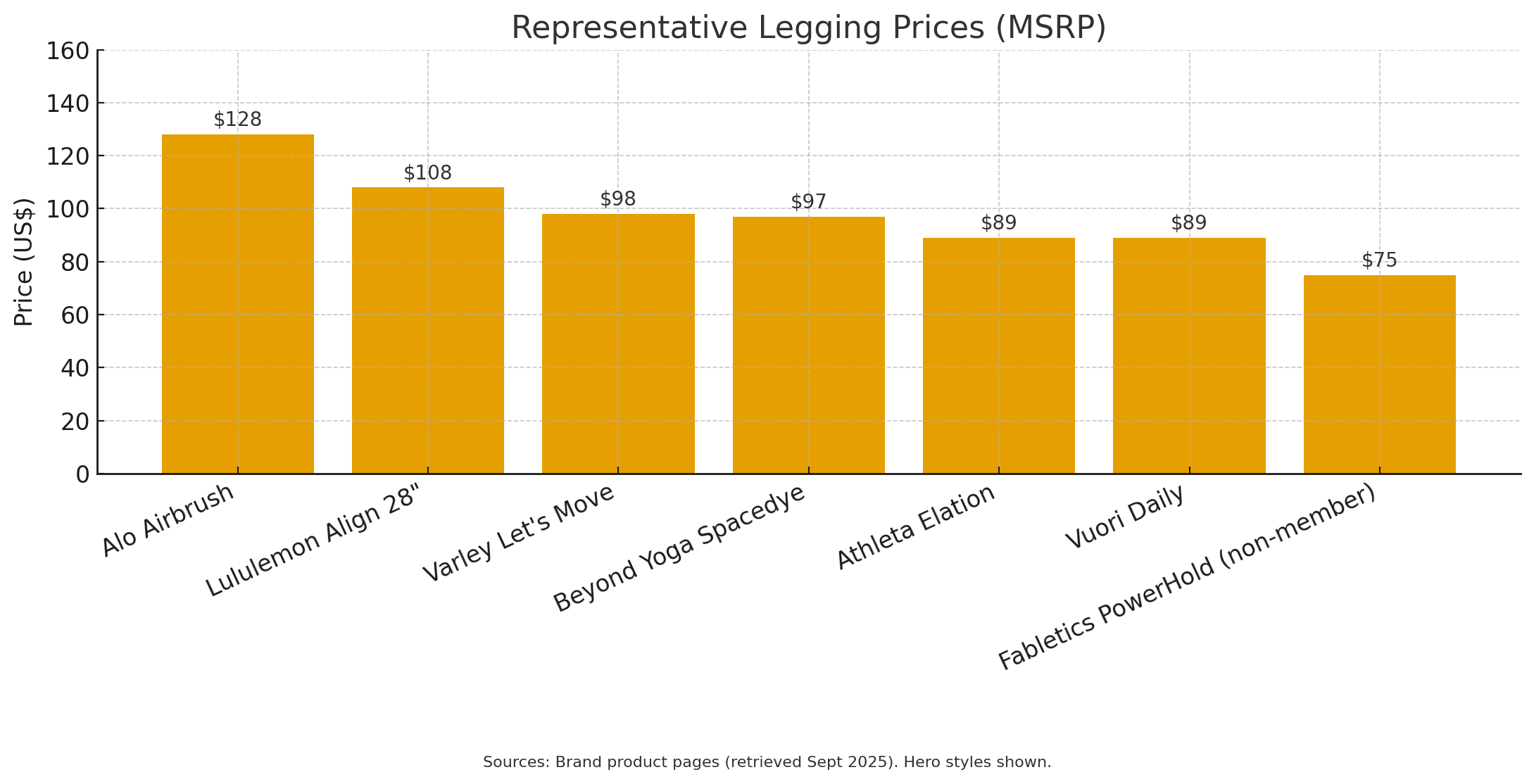

- Price/positioning: Premium AURs (e.g., Airbrush leggings at ~$128) cement a “luxury-wellness” adjacency—price power requires distinctiveness.

Read: Alo scales through high-touch retail, creator marketing, and a wardrobe that implies sport yet reads refined in daily life.

Vuori: “Court to Resort” + real on-court receipts

- Stores & expansion: Surpassed 100 owned locations globally (Aug 2025); accelerating international growth (UK, China, Korea).

- Aesthetic: Clean SoCal minimalism, with Court to Resort as the bridge between performance and travel/lifestyle.

- Sport credibility: A multi-year deal with Jack Draper (current world No. 5) gives Vuori hard on-court validation to push deeper into tennis product.

Read: Vuori pairs an easy lifestyle look with visible elite-sport proof, strengthening its “wear-it-everywhere” claim without the athleisure stigma.

The store race (because stores tell the strategy):

- Lululemon ~700

- Vuori 100

- Fabletics 107

-

Alo 57

What the footprints signal:

- Lululemon will keep adding doors but must refresh aesthetics faster.

- Vuori is turning into a serious global retailer; tennis/golf doors make sense in travel/luxury corridors.

- Alo is building a flagship-heavy network that sells the clubhouse lifestyle as much as product.

- Fabletics is quietly becoming the value-plus omni player with >100 stores and membership economics.

Price ladders are hardening (and visible to the consumer):

Take: With active bottoms softening, premium brands need new reasons to pay up (fabric handfeel, fit innovations, and—crucially—styling that “passes” at the restaurant).

East Hampton × Erewhon: the five brands setting the uniform:

Alo: LA pilates energy with clubroom polish. Think tennis dresses, pleated skorts, cropped collared knits and sculpted leggings that pass from Reformer to lunch. It’s the default Erewhon look and shows up in Hamptons school-drop-off lines just as easily.

Varley: LA/London court-core made elegant. Soft neutrals, half-zip knits, tailored track pants, tennis skirts—the precise “polished comfort” moms wear from the club to Main Street. If you see a cable-stitch over a pleated skort in East Hampton, odds are it’s Varley.

Sporty & Rich: Off-court preppy as a worldview. Tennis club sweats, logo caps, retro polos and cream palettes that scream “country-club casual.” This is the reference aesthetic Lululemon and others are orbiting; the East Coast reads it as heritage without the fuss.

Why these five: they each deliver the new dress code, court-inspired, studio-capable, socially acceptable—without reading like gym gear. They’re the overlap in two style capitals (Montauk brunch and Beverly Hills produce runs), where comfort is table stakes but polish is the pass.

FP Movement: Fashion-forward active that still feels fun. One-shoulder sets, airy parachute pants, bold color capsules that move from pilates to beach errands. It’s the youthful, Instagram-native counterweight in carts that already have neutrals and knits.

Set Active: LA minimalist matching sets for the grocery-run-to-meetup window. Box-cut tees, compressive bras, monochrome leggings/shorts, all in seasonal tones. It’s the Erewhon aisle staple that also sneaks into Hamptons weekends when the brief is “clean, not try-hard.”

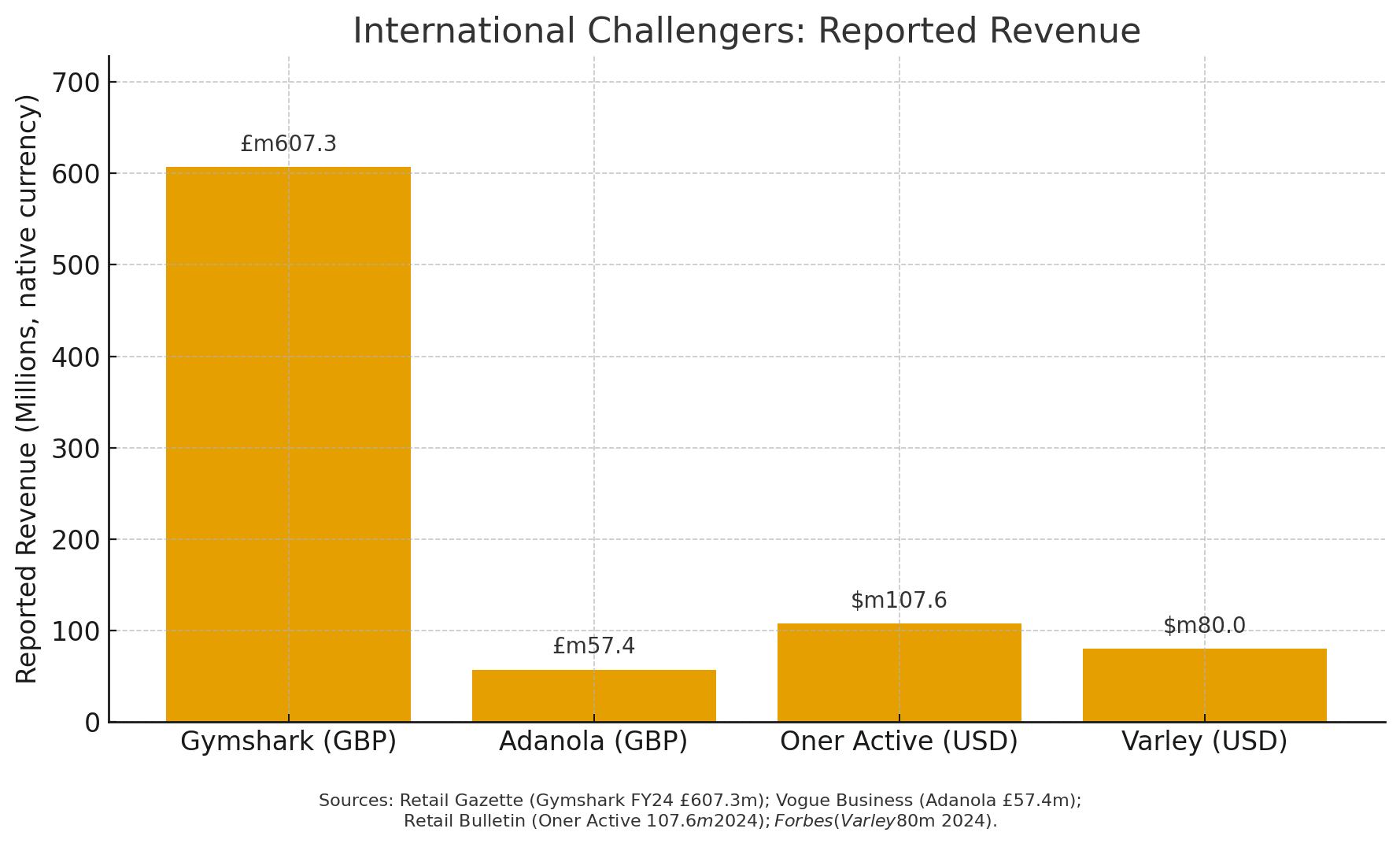

International challengers with real North American upside:

- Gymshark (UK): flagship now on NYC’s Bond Street—credibility + DTC mastery + hybrid retail.

- Adanola (UK): “clean girl” aesthetic aligned with polished athleisure; value-friendly sets with fast refresh.

- Oner Active (UK→LA): creator-led distribution plus relentless newness; strength-first silhouette.

- Varley (UK/US): tennis-adjacent lifestyle—already resonating stateside (Forbes coverage).

- LIVE! Activewear (Brazil): single U.S. beachhead in Miami; yoga-first pilates/run/tennis closet with polished off-duty pieces; building U.S. awareness via events and eCommerce-led scale.

Also watch: Sweaty Betty (UK), back to U.S. stand-alone retail (Chicago & DC); and LSKD (AU), a scrappy, community-led playbook gaining ground in the U.S.

Outdoor Voices: a case study in the narrowing “anywhere” permission:

OV’s 2024 store closures signaled the end of a specific DTC era; the 2025 relaunch under returning founder Ty Haney aims to rebuild community and refine the aesthetic. It’s a reminder that generic “athleisure” storytelling is no longer enough—brands must own a credible sport lane or a distinctive polished lifestyle lane (ideally both).

Sporty-and-Rich-adjacent: the playbook in action:

A critical nuance: mimicry isn’t strategy. Sporty & Rich continues to elevate the off-court tennis narrative via fresh color/material capsules with Adidas—so incumbents must avoid derivative “country-club” clones and instead push their own fit/fabric signatures and authentic sport credentials.

- Lululemon: attaches to national teams and women’s running R&D; merchandises pleats, polos, and varsity sweats without abandoning performance.

- Alo: dresses the clubhouse with cashmere-adjacent knits and tennis-coded skirts; European flagships sell the lifestyle world as much as product.

- Vuori: signs top-5 tennis talent (Jack Draper) to make on-court performance a central claim; then extends looks “from court to resort.”

What the numbers are telling me right now:

-

The growth curve is bending, not breaking. A 6% CAGR outlook is still healthy, but it rewards clearer differentiation and sharper inventory discipline. (See Chart 1.)

-

Lifestyle dollars are migrating to “passable” silhouettes. Circana’s polished-comfort data is consistent with what we see in merchandising across the leaders. Circana

-

Active bottoms need a new story. With –12% category pressure, brands must either re-architect the legging (fit/feel/opacity) or sell alternative bottoms that still read active-adjacent.

-

Retail footprint matters again. Vuori (100+), Fabletics (>100), and Alo (flagships) are proof that physical retail is a brand-experience moat—especially for a more refined, try-on-worthy wardrobe. (See Chart 2.)

Strategic implications (12–18 months):

For incumbents (Lululemon, Nike, Adidas, etc.):

- Double down on credible sport moments that are ownable (e.g., women-specific R&D built on real athlete input). Lululemon’s FURTHER is the blueprint: a cultural event that justifies a product line.

- Merchandise a “passes-anywhere” capsule in every delivery: pleated skirts, trousers with stretch/recovery, collared knits, and travel-ready layers that read elevated.

- Refresh cadence matters. Upstarts are winning TikTok-speed trend windows. The response is faster color/material drops without SKU bloat.

For challengers (Alo, Vuori, FP Movement, Varley, Beyond, YPB)

- Own a sport and an aesthetic. Vuori’s Draper deal gives permission to claim tennis performance; Alo owns the clubhouse. Keep both lanes distinct.

- Price architecture: Protect premium AURs with fabric handfeel and tailored fits; consider value-adjacent capsules to defend share as promo pressure rises.

- Retail where it counts. Flagship corridors + resort markets + club-adjacent neighborhoods monetize the new uniform better than generic high streets.

For wholesale/retail partners

- Buy for outfits, not SKUs. Curate trousers + pleats + court knits as complete looks.

- In-store services (stringing, run gait, pilates clubs) convert “sport credibility” into community and repeat visits—think Omni not just Units Per Transaction.

What could go wrong:

- Aesthetic drift: Over-indexing on “country-club” sameness risks turning premium floors into a sea of cream cable-knits. Keep material innovation and brand signatures front-and-center.

- Cost of legitimacy: Athlete deals and real on-court R&D are expensive. Vuori’s Draper bet raises expectations for performance across the line, not just a capsule.

- It’s refinement, not a return to formality. Workwear casualization persists; the move is toward elevated comfort, not suits. Plan for nuance by market and occasion.

Brand scorecards (executive shorthand):

- Lululemon: Scale incumbent managing NA softness by leaning harder into sport (Team Canada; FURTHER) and a varsity/tennis lifestyle. Execution risk is refresh cadence and not losing edge to faster-moving rivals.

- Alo: Luxury-wellness halo + creator engine; ~57 stores and expanding in EU; DTC-heavy; sells the clubhouse closet at premium AURs.

- Vuori: Now 100+ owned doors; clean SoCal aesthetic; Jack Draper deal to anchor a real tennis push; travel-and-resort hooks broaden usage occasions.

- Athleta: Reset under Gap Inc.—sharpen assortments and rebuild brand heat (short-term comps pressure is the trade-off).

- Fabletics: Membership economics + rapidly expanding retail (>100 stores) = a scaled value-plus foil if premium brands get too same-y.

- FP Movement, Varley: Taste-making references for the “hot-mom” uniform—elevated, functional, and social-feed ready.

- Outdoor Voices: Community nostalgia + founder return; must modernize supply and tighten the SKU plan to stick the comeback.

What to watch (next 6–12 months):

-

US Open → Holiday tennis halo: Expect more tennis capsules (and brand/athlete moves) to ride the court-to-clubhouse wave.

-

Active bottoms reset: Who tells the best non-legging bottoms story (tailored track pants, performance trousers) with true fabric innovation?

-

Store productivity spreads: Vuori and Alo flagships vs. Lulu’s fleet—watch traffic quality, not just door counts.

-

Value-active acceleration: As promo pressure rises, expect Abercrombie YPB, Fabletics and department-store private labels to take more oxygen.