备忘录DTC 品牌和二级市场

It’s not farfetched to argue that brands are capable of attracting consumer attention and commerce in ways that resemble traditional media and entertainment companies. A Vuori yoga studio would be in high demand for daily classes. An LMNT trail run series would attract enthusiasts in a number of cities known for outdoor activity. Both of these venture-backed companies share more than fitness in common; they share tremendous secondary market interest.

If given the option (even in today’s depressed secondaries market), the brand’s most avid supporters advocates, would buy shares of Vuori or LMNT or Gymshark or Liquid Death. The purchase of secondaries is an expression of brand equity, and it may be the best indicator for a brand’s market viability moving forward.

Brands and their equities are not determined solely by their retail sales. A pop entertainer’s value is not determined solely by primary market sales. If you’ve ever tried to buy Taylor Swift tickets from Seatgeek, you’ll know what I mean. Swifties, perhaps the purest expression of brand advocacy in modern entertainment, are willing to pay a premium just to be there for the show.

In the contemporary marketplace, brands have evolved to become much more than mere purveyors of products or services; they are, in many ways, entertainers. This reality is particularly evident in how consumer engagement and brand experience play central roles in shaping customer perceptions and loyalty. Just as a blockbuster show or a high-profile concert captivates an audience, successful brands like Vuori, Shein, Skims, Faherty, Whoop, and LMNT enrapture many of their customers. These brands leave customers wanting more from them, leaving open the idea of creating immersive and emotionally resonant experiences for then.

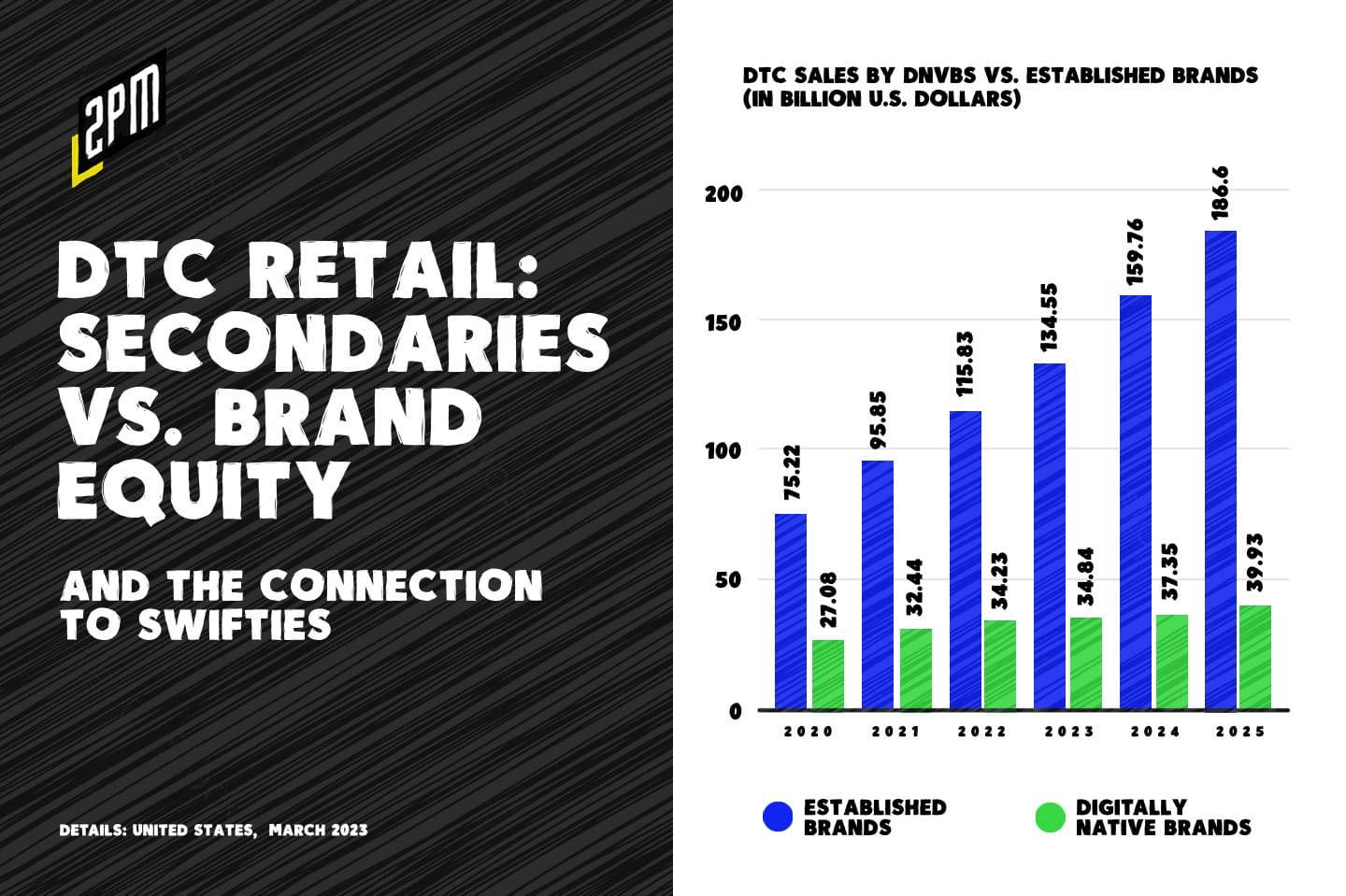

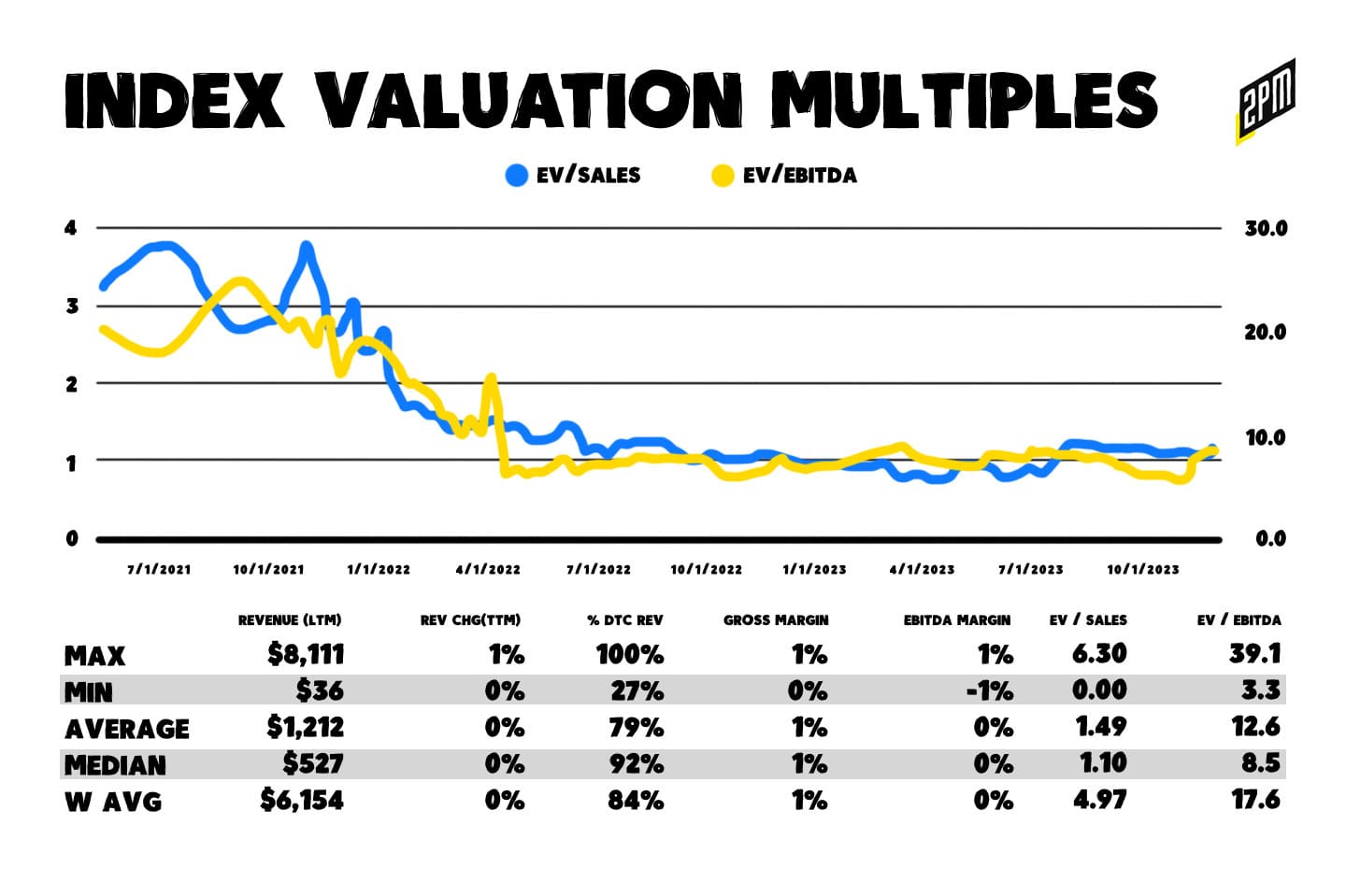

This extends into the realm of financial valuations. For the aforementioned brands, a cross section of extraordinary DTCs, their secondary interest can be likened to after-market ticket prices for major entertainment events. Across the market, valuation multiples in DTC are depressed according to the Drivepoint index that includes: Lululemon., Yeti, Canada Goose, Purple, Hims, Solo Brands, FIGS, Brilliant Earth, Lulu’s, Allbirds, and Laird Superfood Inc. But according to a recent report by Carta, secondary interest in internet-based companies till remains high.

A plurality of startups conducting liquidity programs so far this year on Carta have been in the SaaS sector, which is in line with historical norms. Two other sectors have seen substantial increases in their share of secondary activity: About 23% of deals so far this year involved internet & media companies, up from 18% for the full year 2022. (H1 Report – Carta)

But while this is an indicator of industry health, it is somehwat Carta added: “When the percentage of employees who are sellers declines, the percentage of sellers who are founders and investors increases.” In the context of the ratio of employee offering to founder offering, “Back in H1 2021, nearly seven out of every eight sellers was an employee.” That rate fell to three out of four in H1 2022, and it indicates a reflection of market appeal and the level of excitement a brand generates among investors, akin to a must-see show that draws crowds willing to pay premium second-market prices for the experience.

A barometer for brand equity: what’s the brand’s secondary market like? If the answer is non-existent, it could be a cause for concern. A brand advocate should always want behind-the-scenes access to the top brands.

Just as a sold-out concert or a hit Broadway show signifies high demand and popularity, robust and rising secondary interest in the private market signal a brand’s strong position and the high regard in which it is held by investors. These prices are not just numbers; they represent the collective anticipation and enthusiasm of the brand’s future in the market, mirroring how audience demand drives up ticket prices for a hit entertainment event. While not representative of a secondary market, we commonly see this stock vs. product purchase discussion in the context of Tesla. A Reddit thread on the psychology of this situation is fascinating:

Based on my current behavior, I would rather invest in the company…really want one of the cars though, just not enough to sell the stock.

Or this one:

I have 643 shares of Tesla and don’t own a Tesla. I have a Toyota Tacoma (paid off) and will keep that until the new quad CyberTruck comes out. I will definitely be purchasing that.

When this pattern of thinking is considered, the dynamics of private stock trading become a barometer of a brand’s ‘star power’ in the market. Brands that successfully engage and entertain their audience – with innovative products, compelling marketing, and strong customer relationships – see their ‘ticket prices’ rise, reflecting their desirability and success. Conversely, brands that fail to captivate an audience, much like a lackluster show, might find their secondary interest languishing, indicative of waning investor interest and market appeal. Consider this quote from the Academy of Business Research Journal. There, in 2017, Wei Feng examined the relationship between a firm’s brand equity and its investment value:

Stocks with deteriorating brand equity generally feature lower return potential.

Why do we only consider this with respect to public stock value? Combining the concepts from the business journal review on brand equity with the discussion about secondary stock sale interest for private companies reveals an intricate correlation between increased brand equity and secondary market interest.

High brand equity often translates to a strong, favorable, and unique presence in the consumer’s mind, which can significantly influence their purchasing decisions. Here are three correlations:

Brand Awareness and Equity: The journal article indicates that brand awareness, encompassing recognition and recall of a brand, plays a pivotal role in building brand equity. A private company with high brand awareness is likely to be more recognizable in the market, attracting investor attention. This awareness, especially in the upper echelons of DTC brands, signifies a strong market presence and suggests a robust potential for growth and profitability – key factors that make the company’s shares attractive in secondary markets.

Brand Image and Equity: A positive and strong brand image – comprising attributes, benefits, values, culture, personality, and user type – directly contributes to enhanced brand equity. For private companies, a compelling brand image can be a decisive factor for investors in secondary markets. A favorable brand image often reflects a company’s stability, market strength, and potential for long-term success, making its stocks a desirable commodity in secondary transactions.

Sales Promotions and Equity: Effective sales promotion strategies, both monetary and non-monetary, can bolster a brand’s market presence, directly influencing its equity. For private companies, innovative and successful promotional strategies can signal market agility and consumer appeal, traits that investors seek in secondary market transactions.

When it comes to secondary stock sale interest, this is where the concept of brand equity becomes even more crucial for private companies. High brand equity suggests to potential investors that the company has a strong market position, loyal customer base, and significant growth potential, making its shares a valuable investment.

On platforms like Hiive Markets, Forge Global, and Equity Zen, where secondary transactions for private companies occur, the level of activity and interest in a company’s shares can and should be measured as a data point. Active trading is itself a product offering and can signal strong brand awareness and a positive brand image, suggesting overall robust brand equity.

Summary: For private companies, the interest in secondary stock sales is closely correlated with the brand equity, which is a composite of brand awareness, brand image, and the impact of sales promotions. Strong brand equity not only enhances a company’s standing in the eyes of consumers but also elevates its attractiveness to investors in secondary markets, thereby influencing the liquidity and perceived value of its shares. It can be a virtuous cycle.

In the modern era of branding, where customer engagement is paramount, brands must think and act like entertainers, constantly seeking to captivate and delight their audience. They should also expand their definitions of what a customer is to a brand. A retailer’s ability to do so is not just a matter of market strategy but is directly mirrored in the valuation of their secondary interest. And like a Swiftie’s desire for a ticket at almost any cost, the higher the perceived brand-as-entertainer value, the more customers will be willing to invest. The effort to assess and publish secondary interest in top brands should become a priority, it should become as common as any other subjective measure of equity.

By Web Smith | Editor: Hilary Milnes with art by Alex Remy

Editor’s Note: to join this memo, we’ve added a study to the DTC Power List. For the new feature on polled secondaries interest, we combined a poll (n=97) with internal data on this update’s top 250 brands to assess whether those polled and others would pursue an interest in secondary stock sales from employees, founders, and / or existing shareholders of the retailers mentioned. We weighted the poll as 90% of the the assessment and we plan on growing the list to the full 800+ in the coming weeks. As mentioned above, interest in purchasing secondaries is a positive indicator for the current brand equity, potential brand equity, and current financial health of the retailers mentioned.

备忘录时尚未来的四大趋势

When you think of Vuori, Psycho Bunny, Faherty, Johnnie-O, and Bombas, you think of their rare growth trajectories. None of the brands were first-movers; they each had stiff competition form incumbent retail brands and better-positioned DTCs. But something set them apart from the rest. Here’s an example of how many of these brands work against the typical best practices associated with the segment:

Tucked away in suburban Ohio, a small boutique features a number of brands, none of which are native to the midwest. One trip around the Trevor Furbay boutique in Dublin and you’ll find Faherty, Johnnie-O, and Vuori among others. For smaller formatted stores like this one, it’s rarer to find modern brands of the caliber of those mentioned. For the brands, this type of distribution is a lot of work for relatively little revenue. To a brand of Vuori’s size, this could seem like a waste of time and energy. But for brands like these, who’ve excelled in the art of finding customers where they are, there is no such thing as an account too big or one too small.

These brands are not just popular; they are reshaping what high-performance retail looks like. With their own unique stories and approaches to business, they are rewriting the rules of success for retailers across the globe. Let’s delve deeper. In a recent deep dive by Women’s Wear Daily, the report explained the characteristics that other DTC brands can replicate for their own success. WWD explains the difficulty in achieving what these brand have:

But there are brands that have managed to break that cycle and build highly profitable businesses. In menswear, some of the most impressive include Vuori, Psycho Bunny, Faherty, Johnnie-O and Bombas. Although they service different parts of the market — everything from socks and activewear to polos and beachy button-downs — they have managed to navigate through the potential pitfalls to build multimillion-dollar businesses.

Their stories emphasize the importance of authenticity, quality, social responsibility, and community engagement – trends that are shaping the future of the retail industry.

In an increasingly competitive market, staying true to a brand’s ethos while adapting to market shifts is as difficult as it is crucial. As these brands demonstrate, remaining customer-focused and delivering high-quality products can drive significant growth. Upcoming retailers and DTC brands looking to replicate this success should focus on these aspects: offering unique, quality products, demonstrating social responsibility, fostering a strong brand community, and perfecting channel mix.

This could not come at a better time as fashion retail is poised for a leap in volume of sales for 2023. It’s never been more important to be build close relationships with consumers as competition grows between competitive brands.

Seeing those brands prioritize a small but potentially influential local retailer got me thinking about how each of these companies did so well to build brands with loyal followings, appropriate amounts of inventory, reach, and profitable growth. Here are the top four characteristics shared by each of these retailers.

Trend: Prioritize Product Quality and Innovation

Product reigns supreme in these companies. If you’ve shopped any of them, this is evident. They understand the three Ps of business: Product, Product, and Product. Bombas, a sock company that also deals in other basics, has taken the ‘product-first’ strategy to heart. They prioritize the quality and the utility of their products and you can tell when you wear them. Faherty, an East Coast-based family business, also follows this principle. They deliver products with an East Coast beach flavor made from sustainably sourced materials. The key to their success has been their dedication to creating exceptional products that are both durable enough, appealing, and readily available to consumers.

Vuori was a fitness brand born out of necessity, and another exemplar of this strategy. In “Size Charts, Returns, and EBITDA,” I explained:

Over the course of the pandemic, Vuori became one of the fastest-growing modern brands in the fashion retail space. When the retailer landed its $400 million Softbank investment (at a $4 billion valuation) in 2021, I admittedly didn’t understand the buzz. Then I bought my first pair of joggers from them around a year later. REI, one of Vuori’s top wholesale partners, made it easy. A section of the store is devoted to the brand and an REI associate is frequently stationed within the shop to answer any questions. I was an immediate fan.

Vuori offered an innovative solution to a lack of appealing athletic wear, leading to its exponential growth.

Trend: Craft a Distinct Brand Story and Culture

These standout brands don’t just deliver great products; they also built compelling stories and cultures around their brands. As CEO Dave Gatto of Johnnie-O said, “a brand is a living organism, more than just a logo or a name.” A successful company must create a culture that reflects its brand ethos.

Psycho Bunny turned the challenges it faced in its early years into an inspiring success story. This excerpt begins the narrative that laid the groundwork for the company’s present day stature:

But around 2013, things began to unravel and Psycho Bunny experienced operational issues and internal struggles. Enter Alen Brandman to the rescue.

In 2021, Brandman became the brand’s majority owner. Similarly, Bombas’ advertising campaign Compassion = Change was a powerful expression of its brand story. This campaign was instrumental in spreading awareness about homelessness and promoting a more compassionate approach towards this issue. And, Faherty had a strong human capital ethos that shaped its culture and had consistently been a part of its brand story over the past decade.

Trend: Understand Your Customer and Their Needs

These successful DTC retailers understood their customers and their needs better than anyone else. Johnnie-O’s focus on ‘West Coast prep’ resonated with its target market. Bombas’ approach to addressing the issue of homelessness through its business model appealed to its consumers’ sense of social responsibility. Vuori and Faherty too, with their unique, high-quality wears, understood and catered to the needs of their respective target markets. This quote by Brandman was pretty solid:

Men especially are strange creatures. Some men have the same type of underwear for 12 years. Some men have the same T-shirt for 10 years, so you need to make sure those core fundamentals are treated with great respect to ensure people are going to come back. And we’re not going to do anything to breach that trust.

These brands are not just selling products; they are partnering with their consumers, selling a lifestyle and fostering loyalty to an identity that their customers could connect with.

Trend: Leverage Multiple Channels for Distribution and Growth

This is the key trend, in my opinion. And it goes back to the second paragraph: several of these brands saw value in working with a small store that would barely move the needle from a sales volume standpoint. Each of these brands recognized the importance of multiple distribution channels to their growth. While direct-to-consumer retail was a crucial part of their success, they also understood the value of physical retail spaces and wholesale partnerships.

Faherty, for example, has a significant brick-and-mortar presence and operates 52 stores around the US. Psycho Bunny, despite facing internal struggles and operational issues in the past, managed to bounce back and is currently present in over 70 retail locations across North America. Vuori has followed a similar path, starting out as a direct-to-consumer brand, and then branching out into wholesale. Their strategy shows how a multi-channel approach can help a brand expand its reach and tap into different customer segments.

The success stories of these high-performing DTC brands offer a road map for other retailers. By focusing on product quality, crafting a compelling brand story, understanding the customer, and leveraging multiple channels for distribution, a retailer can replicate their success. But in the end, the internet remains the center of the wheel for these retailers. Vuori founder Joe Kudla:

There’s so much to learn about navigating different cultures and consumer preferences, but that’s the stuff I view as fun. The real challenges were raising money and getting our product marketing and fit correct. Two years in, I thought we were going to run out of money so I thank my lucky stars for the internet and being able to sell online.

These brands have shown that it’s possible to carve out a niche in the market by taking lessons from DTC’s past and challenging the status quo. As the retail landscape continues to evolve, the lessons from these trailblazing brands will remain relevant, guiding the way for future DTC success stories.

Emulating these brands doesn’t require massive investment or out-of-the-box thinking, but instead a dedication to quality, community, and authenticity. It’s a testament to the potential of retail done right, proof that in an industry often seen as challenging and unpredictable, success is achievable when businesses stay true to their values and put the customer first.

作者:Web Smith | 编辑:Hilary Milnes,美术:Alex Remy 和 Christina Williams