There is an entire eCommerce industry that fosters the ideation, launch, and early growth of direct to consumer (DtC) brands. When you notice a new digitally vertical native brand in 2018, there’s a platform aura around many of them. First you’ll see the early PR sensationalism. Then, the founders must live in the right city, have the right investors, and pay the right $25,000 / month PRs retainer. The DtC industrial complex that fosters challenger brands has, thus far, insulated many of them from the reality of attrition-by-market forces.

Consumers first notice that the brands are using Shopify or BigCommerce. Then these target customers ask: Red Antler? Brand Value Accelerator? Partners & Spade? Gin Lane? And then on to the excellent packaging presence. Lumi? That other one? In many (but not all) cases, the table stakes aren’t the physical products anymore. You can argue that in the world of DtC 2.0, the actual product is prologue.

After working with Warby Parker, Partners & Spade struck up a relationship with DTC razor brand Harry’s (before it had launched), Shinola, Hims and Peloton. For an already established brand like Peloton, Partners & Spade worked on their first national advertising campaign, but for a brand like Harry’s, the firm got in early on and helped debut the brand to the world (and has since launched Harry’s secondary brand for women, Flamingo).

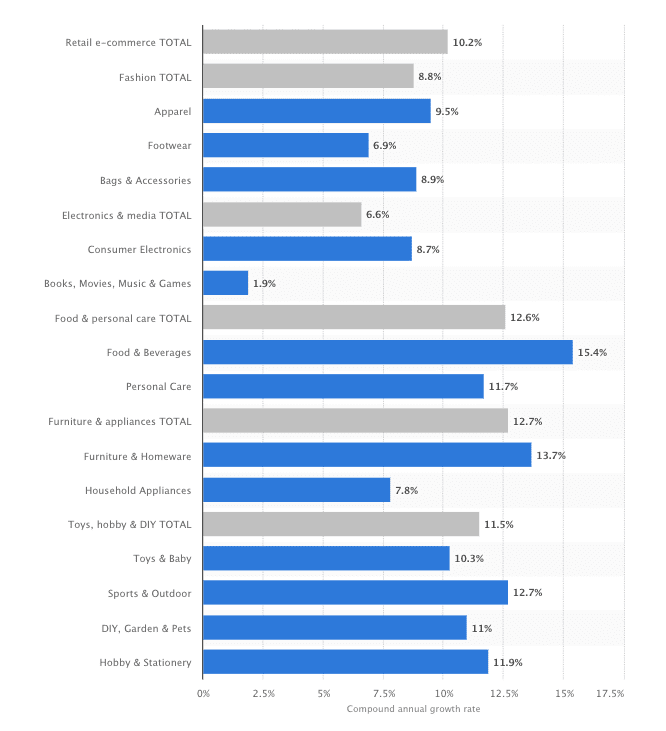

The DtC industrial complex enveloping challenger brands has, thus far, insulated many of them from the reality of attrition-by-market forces. Venture funding is the lifewater of the industrial complex. When brands launch today, many of them are hitting the ground running with $3.5 million to $17.5 million in funding. This means that the days of organic social proof (proving the efficacy of the actual product) are – for the most part – behind us. Our opinions are told to us, en masse, by the best molders of minds in the marketing today. This is not to say that new brand products aren’t great. Or that there isn’t opportunity ahead. Below is the estimated compound annual growth rate through 2022.

2PM 数据

You’ll notice that consumer packaged goods, beauty, and food & personal care are each expected to grow tremendously. This coupled with the abundance of capital and the relative ease founding a DNVB in 2019 means that it’s likely that we haven’t yet observed peak volume of challenger brands competing in stale categories.

From No. 290: brand defensibility:

- brand: the reputation of the product manufacturer. But also, the impression made upon consumers by the most visible brand evangelists.

- product: the value created by the product. But also, the value created by the ease of purchase, the fulfillment process, and the customer follow-up – post purchase.

- new distribution: how is it sold? The better the product, the more likely that a consumer has a 1:1 relationship with the brand.

- acquisition model: how does the brand achieve meaningful foot traffic? And what is the right combination of paid and organic growth? Is organic growth sustainable?

- the hive: who is the product’s first 100? Has the brand experienced organic growth on the foundation of this digital community? Will the “100” defend the brand when skeptics criticize the product and brand?

If there is a concern, it’s that the practice of launching a DNVB has ambitious founders shifting resources from within the company walls to outside of them. Brands can outsource product engineering, the brand message, the media relationships, and the customer acquisition. All while ignoring the benefits of the “product’s first 100” for day one, hockey stick-like growth: a strategy that has worked for Warby Parker, Harry’s, Away but very few others. A strategy that is often fueled by that pesky abundance of early stage capital. An amount of capital that’s often justified by the costs of the industrial complex. As we the cycle? Founders are raising to address an amalgam of costs that were once viewed as optional and eventual. But today, they are essentially table stakes to play the game on day one.

The winners will surely include a small handful of consumer brands that overturn the market dominance of their categories’ legacy brands. But if you’re looking for volume, the real winners of the DTC era are the agencies surrounding the products. They are crafting the narratives of the products that we are told by every editorial tastemaker and affiliate-driven publisher to never live without. Those deskside founder interviews aren’t cheap, I know. These are the products that expertly target us on every platform. And when we convert, we get the lovely welcome to the family email. This optimizes for LTV / CAC ratio. And then we receive it; the well-designed box takes our breath away and the nestled card with the well-tested social media CTA that gets us to bite.

This is the experience wished upon us by every challenger brand that adorns the publications that cover consumerism. And only then do we realize that every experience has hints of another. Not because the agencies aren’t expertly executing, they are. But because there are only so many ways to make categories – that weren’t exciting in the aisles of Target stores – revolutionary across the consumer web. There have been tremendous products launched into the stratosphere of consumer America. Few products have impressed me more than the agencies that build them.

Read your latest curation here: No. 297.

Report by Web Smith | Executive Membership