第 349 期:为杰克-多尔西辩护

埃利奥特管理公司(Elliott Management)计划解除杰克-多西(Jack Dorsey)在推特(Twitter)的首席执行官职务,在此之后,本报告将探讨:活力、企业集团化,以及新创业者可以借鉴的发散思维模式。推特不仅没有落后,反而可能走在了时代的前列。

为杰克-多西的领导能力辩护,就是为商界的多面手辩护。公共市场对多尔西所回避的那种深度专业化给予了奖励。然而,这些市场也开始反映出美国经济活力的下降。在《哈佛商业评论》2012 年的一篇文章中,企业家凯尔-维恩斯(Kyle Wiens)写道:"美国经济的活力正在下降:

我们生活在一个高度鼓励深度专业化的时代,也就是科技分析师文尼-米尔钱达尼(Vinnie Mirchandani)所说的 "单一数学 "时代。医生专业化、律师专业化、学者专业化、机械师专业化......几乎每个人都专业化。专业越深,赚的钱就越多。这很好。除非它不是这样。[4]

从一些就业数据来源可以推断出,美国正在进入一个新的就业市场调整期,尽管深度专业化在医学和学术界等专业中仍将始终普遍存在。能够从多个角度看待问题,避免狭隘的分析,正在重新成为一种崇高的职业价值。多才多艺是多尔西所认同的人格特质。但更重要的是,他掌舵的推特和 Square 是解决中产阶级创业途径日益减少问题的仅存的几根支柱之一。

受众与商业。在一项不科学的 2PM 民意调查(n=632,家庭收入:42,000 美元 - 98,000 美元)中,以下工具从近 30 个选项中脱颖而出。每个工具都因其对中产阶级、早期创业者的价值而备受关注:Twitter(27.1%)、Reddit(17.8%)、Gumroad(11.1%)、Patreon(22.9%)、Substack(7.3%)、Shopify(31.1%)和 Square(29.4%)。

公司越专注,似乎就越符合早期创业精神。不过,这也是有代价的。批评者质疑推特摒弃了广告潜力,而这正是企业集团化带来的增长。学术界和公开市场普遍认为,具有多面手性质的公司(在三个或三个以上杰出行业中无缝运作的公司)估值较高。我想到了一些公司: AT&T、Facebook、亚马逊、康卡斯特和谷歌。几十年来,这些公司一直被允许在政府极少监管的情况下运营新的垂直行业。在美国人的想象中,多才多艺的公司相对较新,但多才多艺的个人长期以来一直不被鼓励。

企业集团时代的到来与美国初创企业数量的减少直接相关。1982年里根反托拉斯大爆发之后,法律元素开始从结构主义转向消费者福利。这一年,AT&T 和 IBM 面临反垄断诉讼,迫使两家公司在 1984 年前进行了改革。[1]这一时期最终会以现在才开始受到审视的方式表现出来,它导致了一种新形式的反竞争行为。这意味着,新公司推出后,会被 Facebook、谷歌或亚马逊等发展速度更快、资本雄厚的公司所扼杀。

市场奖励这些公司是理所当然的;它们几乎是不可动摇的。媒体会让读者相信,创业精神正处于历史最高点。然而,这与事实相去甚远。美国经济正在僵化。泰勒-考恩(Tyler Cowen)在《自满阶级》(The Complacent Class)一书中写道:

如今,美国人换工作的可能性越来越小,在全国各地流动的可能性也越来越小,而且在某一天,根本不可能走出家门[......]经济更加僵化,更加受控,增长速度也更低。

为杰克-多西辩护提醒人们,推特是少数几个几乎没有反垄断风险的主要媒体平台之一。转向类似于 Facebook 或谷歌的联合模式是一种有期限的回报。激进投资者埃利奥特管理公司(Elliott Management)的一个主要论点是,与 Facebook 或谷歌大量的受众和广告产品不同,Twitter 在创新方面一直犹豫不决。我认为这是有意为之。

投资者抱怨 Twitter 未能推出创新的新产品。尽管推特的核心社交网络依然引人注目--它是特朗普总统的主要宣传工具之一--但包括最近的 TikTok 在内的后起之秀已经抓住了公众的想象力和眼球。[6]

在竞选活动中,分界线两边的候选人都乐于批评反竞争行为。与 Twitter 同时代的公司经常被提及。来自参议员沃伦的竞选纲领[2]:

美国的大型科技公司不仅提供有价值的产品,还对我们的数字生活拥有巨大的影响力。近一半的电子商务通过亚马逊进行。超过70%的互联网转介流量通过谷歌或 Facebook 拥有或运营的网站。

专业与深度综合

要想获得美国最令人羡慕、最有保障的工作之一,最好是掩盖自己多方面的兴趣。如果杰克-多尔西没有创办公司,他的多方面兴趣不太可能吸引到典型的高管招聘人员。尽管作为一名软件工程师,杰克-多西的工作业绩非常出色。

这一职业专业化浪潮是对几十年来影响公共市场的行业联合趋势的回应。高管招聘人员列举了制作此类简历的一些好处:增加价值主张、缩短学习曲线、"权威感"、更高的转化率以及更优越的人际网络。

在企业集团崛起的同时,人们开始强调大学毕业后的专业化,这一趋势受到了沿海科技公司招聘惯例和工作保障的影响。 500 咨询公司创始人鲁弗斯-弗兰克解释道[3]:

从 1973 年开始,回顾过去 40 年《财富》1000 强排行榜,你会发现发生了重大变化。到 1983 年,这些公司中有三分之一已跌出榜单。到 2013 年,只有 30% 的原有公司仍在榜上。这种变化的速度还将继续加快,因为预计今天的大公司中只有三分之一能在未来 25 年内存活下来。

Twitter 和 Square 的运作方式似乎与上述许多同时代的公司不同。Twitter.com(273.2 亿美元)创建于 2006 年,彻底改变了与公众人物、新闻和商业的双向交流。对于高级用户来说,它已成为 LinkedIn 的设计目标,也是 Facebook 永远无法企及的。它是一个最接近全球思想、创意、研究和文化论坛的平台。

同样,Square 也彻底改变了信贷和现金交易。Square(347.7 亿美元)成立于 2009 年,在商业和点对点支付领域取得了巨大成就。据分析师称,它的 Cash App 产品价值数十亿美元。这两家公司还没有形成今天的综合企业集团。也许,这是因为它有一个掌舵人。

需要考虑的论点是,这些平台是否更适合集中,而不是沿着联合的道路定位。

......除非它不是

专业化程度越深,赚的钱就越多。这很好。除非情况并非如此。在埃利奥特管理公司(Elliott Management) 宣布收购价值 10 亿美元的 Twitter 股票之前,多尔西最著名的批评者是学术界人士。2019 年 12 月,当纽约大学德高望重的斯科特-加洛韦(Scott Galloway)教授写信给 Twitter 执行主席时,这封信成为了一些不安分的公开市场投资者和机构持股者的行动号召。加洛韦在信的开头就表明了明确的意图:

明确地说,我的首要目标是更换首席执行官杰克-多西(Jack Dorsey)。然而,贵公司的大规模巩固武器包括一个交错的董事会,这可能会迫使股东首先寻求更换其他董事,包括你自己。[....]

当首席执行官在上午工作(兼职)时,很难要求员工在晚上和周末工作。人员外流导致产品开发乏力,阻碍了增长和货币化。[5]

诚然,多西很少有高管可与之相比。不过,当评论家和拥护者试图为他的个性提供类比时,史蒂夫-乔布斯(Steve Jobs)偶尔会被引用:史蒂夫-乔布斯(Steve Jobs)偶尔会被引用。批评者会将多西最糟糕的特点与乔布斯的反常行为进行比较:缺乏专注、失衡、善于委曲求全以及追求灵性。支持者则会把多西最好的特点与乔布斯的相比。大多数情况下,这种比较只停留在两位高管同时经营两家大公司的能力上。

去年第四季度,推特的营收超过 10 亿美元,这在该公司尚属首次。该季度广告销售额为 8.85 亿美元,比 2018 年同期增长了 12%。而 2019 年每天在其平台上看到广告的用户数量增长了 2600 万,比上一年增长了 21%。[9]

这是公平的,因为世界上只有一个史蒂夫-乔布斯(Steve Jobs),一个有才能同时管理皮克斯和苹果公司的领导者。乔布斯在被苹果公司解雇后创办了皮克斯。苹果收购 NeXT 后,乔布斯重返苹果。他一直在皮克斯担任领导职务,直到 2006 年皮克斯被迪斯尼收购。在皮克斯被收购后的一年内,iPhone 首次亮相,这款充满灵感的设备找到了将媒体、技术和商业相结合的新方法。但公平地说,多西成功地经营着两家市值合计近 700 亿美元的公司,而且他着眼于媒体和商业这两个不断发展的行业的未来。

呼唤活力

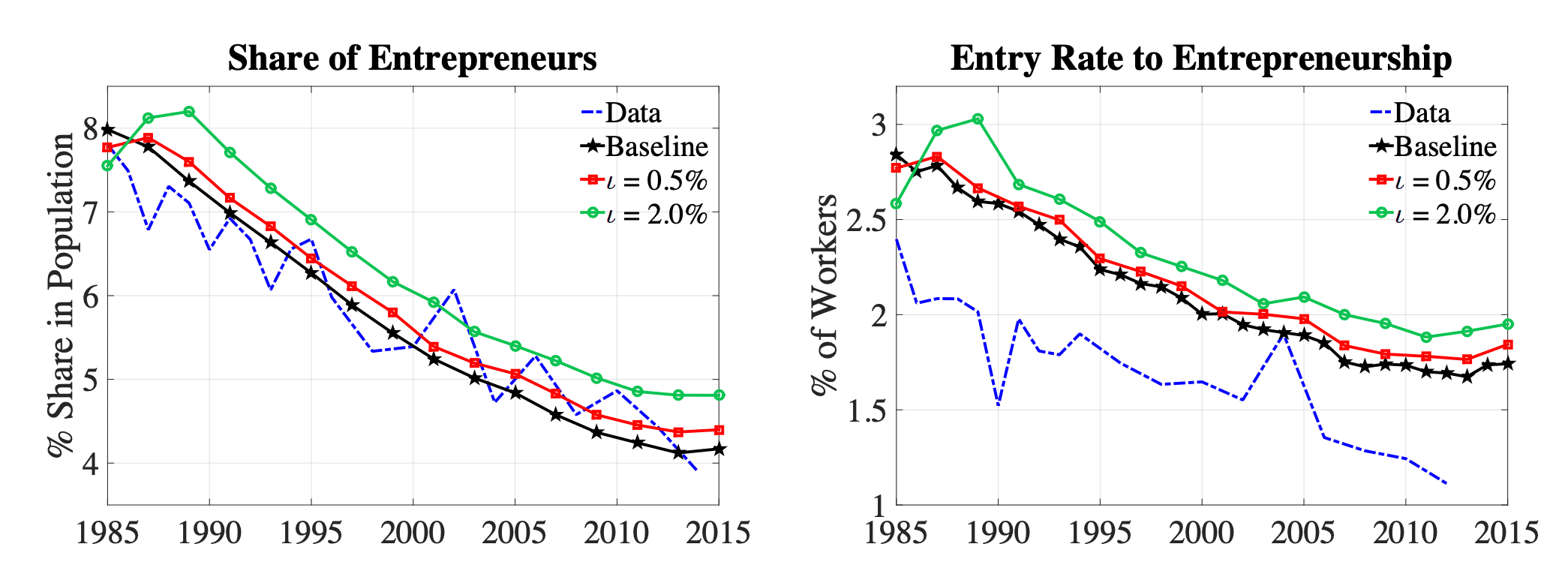

企业活力下降的一个关键因素是创业率降低,与此相关的是充满活力的年轻企业在经济中的作用下降。例如,在过去 30 年中,年轻企业在美国就业中所占的比例下降了近 30%。[7]

多学科思维是早期企业领导者的共同特征。要解决新的、棘手的问题,需要的不仅仅是雄厚的资金。它需要多尔西所规定的、企业集团所不鼓励的那种跳出框框的思维方式。

在 Facebook 和谷歌等企业集团开始调整之前,市场可能不会对 Twitter 的市场纪律给予奖励,因为政府审查和新数据隐私立法的阻力仍在增加。美国各地正在以惊人的速度起草数据隐私法案。今天,新泽西州的立法机构也加入了这场对话:

该法案要求公司在收集个人数据并将其出售给第三方之前,必须获得新泽西州消费者的许可。该法案适用于Alphabet 公司旗下的谷歌和Facebook 公司等互联网公司 ,对任何收集消费者数据的公司都有影响。[8]

随着数据隐私越来越受到关注,转向商业是一条直观的道路。从 Facebook 对 Instagram 购物车功能的重视,到谷歌收购Pointy并重视市场开发,我们已经开始看到这一点。试想一下,如果 Twitter 的首席执行官对这两个领域都有实际了解。董事会会解雇这位首席执行官吗?

结论

推特避开了当今顶级企业集团所面临的一系列不利因素:(1)媒体从广告数据转向交易数据;(2)对企业集团的反垄断审查;(3)越来越多的数据政策问题。随着向线性商务的不断转变,多西的突破性思维可能会对他的公司大有裨益。

Square 和 Twitter 代表了两个固定的行业(媒体和商业),它们的发展并没有侵犯其他垂直行业。但更重要的是,这两家公司代表了一种创业民主化,而这正是活力回归所必需的。简而言之,它们是早期创业者仅存的两种工具。

在技术方面,Square 有可能有助于 Twitter 吸引品牌合作,因为在隐私驱动的数据经济中,平台可以重新想象广告。总之,Twitter 开拓未来之路的最佳机会在于多西。不过,多西对活力再现的吸引力并不仅仅在于他掌舵的两家公司。他是罕见的创始人兼首席执行官,没有受到有投票权的股份类别的保护,这也是当今企业集团无风险的另一个标志。相反,他的领导风格非常适合有抱负的企业家,他们希望在职业专业化之外建立自己的事业。我相信,这是活力重新崛起的先兆。

多西的领导风格是当今公共市场所需要的。他的多学科思维和领导风格可能会得到公共市场的认可。当然,一旦考虑到更广泛的数据点,埃利奥特管理公司(Elliott Management)令人难以置信的团队可能会得出类似的结论。但不得不承认,多尔西可能最终需要自己的乔布斯式时刻来让批评者和支持者都闭嘴。

报告人:Web Smith |大约 2PM