Este resumo para membros foi elaborado exclusivamente para Membros executivosPara facilitar a associação, você pode clicar abaixo e obter acesso a centenas de relatórios, à nossa DTC Power List e a outras ferramentas para ajudá-lo a tomar decisões de alto nível.

No. 343: De audiências a comunidades

Uma carta aberta aos criadores. Atualmente, existem centenas, se não milhares, de boletins informativos viáveis baseados em associação. E isso é ótimo - uma vantagem inequívoca tanto para criadores quanto para consumidores. Desses milhares, vários deles servem como fontes de ideias originais, notícias e análises que são incrivelmente valiosas para os ecossistemas profissionais. É a síntese dessas ideias que tem o maior impacto potencial. Se a educação não tem preço, estamos entrando em uma nova era de criação de valor. Imagine uma cafeteria da era do Iluminismo.

Há boletins informativos dirigidos por operadores que publicam ideias originais. Há cartas significativas que fazem a curadoria das ideias de outros. Algumas delas informam sobre as notícias e outras categorizam e comentam os desenvolvimentos do setor. Muitas vezes, os relatórios que foram escritos por uma pessoa são aprimorados por outras. E, com bastante frequência, os principais veículos de comunicação, como o The Wall Street Journal ou a CNBC, pegam os conceitos originais e os transformam em seus próprios conceitos. Como em uma cafeteria, essa é uma forma valiosa de síntese de informações.

John Dowell é professor da Michigan State University. Em seus quase 40 anos de carreira, ele lecionou inglês, sociologia e antropologia. Seu curso sobre a introdução da síntese explica:

Uma síntese é uma discussão escrita que se baseia em uma ou mais fontes. Portanto, sua capacidade de escrever uma síntese depende de sua capacidade de inferir relações entre as fontes - ensaios, artigos, ficção e também fontes não escritas, como palestras, entrevistas, observações. Esse processo não é novidade para você, pois você infere relações o tempo todo - por exemplo, entre algo que leu no jornal e algo que viu pessoalmente, ou entre os estilos de ensino de seus instrutores favoritos e menos favoritos.

Na Era do Iluminismo (1715-1789), um europeu podia entrar em uma cafeteria pagando uma bebida. Mas a bebida era apenas o preço da entrada, a conversa era a atração. Não eram apenas as conversas sobre assuntos de sociologia, economia e direito que impulsionavam a época. Às vezes, os clientes ouviam conceitos que preenchiam lacunas em seu próprio pensamento. Outras conversas solidificavam ideias fundamentais, direta ou indiretamente.

Inspiração para a cafeteria

Em novembro de 2015, tive uma conversa em uma cafeteria que me marcou como uma das discussões profissionais mais importantes que já tive. A discussão era sobre a mecânica da comunidade e a necessidade de ferramentas que pudessem maximizar a serendipidade. Em um dia ocioso no final de 2015, comecei a planejar o lançamento do que eu então chamava de 2PM Links. Paguei por um serviço chamado Goodbits e lancei a página de destino do site. Depois de mais ou menos uma semana promovendo a ideia do 2PM no Twitter, confirmei que a primeira carta seria publicada para doze leitores inteiros. Eu passaria a publicar cinco dias por semana durante 180 dias úteis seguidos.

No papel: O 2PM Links seria uma parte de conceitos originais e uma parte de síntese de dados e narrativas, uma curadoria de desenvolvimentos que contariam uma história. Os próprios e-mails permitiriam o diálogo 1:1. Os leitores mais engajados escreveriam explicando como reconheceram microtendências e movimentos maiores. Outros explicavam métodos para sintetizar cada carta para obter o máximo efeito. Ocasionalmente, eu lia um e-mail de um dos primeiros assinantes explicando como um conjunto de artigos ao longo de várias semanas o ajudou a planejar as próximas etapas de sua empresa. Por quase dois anos, essas cartas ajudaram a sustentar a motivação para manter a consistência operacional.

Alcance vs. Profundidade

Para criar algo que foi projetado para crescer lentamente, mantive funções remuneradas em empresas estabelecidas. Entretanto, na época em que comecei a publicação, eu estava entre empregos na mídia. Tendo gerenciado ou liderado o comércio eletrônico em duas editoras de mídia digital, aprendi muito com dois estilos muito diferentes de publicação baseada em conversão (leia-se: afiliada).

A Empresa A criou um funil hiperdirecionado, concentrando-se em um consumidor específico (afluente). Nesse caso, o tráfego direto era alto e o SEO era um funil secundário. A marca era o mais importante. Essa empresa dependeria dela. A empresa B criou um sistema que dependia de SEO e do interesse no tópico, e não da influência da plataforma em si. Para a B,a fidelidade do leitor era secundária em relação à descoberta de SEO. Os visitantes clicavam para ler sobre um tópico com o qual haviam se deparado. Se A fosse um funil, ele seria curto e largo. A confiança era construída com o tempo. Para A, o número de leitores seria impulsionado pela fidelidade à plataforma. Enquanto isso, o funil B captava novas pessoas otimizando os artigos para palavras-chave de tópicos. Seu funil seria mais longo, com vários pontos de entrada ao longo dele. Esses pontos de entrada também serviriam como oportunidades de saída. A rotatividade era maior.

O resultado:

- Empresa A: público menor, maior fidelidade, maior taxa de conversão. 1,8 milhão a 2,2 milhões de MAU. Segmento de produto: luxo moderno.

- Empresa B: menor fidelidade, menor taxa de conversão, público maior. 6-7 milhões de MAU. Segmento de produto: luxo acessível até ofertas diárias.

A e B continuam a operar marcas de mídia bem-sucedidas com objetivos diferentes. Como se diz, há mais de uma maneira de esfolar o gato.

Para comprovar a viabilidade a longo prazo do boletim informativo, dei 180 cartas para que as coisas fossem resolvidas. À medida que as coisas avançavam, o 2PM assumia cada vez mais características da Empresa A. Depois de chegar ao número 180, essa identidade influenciava as próximas etapas. Quando eu chegasse à Carta nº 180, haveria três opções:

- seguir em frente e publicar o nº 181

- fechar a carta

- replanejar e criar uma empresa

A escolha foi a opção número três. Em minhas sete páginas de planos rabiscados, concordei que enfatizaria a profundidade em vez do alcance. Manteria a ênfase na versão "A" da mídia. Para isso, enfatizei um modelo de assinante pago. E, em seguida, um modelo de dados/consultoria. E, mais tarde, uma comunidade executiva. Essas iniciativas me permitiriam reinvestir as receitas em serviços aprimorados, design, desenvolvimento de conteúdo e maior acesso geral.

Do público à comunidade

Em uma questão de duas semanas, entre dezembro de 2017 e janeiro de 2018, mudei a plataforma do Goodbits para o Mailchimp, projetando uma integração com o Memberful. Investi em branding e design. Programei grande parte da v1 do site em meu tempo livre. E, mais tarde, importei cerca de 240 edições do 2PM para o site do WordPress, uma a uma. Em março de 2018, após dois meses de testes, a primeira assinatura do 2PM foi lançada para os assinantes da Monday Letter.

Dessa forma, o sistema do 2PM tornou-se uma espécie de funil. Cerca de 10% de todos os assinantes tornam-se membros executivos. E, mediante convite, uma porcentagem dos membros executivos opta pela comunicação direta com executivos que pensam da mesma forma em vários setores digitais.

A comunidade de Membros Executivos do 2PM, Polymathic, foi inspirada por dois pensamentos distintos.

- O fórum foi criado para ajudar executivos talentosos a desenvolver novas competências essenciais por meio de: (a) identificando pontos cegos e (b) aprendendo com líderes que dominaram essas atividades.

- Quando cheguei ao último Code Commerce, lembro-me de quatro ótimas conversas em minha primeira hora no local. Essas conversas foram com Jason Del Rey, Alex Taussig, Marc Lore e Jen Rubio.

Para participar do evento de dois dias da Recode, os ingressos variam de US$ 2.000 a US$ 4.000. Nesse aspecto, o preço tem uma função valiosa. Lá, é provável que todos com quem você conversar deixem uma impressão valiosa. Os eventos tendem a atrair operadores de alto nível. Entre os discursos principais desses eventos importantes, poucas conversas são desperdiçadas e quase todas as interações extracurriculares agregam valor profissional. Dessa forma, o evento não é o único produto. A comunidade de participantes proporciona um valor adicional. O Polymathic Forum foi projetado para se assemelhar aos corredores digitais das principais conferências, como Sundance, PopTech, Google's Solve for X ou FOO Camp. À medida que o número de participantes aumenta, aumenta também a força do local.

Desde a recepção de 15 a 25 membros executivos em nossas mesas-redondas mensais até a criação do Polymathic da 2PM, a mudança do público para a comunidade proporcionou serendipidade de maneiras que antes eram inimagináveis. A receita da assinatura torna-se a principal variável aqui. As assinaturas pagas oferecem um nível de oportunidade que as plataformas orientadas por publicidade não podem oferecer. Como exemplo prático, considere a diferença entre restaurantes fast food e estabelecimentos quatro estrelas.

Em geral, há dois tipos de restaurantes. Uma cadeia anuncia "bilhões de pessoas servidas". Isso enfatiza os KPIs da empresa: alcance, volume e satisfação das massas. Mas e se você não estiver tentando alcançar as massas? O segundo tipo de restaurante se baseia na qualidade da comida e do serviço, além da atmosfera convidativa para conversas. Nesse último ambiente, é mais provável que se encontre a serendipidade. É emblemático de uma mudança de priorizar o público (alcance) para priorizar a comunidade (profundidade).

Andy McIllwain, gerente sênior de marketing da GoDaddy, teve uma ideia interessante sobre o crescimento do setor de boletins informativos e a mudança do público para a comunidade. Em uma breve série de tweets, ele explica:

A década de 2010 foi marcada por plataformas de mídia social radicalmente abertas - uma bagunça gigantesca e incontrolável. Nos próximos dez anos? O pêndulo volta para as comunidades de nicho de interesse e propósito.

McIllwain continua:

Modelos de receita da comunidade: Patrocínio direto, taxas de associação escalonadas, comissões de afiliados e experiências pagas (eventos, retiros). As marcas precisam participar disso. É a mudança do público para a comunidade.

Embora existissem boletins informativos orientados por membros antes do Substack, o conceito de comunidade com acesso pago foi popularizado com o crescimento da popularidade da plataforma apoiada pelo A16Z. Assim como uma mesa em seu restaurante favorito, a comida é apenas uma parte da atração nesses ambientes, quando executada adequadamente. A outra é a ambientação e o ambiente. No 2PM, a ideia de comunidade é levada um passo adiante. A associação executiva abre oportunidades legítimas de serendipidade. Dez vezes por ano, convidamos nossos membros pagantes para um jantar de cortesia em um dos principais mercados (Nova York, Los Angeles, Chicago, Austin e Boston).

Dessa forma: as comunidades fechadas e orientadas pela mídia se tornaram o antídoto para o ruído dos lugares comuns digitais. Você verá isso em publicações como: Trapital, Petition, Off The Chain, Stratechery e Thing Testing. Em cada caso, cada fundador de mídia trabalha incansavelmente para fornecer valor aos seus membros pagantes. Uma associação é um voto para o futuro, além do presente. Há mais espaço para empresas como essas. E esses projetos geralmente começam com estratégias simples em torno de ideias originais. A esperança é que mais boletins informativos sejam lançados e que mais comunidades se formem ao redor deles. Devemos incentivar o envolvimento e a concorrência. É assim que as ideias tomam forma. O ecossistema, como um todo, é a cafeteria de hoje. Esse não é apenas o futuro da mídia, ele é emblemático de uma mudança maior à medida que a humanidade adota a cultura digital como sua.

Leia a carta de nº 343 aqui.

Reportagem de Web Smith | Editado por Carolyn Penner | Aproximadamente 2PM

Member Brief: SMS and The New Chaos

The moment that changed the music business happened insurgently, as they do. In 1998, when Shawn Fanning began working on Napster, the once-infamous file sharing platform, it was built on a borrowed laptop with little money and even less support. And then, in an act of serendipity, a pre-Facebook Sean Parker met Fanning in a hacker chat room. The two would go on to raise a quick $50,000, move to California, and settle in on the second floor of a bank.

Though networks of distributed files existed across the web, Napster’s focus on MP3 files (coupled with a relatively simple interface) pushed the service to 80 million registered users. The growth was seemingly instantaneous. The platform’s sweet spot: unreleased and hard-to-find music (such as studio recordings, concert bootlegs, and older songs). In a number of ways, Napster paved the way for today’s streaming economy.

There was no ramp up. There was no transition. It was like that famous shot from 2001: A Space Odyssey, when the prehistoric monkey throws a bone in the air and it turns into a spaceship. Napster was a ridiculous leap forward.

Alex Winter, Director of Downloaded

The disruption felt like the violent recoil of heavy artillery after a feather’s landing on the trigger. There was collateral damage on both sides of the barrel. The music industry was unprepared for a disruption that would cannibalize the physical retail of music. And Napster was unprepared for the litigation that would come. Chaos was created, whether intentional or not.

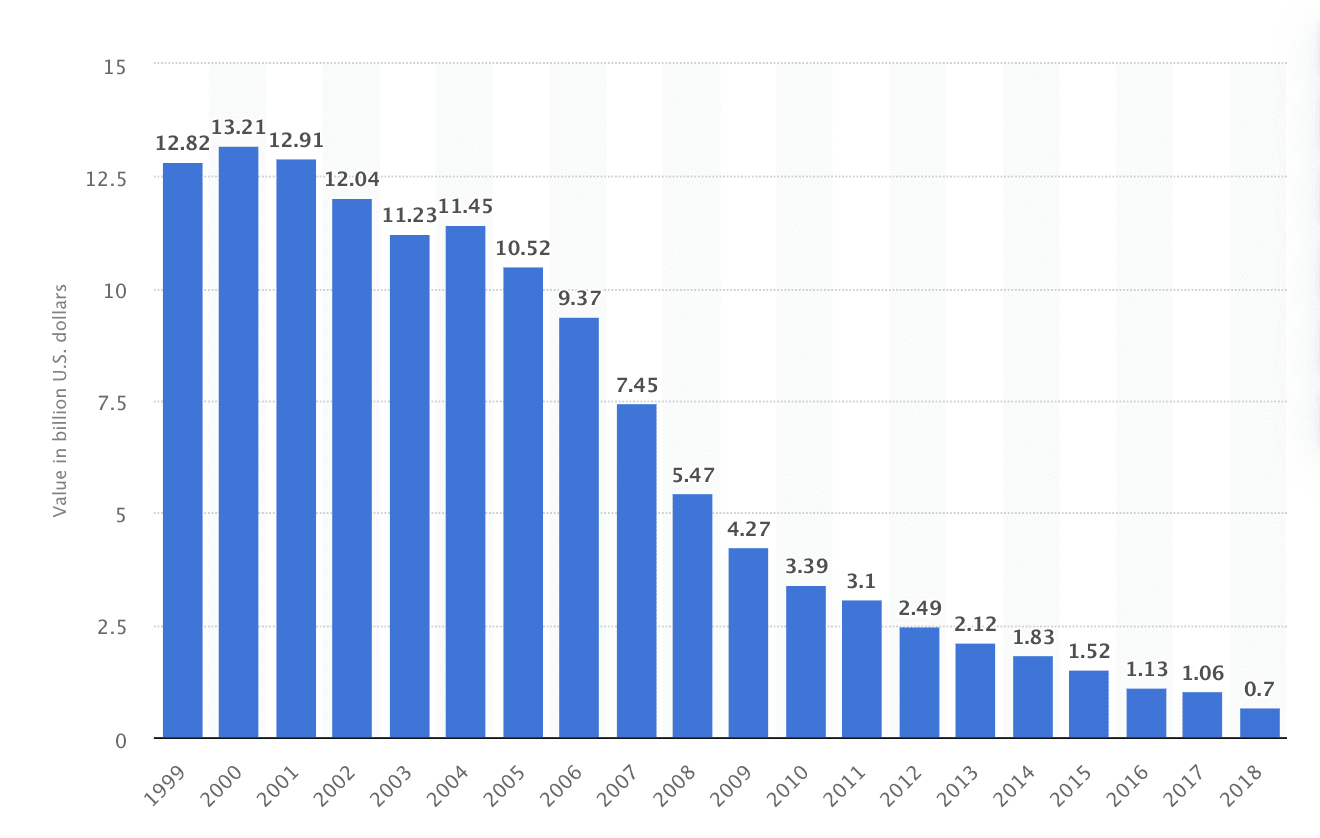

In a year’s time, billions in value was lost to Napster, a platform that was designed to market music into a public good. The whole of today’s streaming economy was born of this disruption. And while Napster was at the precipice of this shift from physical to digital, its key technologies are no longer relevant. The modern version of Napster lives on as a carbon copy of the economy that it would later influence: subscription-based streaming. It would be a retail innovation by Amazon that, when applied to digital media marketplace, would re-define a two hundred year old industry for a new millenium.

Fanning and Parker’s platform emerged at the end of an explosive decade for the music industry. There were healthy profits reaped by many labels and publishers, thanks to the maturing of the compact disc (CD) as a preferred medium. At $15 – $21 per unit, the music industry’s primary channel was an expensive one. In this way, Napster was a catalyst for market correction. Until that point, a consumer would have to purchase an entire CD to listen to the two or three songs that they preferred. Napster allowed for the ownership of individual tracks and, in turn, it devalued the sale of entire albums.

Joe Rogan recently hosted The Wu-Tang Clan’s Robert Fitzgerald “RZA” Diggs on Episode No. 1382 of his podcast. The host couldn’t have predicted that the most newsworthy snippet of the conversation would hinge on the technology of the 1990’s.

Napster comes right in and and takes all these songs where all these people who are waiting for their publishing checks are waiting for the economics to be created from music. Now, there’s no publishing check. All of the numbers have decreased because there’s no physical sell of the music to accumulate value.

Diggs would go on to explain that between 2000 – 2015, the loss in physical sales ultimately transformed the industry into one that we see today. There were few winners in music during that span. Of them: the iPod, the iPhone, Spotify, Beats By Dre, Live Nation, and Universal Music Group. Music was no longer the product for sale.

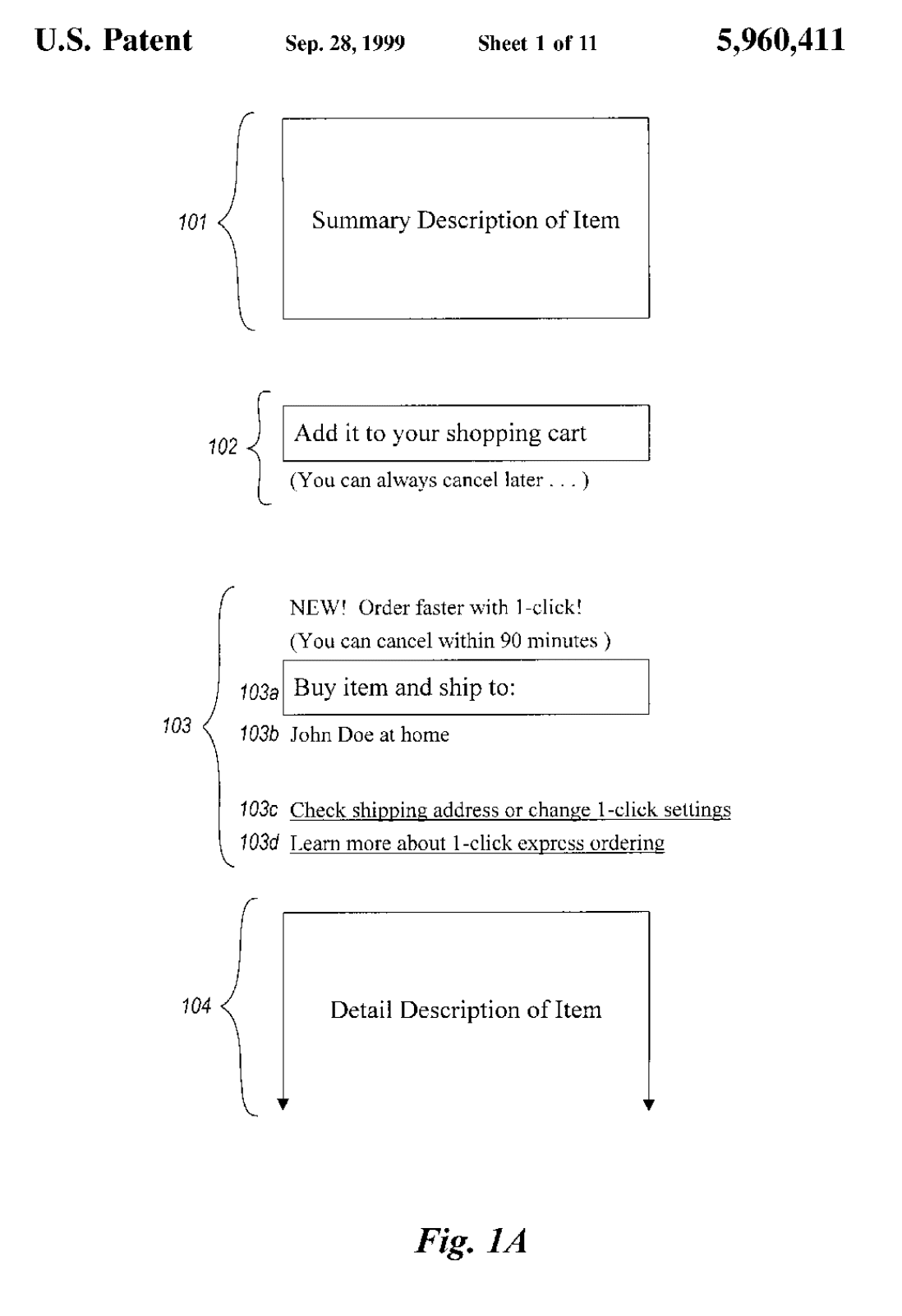

On Chaos Theory and Patent US5960411A

As eCommerce is a multi-dimensional consideration, a single theory may not be sufficient for the overall perspective views. […] However, the Chaos Theory is suitable for describing the customer decision making, especially the buying behaviours seems to be random in which the classical model of classical decision model cannot be described. [1]

The market would begin to mold around Napster’s influence. Platforms with similar architecture went live. That list included: Gnutella, Freenet, BearShare, Kazaa, LimeWire, AudioGalaxy, and Madster. It’s important to note that each of these platforms was disrupted by copyright litigation.

Flapping a butterfly’s wings over the Amazon could influence the storm in China. This is the basis of the Butterfly Effect, also known as deterministic chaos, a phenomenon where equations with little to no uncertainty yield uncertain outcomes. Chaos Theory is the mathematics that explains the butterfly wings’ theoretical influence over China’s weather patterns. In this analogy, there is a bit of irony.

Chaos Theory is a delicious contradiction – a science of predicting the behavior of “inherently unpredictable” systems. It is a mathematical toolkit that allows us to extract beautifully ordered structures from a sea of chaos. [2]

It was Apple’s CEO Steve Jobs who challenged conventional wisdom by questioning the value proposition of file sharing. For Jobs, piracy wasn’t the catalyst for Napster’s monumental growth and influence. Rather, the combination of ease and convenience was the deterministic chaos. Steve Jobs would recruit the help of Jeff Bezos and a now-famous Amazon patent to address the mathematics of buying behaviors. When the deal was announced between the two companies, Jobs levied a glowing endorsement of Bezos’ early technological advantage.

The Apple Store has been incredibly successful and now we’re taking it to the next level. Licensing Amazon.com’s 1-Click patent and trademark will allow us to offer our customers an even easier and faster online buying experience.

In September of 2000, Apple became the first company to license Amazon’s 1-Click patent (US5960411A) and trademark for use across Apple’s eCommerce properties. This innovation enabled Apple to store billing and shipping information, allowing customers to click their mouses once without any data input. To Jobs, this was the key to the industry’s music problem. By making conversion easy and ownership effortless, consumers would flock to legitimate sources of commerce. And he was right.

By 2003, the iTunes Music Store was outselling its next best competition by a margin of five to one. That competition was a legitimate version of Napster. Apple’s combination of iTunes and the iPod provided a seamless experience for conversion, management, and consumption. Apple understood that Amazon’s advantage wasn’t what it was selling, it was how it was selling. This influence would affect music and entertainment. iTunes was a precursor to 2005’s Pandora and 2008’s Spotify. Apple’s 1-Click system of retail influenced a new style of movie consumption, one that would spawn companies like Netflix in 2010 – though streaming technologies hadn’t yet caught up to market demands.

Apple would become the only company to license Amazon’s technology. US Patent 5960411A would help Amazon to nearly two decades of unfettered growth. That patent would expire in 2017. By that year, nearly half of all online retail volume in America was completed through Amazon.com and its affiliates. Consumers are willing to set aside cost for ease of purchase. Amazon was the first to prove this; Apple may have been the second.

Chaos Theory Revisited

Others, including Amazon competitors, have already noticed the 1-Click patent’s expiration. Last year, a group of companies in the alliance known as the World Wide Web Consortium, including Apple, Facebook and American Express, started working on standards to implement one-click purchasing. Google is also reportedly working on a one-click payment solution. [3]

Amazon’s innovations influenced an unforeseen number of industry advancements. With 1-Click commerce in the public domain, new upstarts like Fast join technology’s giants in building independent solutions to bolster the adoption of frictionless commerce. Apple Pay has seen wide adoption. Shopify Pay was a star of the most recent holiday season, garnering praise from the vendors who benefited from frictionless payments. This dizzying pace of innovation is the result of a technology that’s been locked away about for nearly 20 years.

Until recently, Amazon’s patents prevented wide use. Amazon’s 1998 lawsuit against Barnes & Noble is a persisting example of why few companies test Bezos knack for IP litigation.

Amazon started using one-click technology in September 1997, but did not receive a patent for it until Sept. 28 this year. Barnesandnoble has offered “Express Lane,” its one-click checkout, since the spring of 1998. “The one-click feature is one of Amazon.com’s signature strategies for differentiating itself from the competition and building loyalty among its customers,” Amazon wrote in its complaint. [4]

In 2000, then-students Erik Brynjolfsson and Michael D. Smith identified this in a case study written for MIT’s Sloan School of Management. Pricing rationality matters less when ease-driven loyalty is at the forefront of the consumer’s mind.

A direct prediction of these models then is the retailer with the lowest prices should have the highest proportion of sales since it will get sales from all the informed consumers in addition to its “share” of the uninformed consumers. However, this prediction is not supported by our data. Amazon.com is the undisputed leader in online book sales, and yet is far from the leader in having lower prices. [5]

To this end, a solution for the reduction of bottom-funnel friction recently launched. And it may be the most fluid of them all. “Ten years ago today, I was packing boxes.” Gary Vaynerchuk will go on record as saying that he isn’t very smart. Don’t let him fool you. In 1998, at the onset of his early days of growing his family’s online business, his team built one of the first iterations of an automated cart abandonment recovery. Unfortunately, he didn’t file a patent for that process – a tool that is now common throughout cloud-based carts like Shopify, BigCommerce, Adobe, and SalesForce Commerce Cloud.

Polymathic Audio No. 3: Gary Vaynerchuk

In 1998, Wine Library was grossing nearly $3 million annually. By 2011, that figure inched toward $67 million in annual sales. Vaynerchuk didn’t accept any outside investment to get to that point, a remarkable note when you consider the constraints of cash flow-driven growth. That same year, he stepped down from the family business to build VaynerMedia. When Vaynerchuk and I spoke with 2PM for Polymathic, he relayed a recent story of his father reaching out to him and asking for him to come back to the Vaynerchuk family’s original business and course-correct a company that had halved in size since Gary’s departure. Deterministic chaos: the solution that Gary executed may end up becoming another proverbial butterfly over the Amazon.

To solve the problem for Wine Library, Vaynerchuk recruited some help from his VaynerMedia team. The result was WineText, an SMS-based marketing and commerce channel. The user begins by signing up on the homepage, providing a few key details: name, address, phone number, and payment data. Like Amazon’s 1-Click system, WineText saves users’ credit cards with the help of Stripe. Powered by Twilio, Vaynerchuk and team can send a daily deal to the list at a cost of anywhere between $240 and $360 per text. According to Vaynerchuk, the SMS list of nearly 9,000 customers consistently outperforms Wine Library’s email list of 400,000 by a magnitude of 9x. And here’s why.

WineText opt-in grants Vaynerchuk access to your phone number. On occasion, a customer will receive an SMS prompt with a “high value wine offer.” Users have up to ten minutes to respond to the text with the number of bottles requested. That number of bottles is at your door within 48 hours of shipping. The top-of-funnel friction removes all bottom-funnel checkout thinking. It makes a commerce decision reflexive.

To accomplish this, WineText built a native checkout solution to account for Shopify’s native restrictions with respect to stored credit cards. For those who are interested, there is a way around it according to Postscript Co-Founder and President Alex Beller:

One way around this for more mainstream merchants who want to allow customers to buy in-message is using Postscript + Recharge + Shopify. Recharge allows for that sort of open access to credit cards of saved customers.

Beller added:

All brands should not jump on this bandwagon. However, any brand with subscriptions, natural reorder cycles, or drop strategies should lean in here. Engagement rates are too high to ignore.

As more retail operators become aware of the technology stack implemented by Vaynerchuk and team, WineText-like services will become more common. There are no patents to protect it. Amazon’s innovation indirectly impacted the streaming industry that exists today. Just as eCommerce patents changed music forever, you have to consider unrelated industries that will thrive with frictionless commerce.

Chaos Elsewhere

The Action Network, created by the Chernin Group in 2017, has an app where gamblers can track their bets across sportsbooks. It’s also using in-depth stats and analysis to draw in bettors, and has been striking content and other deals with companies like Yahoo Sports, Nascar, PointsBet, William Hill, and DraftKings, to expand its footprint. [6]

In a conversation with Action Network’s Darren Rovell, I mentioned how 1-Click technology could impact publisher-driven betting. Rovell remains skeptical that a media platform could vertically integrate in such a way. When asked if Action Network would ever facilitate live bets, the industry veteran responded:

Facilitate? Yes. Click on our platform and it clicks to a [sports] book. Or bet with a book and you can track the progress with us. But, as of now, it’s not in our best interest to be an operator.

But in the analogy of the butterfly’s flight over the Amazon, all signs point to the intersection of media, commerce, and legalized gambling as the next major disruption in consumer media. Platforms like Barstool Bets, theScore, FanDuel, Draft Kings, B/R Sports Odds, and others are positioning to move beyond informing wagers by partnering with sports books to facilitate end to end commerce. They’ll eventually want users to place bets, natively.

In the past, people would read articles or watch videos on these publishers’ properties that would inform the bets they make elsewhere. But with sports betting becoming more widely legal, publishers can close that gap — and turn this into a revenue stream for themselves. “Our whole philosophy is if we do it right and give people an opportunity to bet within theScore, they’re not going to go elsewhere,” said John Levy, CEO of theScore. [7]

Frictionless commerce will define the next ten years of mid-market, online retail in North America. As it does, savvy commerce architecture will find its way to other industries once again. Legalized gambling appears ripe for this sort of disruption. Publishers want to shorten the distance between “finding your line” and you acting on it. What was once an industry built on publishing data and insights will become one where users can act with one click of a button. If there is one thing that we’ve learned from Napster, Amazon, Apple, and the streaming economy: ease of use is the safest bet.

Pesquisa e relatório de Web Smith | About 2PM