अस्थायी रूप से अनलॉक। यहाँ कोई जवाब नहीं है, कुछ पूर्वानुमान हैं और कोई वास्तविक भविष्यवाणी नहीं है। यह बस आश्चर्यजनक आंकड़ों की प्रतिक्रिया है। मुझे लगता है कि हर जगह, बड़े और छोटे, खुदरा विक्रेताओं के बंद दरवाजों के पीछे यही बातचीत हो रही है।

वह आउटलेट मॉल उस घर से 11 मिनट की दूरी पर था जहाँ मैंने अपने प्राथमिक विद्यालय के साल बिताए थे। 1990 के दशक की शुरुआत से टेक्सास के उस हिस्से में बहुत कुछ बदल गया है। उस समय एलन, टेक्सास राष्ट्रीय स्तर पर सबसे अमीर उपनगर नहीं था। आज, औसत घरेलू आय $113,719 है। बेरोजगारी दर 4.3% है और गरीबी नगण्य है। यह एक रमणीय जगह है। उपनगर के इसी विचार के बारे में मैंने तब लिखा था जब मैंने स्वच्छ शहरीकरण की अपनी अवधारणा को समझाया था। बहुत कम राज्य टेक्सास से बेहतर उपनगर बनाते हैं। संक्षेप में, " स्वच्छ शहरीकरण शहरी नवीनीकरण के सर्वोत्तम पहलुओं को उच्च-मध्यम वर्ग और धनी बाहरी उपनगरों में आयात करता है।" ब्लूमबर्ग के एक स्तंभकार, नोआ स्मिथ के एक उद्धरण ने इस विचार को प्रेरित किया:

मैंने आगे बताया कि कैसे डलास जैसे अधिकांश महानगरीय क्षेत्र एक ऐसा प्रारूप अपना रहे हैं जो प्रत्येक उपनगरीय क्षेत्र को अपने खुदरा केंद्रों, चिकित्सा सुविधाओं और रहने की जगहों के साथ आत्मनिर्भर होने की अनुमति देता है। बहुकेंद्रित विकास (एक से अधिक केंद्रों वाला) परिवहन संपर्क, शहरी नियोजन, मिश्रित उपयोग विकास और प्रगतिशील शहरी डिज़ाइन का एक पैटर्न है। इस प्रकार के विकास का परिणाम उपनगरीय विकास का एक वर्गीकरण है जो अधिक आम हो गया है क्योंकि युवा कमाने वाले शहरों से पलायन कर रहे हैं।

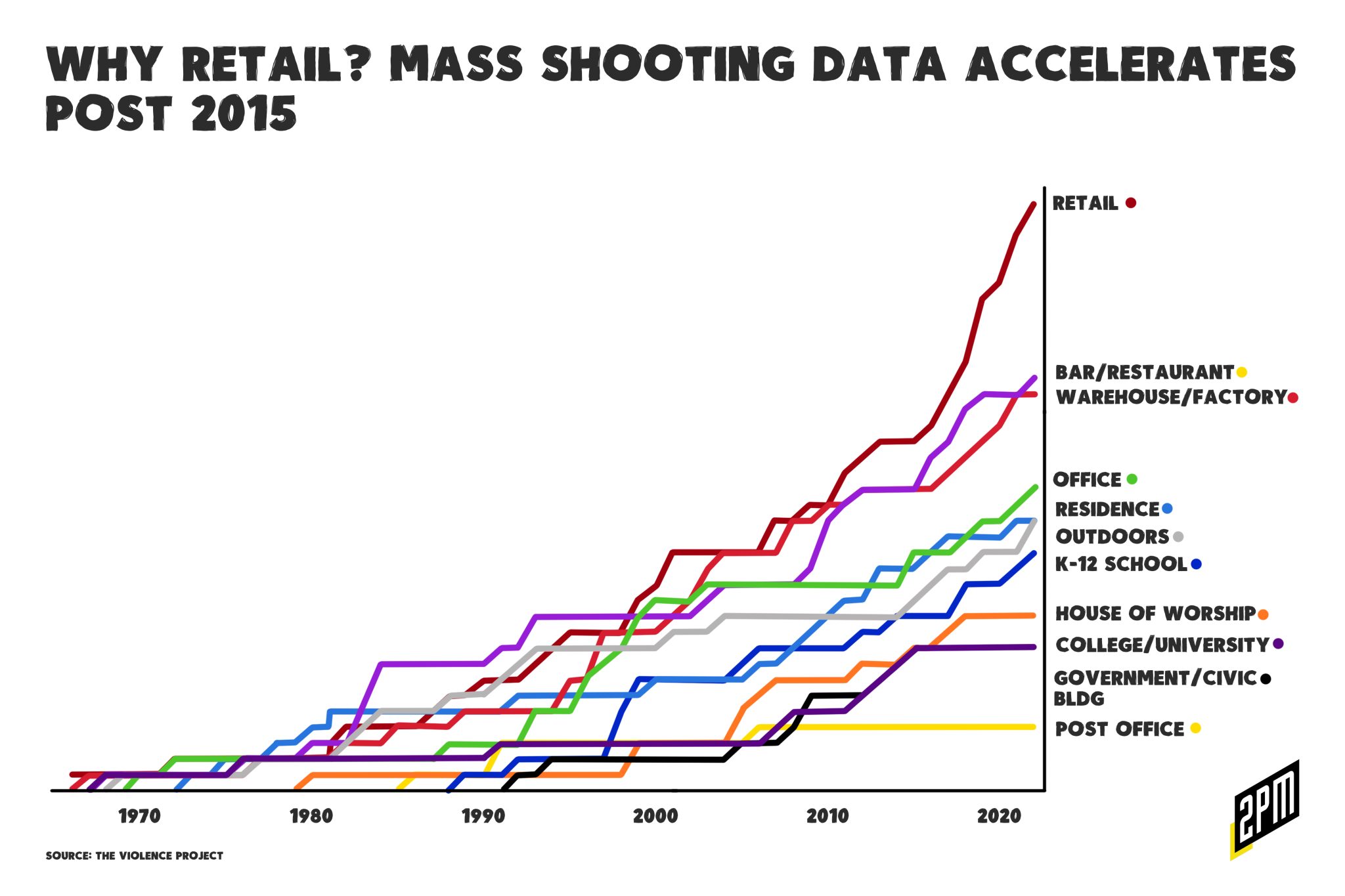

इसी पृष्ठभूमि में मैं उस क्षेत्र में हुई दुखद जनहानि को देख रहा हूँ जिसने पहले कभी इतनी बड़ी हिंसा नहीं देखी। वायलेंस प्रोजेक्ट के नए आँकड़े बताते हैं कि एलन, टेक्सास में जिस तरह की हिंसा हुई, वह तेज़ी से बढ़ रही है।

हम प्रायः स्कूलों को इन अनावश्यक हिंसा के कृत्यों का प्राथमिक लक्ष्य मानते हैं, लेकिन जबकि प्रत्येक कृत्य अपने आप में भयानक है: खुदरा व्यापार अब इसके केंद्र में है।

हाल तक तक, केबल समाचार देखने वाला औसत अमेरिकी खुदरा अपराध को सैन फ्रांसिस्को, लॉस एंजिल्स, न्यूयॉर्क सिटी, ओकलैंड, मियामी और शिकागो जैसे क्षेत्रों में केंद्रित चोरी और बर्बरता के कृत्यों के रूप में वर्गीकृत करता था। 2022 के नेशनल रिटेल फेडरेशन के रिटेल सिक्योरिटी सर्वे में, रिटेल अधिकारियों की "जोखिम और खतरे की प्राथमिकताओं" से संबंधित सबसे अधिक दबाव वाले मुद्दे अतिथि-पर-सहयोगी हिंसा, बाहरी चोरी, संगठित खुदरा अपराध और साइबर अपराध थे। "सामूहिक हिंसा" पांचवें स्थान पर थी, जिसमें 28.1% अधिकारियों ने सुझाव दिया कि यह "कुछ हद तक" चिंताजनक था और 29.8% लोगों का मानना था कि यह बहुत अधिक चिंताजनक था। यह प्राथमिकता सूची आने वाले महीनों में बदल सकती है।

खुदरा अधिकारियों के रूप में, सार्वजनिक सुरक्षा के बदलते परिदृश्य और भौतिक व्यवसायों पर इसके प्रभाव को समझना अत्यंत महत्वपूर्ण है। टेक्सास के एलन स्थित प्रीमियम आउटलेट में हाल ही में हुई दुखद सामूहिक गोलीबारी ने खुदरा दुकानों की ऐसी हिंसक घटनाओं के प्रति संवेदनशीलता को उजागर किया है। हालाँकि यह एक खुदरा समस्या है, लेकिन इसका वास्तविक समाधान खुदरा उद्योग के नियंत्रण में नहीं है। इस कहानी में खुदरा दुकानों और आस-पास के रेस्टोरेंट में निर्दोष नागरिकों को निशाना बनाए जाने जैसे सामाजिक संक्रमण से जुड़ी चिंताओं को उजागर करना होगा। मुझे नेशनल लाइब्रेरी ऑफ मेडिसिन में हाल ही में प्रकाशित एक जर्नल लेख का यह पैराग्राफ इस रिपोर्ट में उल्लिखित आंकड़ों की एक व्याख्या के लिए प्रासंगिक लगा।

हाल ही में सामूहिक गोलीबारी में एक संक्रामक प्रभाव का सुझाव दिया गया है, जो "नकल" प्रभाव जैसा है। यह प्रभाव बताता है कि व्यवहार "संक्रामक" हो सकते हैं और पूरी आबादी में फैल सकते हैं। सामूहिक गोलीबारी के उदाहरण में, संक्रामक प्रभाव तब मौजूद माना जाएगा जब एक सामूहिक गोलीबारी की घटना निकट भविष्य में सामूहिक गोलीबारी की अन्य घटनाओं की संभावना को बढ़ा दे। हवाई जहाज अपहरण, धूम्रपान निषेध और अत्यधिक भोजन सहित कई अन्य व्यवहारों में संक्रामक प्रभाव का दस्तावेजीकरण किया गया है, और आत्महत्या के संबंध में इस पर गहन शोध किया गया है। अब इस बात के प्रमाण हैं कि जब एक सामूहिक गोलीबारी होती है, तो औसतन अगले 13 दिनों के भीतर एक और घटना की संभावना में अस्थायी रूप से वृद्धि होती है।

इसलिए मुझे 1969 से 2022 तक की खुदरा गोलीबारी के इतिहास और आने वाले वर्षों में भौतिक व्यवसायों पर पड़ने वाले सभी प्रभावों का पता लगाना ज़रूरी लगा। इसमें मॉल में सशस्त्र गार्डों की बढ़ती उपस्थिति, मौके पर मौजूद पुलिस अधिकारियों का संभावित सैन्यीकरण, और सुरक्षा के प्रति बदलते नज़रिए के कारण ऑनलाइन खुदरा व्यापार की ओर संभावित बदलाव शामिल हैं।

एक ऐतिहासिक परिप्रेक्ष्य: 1969-2022

1969-1990: इस दौरान, खुदरा दुकानों में सामूहिक गोलीबारी अपेक्षाकृत कम थी। हालाँकि 1980 में मियामी, फ्लोरिडा के लिबर्टी सिटी शॉपिंग सेंटर में हुई गोलीबारी जैसी घटनाओं, जिसमें दो लोगों की जान चली गई थी, ने चिंताएँ पैदा कीं, लेकिन खुदरा दुकानों से जुड़े संभावित खतरों के बारे में लोगों में जागरूकता सीमित थी। नतीजतन, इस दौरान सुरक्षा उपायों को ज़्यादा कड़ा नहीं किया गया।

1990-2000: 1990 के दशक में खुदरा दुकानों पर गोलीबारी की घटनाओं में वृद्धि देखी गई, जिससे यह मुद्दा प्रमुखता से उभरा। 1992 में टेक्सास के किलीन स्थित फोर्ट हूड मॉल में हुई दुखद गोलीबारी, जिसमें 23 लोगों की जान चली गई, एक महत्वपूर्ण मोड़ साबित हुई। इस घटना ने मॉल में सुरक्षा प्रोटोकॉल बढ़ाने की आवश्यकता पर चर्चा को जन्म दिया। हालाँकि कुछ मॉल ने निगरानी बढ़ाने और प्रवेश बिंदुओं को सीमित करने जैसे सुरक्षा उपाय लागू करना शुरू कर दिया, लेकिन कुल मिलाकर प्रतिक्रिया अपेक्षाकृत सीमित रही।

2000-2010: इस अवधि के दौरान खुदरा दुकानों पर सामूहिक गोलीबारी की घटनाएँ चिंताजनक आवृत्ति के साथ जारी रहीं। 2007 में साल्ट लेक सिटी, यूटा में ट्रॉली स्क्वायर गोलीबारी और 2008 में ओमाहा, नेब्रास्का में वेस्टरोड्स मॉल गोलीबारी जैसी घटनाओं ने बेहतर सुरक्षा की तत्काल आवश्यकता को और रेखांकित किया। इन घटनाओं ने खुदरा विक्रेताओं को सुरक्षा उपायों को बेहतर बनाने के लिए कानून प्रवर्तन एजेंसियों के साथ और अधिक निकटता से सहयोग करने के लिए प्रेरित किया। हालाँकि, समस्या का दायरा गंभीर बना रहा।

2010-2022: इस अवधि के दौरान खुदरा दुकानों पर सामूहिक गोलीबारी की घटनाएँ चिंताजनक चरम पर पहुँच गईं। कोलोराडो के ऑरोरा थिएटर में 2012 में हुई गोलीबारी और टेक्सास के एल पासो में 2019 में हुई वॉलमार्ट गोलीबारी जैसी घटनाओं, जिनमें कई लोगों की जान चली गई, ने खुदरा दुकानों में सुरक्षा को लेकर लोगों की चिंताओं को बढ़ा दिया। खुदरा विक्रेताओं ने सुरक्षा को अधिक गंभीरता से लेना शुरू कर दिया और अपने ग्राहकों और कर्मचारियों की सुरक्षा के उपायों में सुधार करने के लिए काम किया। हालाँकि, घटनाओं की बढ़ती संख्या ने चुनौतियाँ पेश करना जारी रखा।

यहां सामूहिक गोलीबारी से संबंधित चिंताजनक आंकड़ों का वर्षवार विवरण दिया गया है (स्रोत: द वायलेंस प्रोजेक्ट ):

| वर्ष | के-12 | कॉलेज | सरकारी भवन | गिरजाघर | खुदरा | भोजन | कार्यालय | निवास स्थान | सड़क पर | गोदाम | पोस्ट ऑफ़िस |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1966 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 |

| 1967 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 0 |

| 1968 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 1 | 0 |

| 1969 | 0 | 1 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | 1 | 0 |

| 1970 | 0 | 1 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 0 |

| 1971 | 0 | 1 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 0 |

| 1972 | 0 | 1 | 0 | 0 | 2 | 1 | 2 | 0 | 1 | 1 | 0 |

| 1973 | 0 | 1 | 0 | 0 | 2 | 1 | 2 | 1 | 1 | 1 | 0 |

| 1974 | 0 | 1 | 0 | 0 | 2 | 1 | 2 | 1 | 1 | 1 | 0 |

| 1975 | 0 | 1 | 0 | 0 | 2 | 1 | 2 | 2 | 1 | 1 | 0 |

| 1976 | 0 | 2 | 0 | 0 | 2 | 1 | 2 | 2 | 1 | 1 | 0 |

| 1977 | 0 | 2 | 0 | 0 | 2 | 2 | 2 | 2 | 2 | 2 | 0 |

| 1978 | 0 | 2 | 0 | 0 | 2 | 3 | 2 | 2 | 2 | 2 | 0 |

| 1979 | 0 | 2 | 0 | 0 | 2 | 3 | 2 | 2 | 2 | 2 | 0 |

| 1980 | 0 | 2 | 0 | 1 | 2 | 4 | 2 | 3 | 2 | 2 | 0 |

| 1981 | 0 | 2 | 0 | 1 | 2 | 4 | 2 | 3 | 2 | 2 | 0 |

| 1981 | 0 | 2 | 0 | 1 | 3 | 5 | 2 | 3 | 2 | 2 | 0 |

| 1982 | 0 | 2 | 0 | 1 | 4 | 5 | 2 | 3 | 3 | 3 | 0 |

| 1983 | 0 | 2 | 0 | 1 | 4 | 5 | 2 | 5 | 4 | 3 | 0 |

| 1984 | 0 | 2 | 0 | 1 | 4 | 8 | 2 | 5 | 5 | 3 | 0 |

| 1985 | 0 | 2 | 0 | 1 | 4 | 8 | 2 | 5 | 5 | 4 | 0 |

| 1986 | 0 | 2 | 0 | 1 | 4 | 8 | 2 | 5 | 5 | 4 | 1 |

| 1987 | 0 | 2 | 0 | 1 | 5 | 8 | 2 | 5 | 5 | 4 | 1 |

| 1988 | 0 | 2 | 0 | 1 | 6 | 8 | 3 | 5 | 6 | 4 | 1 |

| 1989 | 1 | 2 | 0 | 1 | 6 | 8 | 3 | 5 | 6 | 5 | 1 |

| 1990 | 1 | 2 | 0 | 1 | 7 | 8 | 3 | 5 | 6 | 5 | 1 |

| 1991 | 1 | 3 | 0 | 1 | 7 | 9 | 3 | 5 | 7 | 5 | 3 |

| 1992 | 2 | 3 | 1 | 1 | 7 | 9 | 3 | 6 | 8 | 5 | 3 |

| 1993 | 2 | 3 | 1 | 1 | 8 | 11 | 5 | 6 | 9 | 5 | 3 |

| 1994 | 2 | 3 | 2 | 1 | 9 | 11 | 5 | 6 | 9 | 5 | 3 |

| 1995 | 2 | 3 | 2 | 1 | 10 | 11 | 5 | 6 | 9 | 7 | 3 |

| 1996 | 2 | 3 | 2 | 1 | 10 | 11 | 7 | 6 | 9 | 7 | 3 |

| 1997 | 2 | 3 | 2 | 1 | 10 | 11 | 8 | 6 | 9 | 10 | 3 |

| 1998 | 5 | 3 | 2 | 1 | 10 | 11 | 9 | 6 | 9 | 10 | 3 |

| 1999 | 7 | 3 | 2 | 3 | 12 | 11 | 11 | 6 | 9 | 10 | 3 |

| 2000 | 7 | 3 | 2 | 3 | 13 | 11 | 12 | 7 | 9 | 10 | 3 |

| 2001 | 7 | 3 | 2 | 3 | 15 | 11 | 12 | 7 | 10 | 11 | 3 |

| 2002 | 7 | 3 | 2 | 3 | 15 | 11 | 12 | 7 | 10 | 12 | 3 |

| 2003 | 7 | 3 | 2 | 3 | 15 | 12 | 13 | 7 | 10 | 14 | 3 |

| 2004 | 7 | 3 | 2 | 3 | 15 | 13 | 13 | 7 | 11 | 15 | 3 |

| 2005 | 8 | 3 | 3 | 5 | 15 | 13 | 13 | 7 | 11 | 15 | 3 |

| 2006 | 9 | 3 | 3 | 6 | 15 | 13 | 13 | 8 | 11 | 15 | 4 |

| 2007 | 9 | 4 | 3 | 7 | 17 | 13 | 13 | 8 | 11 | 15 | 4 |

| 2008 | 9 | 5 | 4 | 7 | 17 | 13 | 13 | 9 | 11 | 17 | 4 |

| 2009 | 9 | 5 | 6 | 7 | 18 | 14 | 13 | 10 | 11 | 17 | 4 |

| 2010 | 9 | 5 | 6 | 7 | 18 | 17 | 13 | 11 | 11 | 18 | 4 |

| 2011 | 9 | 5 | 6 | 7 | 20 | 18 | 13 | 12 | 11 | 18 | 4 |

| 2012 | 10 | 6 | 6 | 8 | 21 | 19 | 13 | 12 | 11 | 19 | 4 |

| 2013 | 10 | 7 | 7 | 8 | 22 | 19 | 13 | 14 | 11 | 19 | 4 |

| 2014 | 11 | 8 | 8 | 8 | 22 | 19 | 13 | 14 | 11 | 19 | 4 |

| 2015 | 11 | 9 | 9 | 9 | 22 | 19 | 15 | 14 | 12 | 19 | 4 |

| 2016 | 11 | 9 | 9 | 9 | 23 | 21 | 15 | 15 | 13 | 19 | 4 |

| 2017 | 11 | 9 | 9 | 10 | 25 | 22 | 15 | 16 | 14 | 20 | 4 |

| 2018 | 13 | 9 | 9 | 11 | 27 | 24 | 16 | 16 | 14 | 21 | 4 |

| 2019 | 13 | 9 | 9 | 11 | 31 | 25 | 17 | 16 | 15 | 22 | 4 |

| 2020 | 13 | 9 | 9 | 11 | 32 | 25 | 17 | 16 | 15 | 23 | 4 |

| 2021 | 14 | 9 | 9 | 11 | 35 | 25 | 18 | 17 | 15 | 25 | 4 |

| 2022 | 15 | 9 | 9 | 11 | 37 | 26 | 19 | 17 | 17 | 25 | 4 |

बचपन में, यह आम धारणा थी कि सबसे खतरनाक स्कूल वे होते हैं जिनमें मेटल डिटेक्टर लगे होते हैं। ये स्कूल शहर के दुर्गम इलाकों में स्थित थे; हिंसा की आशंका रहती थी और कानून प्रवर्तन एजेंसियों की मौजूदगी भी। आज भी, संयुक्त राज्य अमेरिका के सर्वश्रेष्ठ पब्लिक हाई स्कूल इस उपाय से बचते हैं। उनका मानना है कि इससे यह संदेश जाएगा कि सुरक्षा की धारणा एक खोई हुई बात है। हालाँकि K-12 स्कूलों में यह प्रचलित व्यवहार है, लेकिन खुदरा दुकानों में शायद ऐसी धारणा न हो।

अनुमानित प्रभाव और बाजार की धारणाएँ

सशस्त्र गार्डों की बढ़ती उपस्थिति: खुदरा दुकानों में गोलीबारी की बढ़ती घटनाओं को देखते हुए, यह संभावना है कि मॉल और खुदरा दुकानें खरीदारों की सुरक्षा सुनिश्चित करने के लिए सुरक्षा उपायों को प्राथमिकता देंगी। सशस्त्र गार्ड अधिक दिखाई दे सकते हैं, जो एक निवारक के रूप में कार्य करेंगे और आपात स्थिति में त्वरित प्रतिक्रिया प्रदान करेंगे। सुरक्षा की यह बढ़ी हुई उपस्थिति खरीदारों और कर्मचारियों में सुरक्षा की भावना पैदा करने और उन्हें दुकानों पर आने के लिए प्रोत्साहित करने का लक्ष्य रखेगी। सशस्त्र गार्डों की उपस्थिति एक सक्रिय उपाय के रूप में भी काम कर सकती है, जिससे संभावित हमलावरों को रोका जा सकता है।

पुलिस अधिकारियों का संभावित सैन्यीकरण: प्रवृत्ति रेखा की गंभीरता को देखते हुए, यह संभव है कि खुदरा गोलीबारी की घटनाओं पर प्रतिक्रिया देने वाले पुलिस अधिकारी अधिक सैन्यीकृत दिखाई दें। इसका उद्देश्य खतरों को शीघ्रता से बेअसर करना और हताहतों की संख्या को कम करना होगा। हालाँकि, प्रभावी प्रतिक्रिया और एक स्वागत योग्य वातावरण बनाए रखने के बीच संतुलन बनाना, खरीदारों में अनावश्यक भय या असुविधा को रोकने के लिए अत्यंत महत्वपूर्ण है। कानून प्रवर्तन एजेंसियों और खुदरा विक्रेताओं के बीच सहयोग, सुरक्षा और ग्राहक अनुभव, दोनों को प्राथमिकता देने वाले दिशानिर्देश निर्धारित करने में महत्वपूर्ण भूमिका निभाएगा।

ऑनलाइन खुदरा व्यापार की ओर रुझान: खुदरा क्षेत्रों में सुरक्षा के प्रति बदलते नज़रिए से अनजाने में ऑनलाइन खुदरा व्यापार की ओर रुझान बढ़ सकता है। अपनी भलाई को लेकर बढ़ती चिंता के कारण, उपभोक्ता ऑनलाइन खरीदारी की सुविधा और कथित सुरक्षा को चुन सकते हैं। यह बदलाव पारंपरिक खुदरा विक्रेताओं के लिए चुनौतियाँ पेश करता है। इसके अनुकूल होने के लिए, खुदरा विक्रेताओं को मज़बूत ऑनलाइन प्लेटफ़ॉर्म विकसित करने और प्रभावी ओमनीचैनल रणनीतियों को लागू करने में निवेश करना होगा जो उनकी ऑनलाइन और ऑफलाइन उपस्थिति को सहजता से एकीकृत करें। यह दृष्टिकोण खुदरा विक्रेताओं को एक सुसंगत ब्रांड अनुभव प्रदान करते हुए बदलती उपभोक्ता प्राथमिकताओं को पूरा करने में सक्षम बनाता है।

खुदरा विक्रेता अपने डिजिटल मार्केटिंग प्रयासों को बढ़ाकर, वेबसाइट उपयोगकर्ता अनुभव को बेहतर बनाकर और ग्राहकों को आकर्षित करने के लिए व्यक्तिगत सुझाव देकर ऑनलाइन खुदरा व्यापार की ओर इस बदलाव का लाभ उठा सकते हैं। कनेक्टेड मॉल की अवधारणा, जिसके बारे में मैंने 2020 में लिखा था, संयुक्त राज्य अमेरिका के कई प्रीमियम उपनगरीय मॉल में आम हो जाएगी।

यहाँ वह थीसिस है। थीसिस के केंद्र में प्रीमियम रिटेलर ईस्टन टाउन सेंटर ने अंततः ऑपरेशन की सुविधा प्रदान की (20 मील के दायरे में उसी दिन शिपिंग), हालांकि समाधान अभी भी प्रारंभिक प्रतीत होता है ।

यह ध्यान रखना ज़रूरी है कि ऑनलाइन रिटेल की ओर रुख़ कोई पूर्ण समाधान नहीं है। हिंसा के ख़तरे के कारण ग्राहकों को दुकानों से दूर नहीं रहना चाहिए। कई उपभोक्ता अभी भी भौतिक दुकानों पर जाने, लोगों से मिलने-जुलने और उत्पादों से सीधे जुड़ने के वास्तविक अनुभव को महत्व देते हैं। इसलिए, भौतिक खुदरा विक्रेताओं को ऐसे अनूठे इन-स्टोर अनुभव बनाने पर ध्यान केंद्रित करना चाहिए जो सुरक्षा पर ज़ोर देते हों, साथ ही यह भी ध्यान रखना चाहिए कि सरकारी हस्तक्षेप के बिना बहुत कुछ किया जा सकता है।

2025 की ओर देखते हुए, भौतिक और मोर्टार व्यवसायों के लिए बाज़ार की धारणाएँ बहुआयामी हैं। एक ओर, बेहतर सुरक्षा उपायों और स्पष्ट सुरक्षा उपस्थिति की माँग खुदरा विक्रेताओं की लागत में वृद्धि का कारण बन सकती है। ग्राहकों और कर्मचारियों की सुरक्षा और कल्याण सुनिश्चित करने के लिए सुरक्षा कर्मियों, तकनीकी उन्नयन और प्रशिक्षण कार्यक्रमों के लिए बजट आवंटन में वृद्धि हो सकती है। खुदरा विक्रेताओं को इन निवेशों को विश्वास निर्माण, सुरक्षित वातावरण बनाए रखने और संभावित जोखिमों को कम करने के लिए महत्वपूर्ण मानना चाहिए।

दूसरी ओर, कृत्रिम बुद्धिमत्ता (एआई), मशीन लर्निंग (एमएल), और डेटा एनालिटिक्स जैसी उन्नत तकनीकों का एकीकरण खुदरा विक्रेताओं को अपनी सुरक्षा रणनीतियों को बेहतर बनाने में मदद कर सकता है। एआई-संचालित निगरानी प्रणालियाँ वास्तविक समय में संभावित खतरों की पहचान कर सकती हैं और तत्काल अलर्ट जारी कर सकती हैं, जिससे सक्रिय प्रतिक्रिया संभव हो सकती है। एमएल एल्गोरिदम ऐतिहासिक डेटा का विश्लेषण करके पैटर्न की पहचान कर सकते हैं और संभावित जोखिमों का अनुमान लगा सकते हैं, जिससे खुदरा विक्रेताओं को सुरक्षा उपाय लागू करने में मदद मिलती है। मुझे उम्मीद है कि इस प्रकार के निवारक उपाय और भी आम हो जाएँगे।

मॉल में खुदरा विक्रेताओं की गोलीबारी का इतिहास हमारे समाज की एक दुर्भाग्यपूर्ण सच्चाई को दर्शाता है। ऐसी घटनाओं के प्रभाव को समझना और भौतिक व्यवसायों की दीर्घायु और सफलता सुनिश्चित करने के लिए सुरक्षा संबंधी चिंताओं का सक्रिय रूप से समाधान करना अत्यंत आवश्यक है। सशस्त्र सुरक्षाकर्मियों की उपस्थिति बढ़ाकर, कानून प्रवर्तन एजेंसियों के साथ सहयोग करके, और ऑनलाइन तथा स्टोर में अनुभव के लिए तकनीक को अपनाकर, खुदरा विक्रेता सुरक्षा के बदलते परिदृश्य में आगे बढ़ सकते हैं, उपभोक्ताओं का विश्वास जीत सकते हैं और खुदरा उद्योग में प्रतिस्पर्धात्मक बढ़त बनाए रख सकते हैं।

खुदरा हिंसा को सक्रिय दृष्टिकोण से देखे बिना, अमेरिकी पूंजीवाद के स्थायी स्तंभों में से एक, उपनगरीय मॉल की अवधारणा को पहचानना मुश्किल होगा। और यह देखते हुए कि इस तरह की हिंसा कई लोगों के लिए कम सहनीय है (अन्यत्र समान स्तर की हिंसा की तुलना में), यह विडंबना मुझे समझ में आती है। पूंजीवाद दांव पर है और खुदरा व्यापार अमेरिका का मुख्य नियोक्ता है। शायद तब, इसके बारे में कुछ करना होगा - एक ऐसे तरीके से जो व्यक्तिगत स्वतंत्रता का सम्मान करते हुए जीवन के महत्व का भी सम्मान करे।

खुदरा क्षेत्र पिछले कुछ समय से राजनीतिक उथल-पुथल के केंद्र में रहा है, लेकिन टेक्सास के एलन हत्याकांड से स्थिति और बिगड़ने की संभावना है। इसके साथ तालमेल बिठाते हुए, उपभोक्ताओं के बदलते नज़रिए, भय और प्राथमिकताएँ एक सुरक्षित खरीदारी के माहौल को बढ़ावा देने में महत्वपूर्ण भूमिका निभाएँगी। अंततः, इन चिंताओं के समाधान ही संयुक्त राज्य अमेरिका में खुदरा क्षेत्र का भविष्य तय करेंगे।

वेब स्मिथ द्वारा | हिलेरी मिल्नेस द्वारा संपादित, एलेक्स रेमी और क्रिस्टीना विलियम्स द्वारा कला

इस श्रृंखला का पहला भाग: जहाँ नेटसेक और वाणिज्य का मिलन होता है (चीन का प्रभाव)

संपादक का नोट: मुझे "विचार और प्रार्थना" वाक्यांश से नफ़रत है क्योंकि यह बदलाव लाने में असमर्थता दर्शाता है। मेरी आशा है कि इस दृष्टिकोण का योगदान किसी न किसी रूप में मददगार साबित होगा। इस दुखद घटना से प्रभावित परिवारों, व्यवसायों और जान गंवाने वालों के प्रति मेरी हार्दिक संवेदना।