In what can only be characterized as a leading indicator for shifting economic tides in retail, the middle-class brand is beating the S&P and leaving a trail of upper-scale competitors in its wake. It’s emblematic of the slowing bifurcation of consumers and the retailers that support them. This is from our report on the Gilded Age 2.0, a period that seemed to last for about four to five years (2017-2022).

While history doesn’t repeat itself, it does rhyme. The economically-disadvantaged deliver food, novelties, alcohol, and commodities to urban sprawls and gated suburbs – within the hour. Across the country, the net worths of the top 1% have become noticeable as conspicuous consumption of products and services have risen; the rise of platforms like StockX, Hodinkee, and Uncrate demonstrate this. For the top .01%, there are more 40,000+ square foot homes than there were in the Roaring 20’s. Retail is responding to economic realities of today. Wealth is galvanizing; retail strategies should adjust to meet the shifts head on.

As well-funded resale sites like The RealReal, thredUp, and Poshmark battle it out online, spending big money on marketing while rapidly losing valuation, a decidedly offline company is quietly winning. Its success is emblematic of the power the long middle wields in retail today. That power is only growing as bifurcation trends putters out.

Winmark owns franchises of secondhand shops across the United States to include: Plato’s Closet, Play It Again Sports, and Once Upon a Child. You’ve probably never heard of its parent company but you have at least driven by one of the shops in a suburban strip mall. Forbes profiled the company, which is a profitable, public, billion-dollar business that goes so far under the radar that it doesn’t do earnings calls. Twenty investors own 80% of the company:

Call it the tortoise of the resale wars. The company, which went public in 1993, before hardly anyone was shopping on the internet, has taken a slow-and-steady approach. New stores are opened at a modest pace, allowing the company to be selective about the franchisee applicants it accepts. It hasn’t overspent on splashy marketing.

The resale industry (formerly known as second-hand shops) is growing fast. The segment could double to $82 billion by 2026, according to an industry-funded report—fueled by a generation of young shoppers interested in buying unique pieces in an affordable, environmentally friendly way. It’s getting an added boost at a time of soaring inflation and supply chain issues, with many shoppers flocking to thrift stores after encountering high prices and out-of-stock items at big-box retailers.

Winmark’s business model is the right one for the moment. It offers affordable, practical goods for middle class Americans who, as Once Upon A Time franchisee Diane Hubel says, need to be efficient with their dollar as inflation has spiked and wages remain stagnant for most. It even offers them a way to make money in return by selling off stuff they no longer need. And because the products are secondhand, the supply chain problems plaguing other retailers don’t exist within Winmark’s portfolio of retailers. The stock isn’t guaranteed, which can be a disadvantage, but it’s reliable in that it can typically provide some option, even if it’s not the first preferred.

Then there’s the profitability. Winmark will not build an unprofitable operation.

Winmark has dabbled in e-commerce, but only when the prices are high enough to make it profitable. For instance, at Music Go Round, which sells things like used saxophones and electric guitars, the average order value is over $250, so it launched a website to sell goods online. It has no such plans for clothing stores like Plato’s Closet or Once Upon A Child, where the average item costs under $10.

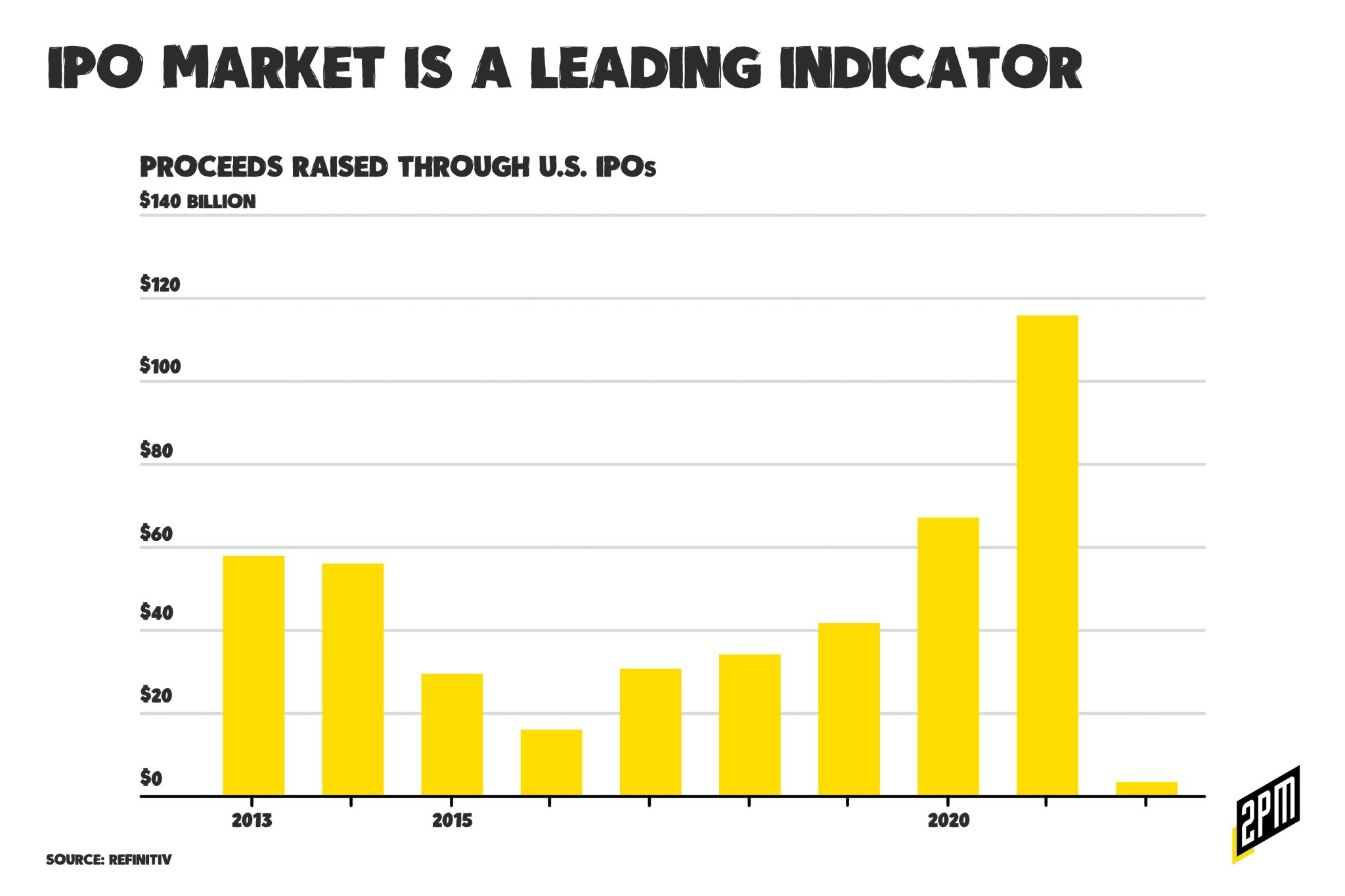

As laid out by Forbes, Winmark’s online competitors are not profitable and their valuations have been sliced their IPOs. It’s likely that if they were still private, they would avoid IPO altogether:

These DTC competitors were revolutionaries of an antiquated secondhand market but the business mechanics are hard to make work. They’re learning that now, and the boom times are over. Winmark is leaner — it doesn’t have to invest in the extensive process of listing secondhand items for mass consumption.

All of this makes for a story of a retailer who is winning in difficult times. It’s not flashy. It hasn’t raised venture capital. But it’s there for a middle class that is finding themselves against market forces working against them. It’s a bleak outlook right now for many — meaning simpler, down to basics businesses are finding themselves in better position than the recent years defined by consumer bifurcation and the companies appealing to a luxury consumer.

By Web Smith | Art by Christina Williams and Alex Remy | Edited by Hilary Milnes

Also read: Sak Pase, a reflection on our last several weeks and the recent missionary trip that I was fortunate enough to embark on.